The New EU List Of Tax Havens: Much Ado About Nothing – OpEd

By IDN

By Jan Servaes

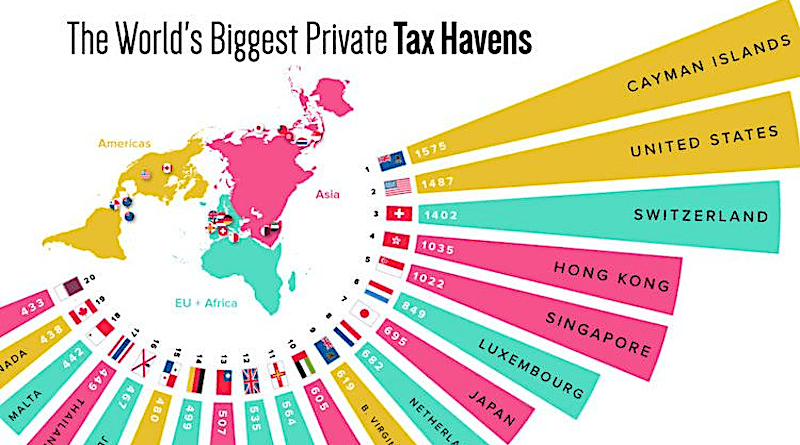

The European Finance Ministers recently revised the European list of tax havens. They added Antigua, Barbuda, Belize and Seychelles to the blacklist and removed the British Virgin Islands, the Bahamas, Costa Rica, Cayman Islands and the Marshall Islands. The list includes Russia, Panama, and other Caribbean states and territories, and six in the Pacific Ocean. The EU claims these countries either lacked tax information or failed to deliver on governance and transparency reforms commitments.

Oxfam claims that, unless structural and effective measures are taken, this list is “confusing and ineffective”, i.e., “still as incomplete as ever”. Even the European Parliament strongly condemns the recent removal of some countries from the list and calls for more transparency and stricter criteria for drawing up the list. They state that “if we focus on others, we must also look at ourselves in the mirror. It is not a pretty picture. EU countries are responsible for 36% of tax havens.”

Oxfam wants stricter criteria to blacklist countries with a zero or low tax rate automatically and to monitor European countries with the same force as non-European countries. Oxfam also called for the implementation of two long-announced purges: (a) a criterion of transparency regarding the location and ownership of the company and (b) the expansion of the average scope of the list to include more countries such as the US and the UK.

Therefore, Chiara Putaturo, tax expert at Oxfam EU, concludes: “This is another exercise for nothing. The blacklist means nothing. It leaves countries with zero rates, such as the British Virgin Islands, untouched. Moreover, it leaves countries such as the US and the UK, as well as European tax havens such as Luxembourg and Malta, alone. It is a blow to the many citizens struggling to make it to the end of the month, while the super-rich and profit-hungry multinationals are given a free pass to avoid their tax obligations.”

“The EU must finally make good on its promise to thoroughly review the blacklist if it is serious about tackling tax havens. Countries that are supposedly too big to be on the list should no longer be spared. Countries that allow their companies to pay zero taxes or not disclose their owners should be blacklisted. The EU must not allow tax havens to continue to grow within its own borders.

A code of conduct for ‘fairer tax competition’

In July 2020, the European Commission asked the Code of Conduct Group (CCG), the Council body responsible for the EU list of tax havens, to reform the criteria of the EU list of tax havens.

In May 2021, the European Commission proposed the “Business in Europe: Framework for Income Taxation (BEFIT)”, which includes rules for a common tax base and the allocation of profits between Member States based on a formula (formular distribution).

The BEFIT has been operational since September 12, 2023 and should become one of the EU’s own resources. It will reduce tax compliance costs for large companies, especially those operating in more than one Member State, and make it easier for national authorities to determine what taxes are rightly due.

In July 2023, the Council called on the Code of Conduct Group (CCG) to further work on the inclusion of the beneficial ownership criterion and to expand the geographical scope of the EU list. It is not yet clear when the CCG will be able to implement these reforms.

Oxfam

Oxfam, therefore, calls on the Spanish and Belgian EU Presidencies to strengthen the criteria for the blacklisting of tax havens in the EU and to improve the governance and transparency of the Code of Conduct Group on Corporate Taxation.

Oxfam considers the effective tax rate of 15%, agreed at OECD level and re-proposed by the European Commission, to be far too low. In addition, the OECD agreement and the EU proposal include a so-called ‘substance carve-out’, which allows companies to pay a lower tax rate than 15 percent in countries where they have many employees or material assets, such as factories and machinery.

The OECD agreement allocates almost all tax revenue from the global minimum tax to ‘countries of residence’, for example those countries where multinational companies have their headquarters. This is usually located in rich countries. However, there is an opportunity for low-income countries to raise more revenue from the minimum tax, through the Subject to Tax Rule (STR). An amendment to the bilateral tax treaties is required to apply this rule.

It is also currently being discussed in the US.

Luxembourg

The 2021 OpenLux scandal revealed that Luxembourg hosts 55,000 offshore companies with no economic activity. Several are used for tax avoidance, evasion or money laundering. More recently, the so-called Pandora newspapers (a group of about 17 newspapers including Le Monde, the SüddeutscheZeitung, Le Soir, The Guardian, The Washington Post, etc.) exposed how the rich use shell companies to pay less taxes or hide their financial activities. The hidden wealth of hundreds of world leaders, politicians and billionaires had been exposed in one of the biggest financial document leaks ever.

Oxfam America is also working on similar actions and petitions: Tax the Rich.

Tax evasion, avoidance, fraud

Many governments and companies in the EU abuse tax practices such as patent boxes, research and development super deductions. and tax credits. Evidence suggests that these practices, introduced to support innovation, have instead led to a new, damaging corporate tax ‘race to the bottom’.

Harmful corporate tax practices include aggressive tax rules that facilitate tax avoidance (such as low withholding taxes on interest, royalties and dividends) and zero-tax or low-tax regimes that inherently attract profit shifting (whether applied to foreign or domestic companies), such as patent boxes (preferential tax treatment for income from intangible assets such as royalties) and tax exemptions (temporary reduction or elimination of taxes on certain products or services).

According to EU figures, 14 of the 27 EU countries had a patent box in 2019. They all have a tax rate for patents, software and similar intangible assets below 15 percent and half of them even below 10 percent.

The Carbon Border Adjustment Mechanism (CBAM) will also be gradually introduced from 1 October 2023. The CBAM is a European regulation and part of the Fit for 55 package. This package aims to reduce greenhouse gas emissions by at least 55% before 2030. The aim of the CBAM is to prevent the risk of carbon leakage.

The CBAM is thus a price correction for imports into the EU of designated goods, based on CO2 emissions in the production process outside the EU. It is assumed that encouraging the reduction of emissions by operators in third countries may reduce global carbon emissions.

Oxfam calls for CBAM revenues to be used for climate action and for the least developed countries to be exempt so that the lowest-income countries are not disproportionately affected.

Three essential steps

Oxfam’s Tax Briefing 2021 formulates three steps for the EU and Member States to tackle tax havens:

– 1 – Strengthen the EU’s list of tax havens. Oxfam’s latest analysis identifies five EU member states – Cyprus, Ireland, Luxembourg, Malta and the Netherlands – as tax havens. The European Parliament has also called these countries tax havens and the European Commission has noted that they favor aggressive tax planning.

The Code of Conduct Group, which is responsible for blacklisting and assessing harmful tax practices in EU countries, is being urged to review the criteria and its mandate.

– 2 – Increase corporate transparency. Public Country by Country Reporting (pCBCR) and beneficial ownership transparency are crucial to prevent companies and individuals from evading their tax obligations. #OpenLux emphasizes the importance of transparency, as this would not have come to light without public registers of beneficial owners.

– 3 – Assess tax policy on wealth. Individual wealth and capital incomes are currently undertaxed compared to other sources of income such as labor and consumption.

Billionaires’ wealth has increased during the COVID-19 pandemic. While governments and ordinary people have been hit hard by the health and economic impact of COVID-19, it has in some ways been good news for billionaires, many of whom have seen their wealth grow astronomically. A recent Oxfam analysis, the Inequality Virus, shows how Europe’s 305 billionaires have grown fortunes by almost €500 billion since March 2020 – enough to write a check for €11,092 to each of the poorest 10% of the Europeans.

To bridge this gap, Oxfam is calling for an increase in wealth and capital income taxes.

There needs to be a significant effort through the private sector and philanthropists. “Billionaires’ wealth has increased more in the first 24 months of COVID-19 than in 23 years combined. The total wealth of the world’s billionaires now equals 13.9 percent of global GDP. This is a threefold increase (compared to 4.4 percent) in 2000,” according to Oxfam International’s 2022 report, titled “Profiting from Pain”.

The 2023 Forbes billionaires list tops the Belgian-domiciled Frenchman Bernard Arnault, president of Louis Vuitton, followed by American billionaires such as Tesla’s Elon Musk, Amazon owner Jeff Bezos; Larry Ellison of Oracle, Warren Buffett of Birkshire Hathaway, Bill Gates, founder of Microsoft; or Mark Zuckerberg of Facebook. These billionaires, along with the more than 2,000 billionaires around the world, are wealthy enough to make substantial progress toward achieving the now stalled SDGs.

Fighting a losing battle?

Fighting a losing battle?

The Oxfam report, Survival of the Richest, shows that the richest 1% have captured around 54% of all new wealth created in the past decade, and almost two-thirds of all new wealth created since 2020. Tax havens have played a role in this explosion of wealth because they allow the wealthiest to avoid their tax obligations.

* Jan Servaes is editor of the 2020 Handbook on Communication for Development and Social Change (https://link.springer.com/referencework/10.1007/978-981-10-7035-8) and co-editor of SDG18 Communication for All, Volumes 1 & 2, 2023 (https://link.springer.com/book/9783031191411) [IDN-InDepthNews]