A Disrupted Global Recovery – Analysis

The continuing global recovery faces multiple challenges as the pandemic enters its third year. The rapid spread of the Omicron variant has led to renewed mobility restrictions in many countries and increased labor shortages. Supply disruptions still weigh on activity and are contributing to higher inflation, adding to pressures from strong demand and elevated food and energy prices. Moreover, record debt and rising inflation constrain the ability of many countries to address renewed disruptions.

Some challenges, however, could be shorter lived than others. The new variant appears to be associated with less severe illness than the Delta variant, and the record surge in infections is expected to decline relatively quickly. The IMF’s latest World Economic Outlook therefore anticipates that while Omicron will weigh on activity in the first quarter of 2022, this effect will fade starting in the second quarter.

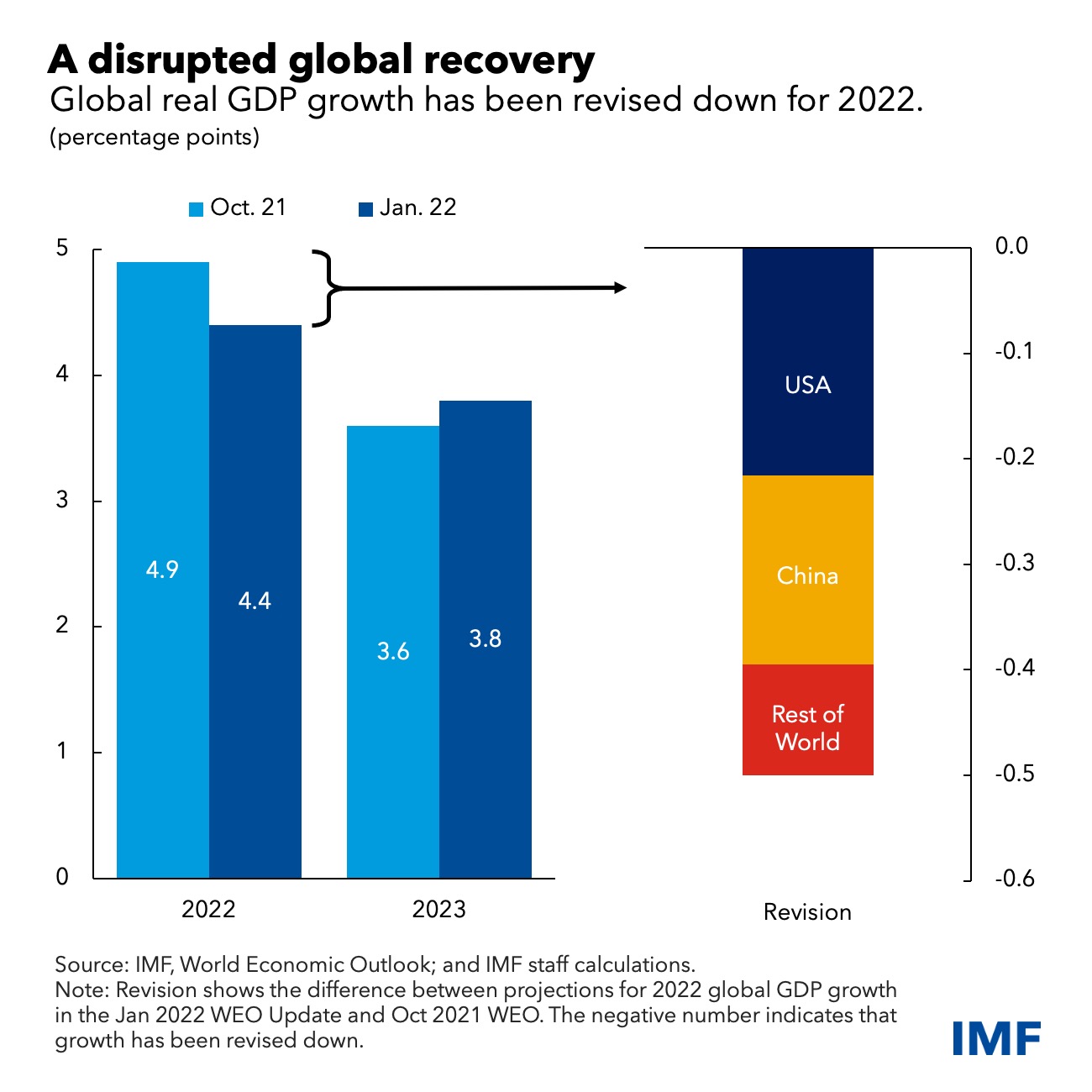

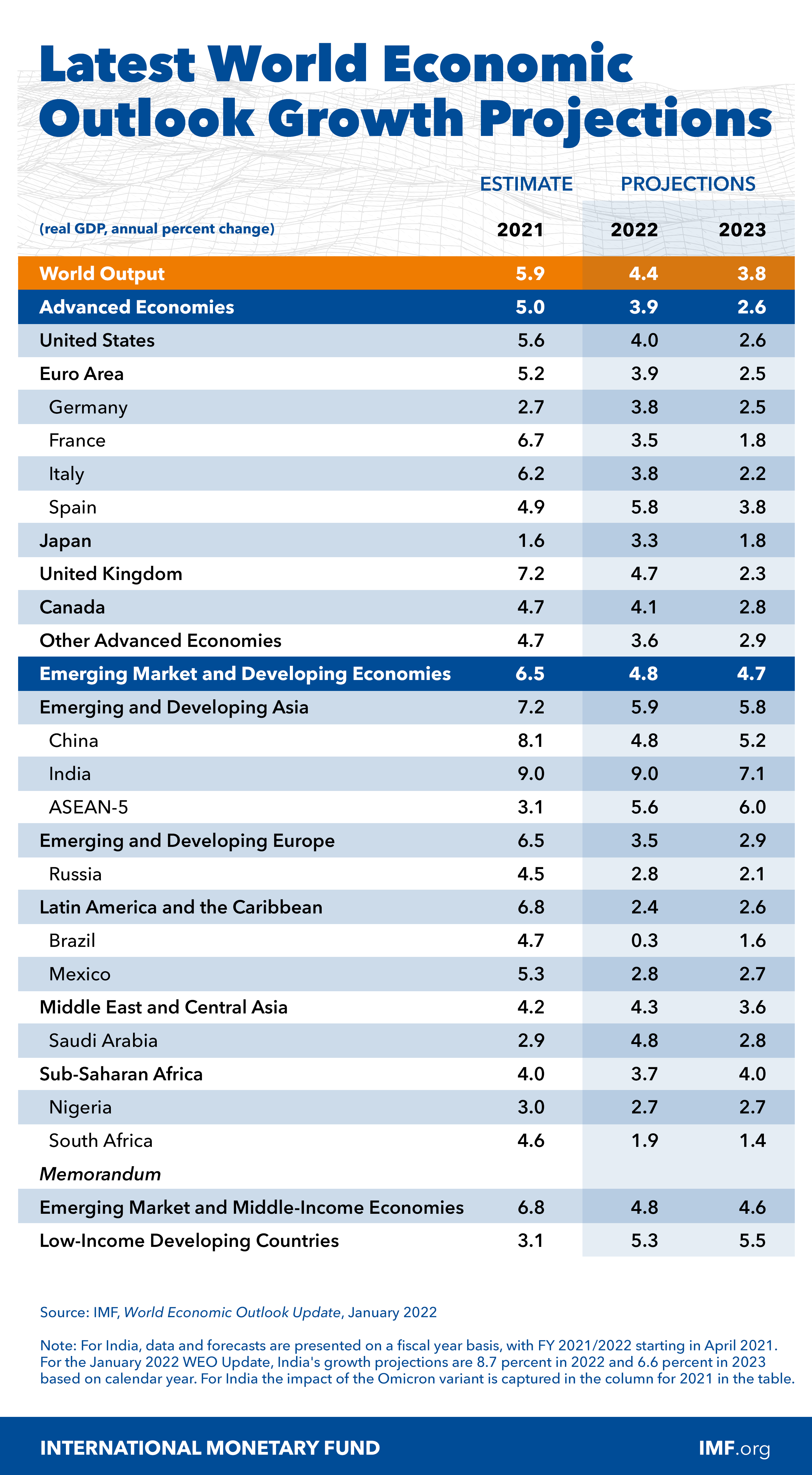

Other challenges, and policy pivots, are expected to have a greater impact on the outlook. We project global growth this year at 4.4 percent, 0.5 percentage point lower than previously forecast, mainly because of downgrades for the United States and China. In the case of the United States, this reflects lower prospects of legislating the Build Back Better fiscal package, an earlier withdrawal of extraordinary monetary accommodation, and continued supply disruptions. China’s downgrade reflects continued retrenchment of the real estate sector and a weaker-than-expected recovery in private consumption. Supply disruptions have led to markdowns for other countries too, such as Germany. We expect global growth to slow to 3.8 percent in 2023. This is 0.2 percentage point higher than in the October 2021 WEO and largely reflects a pickup after current drags on growth dissipate.

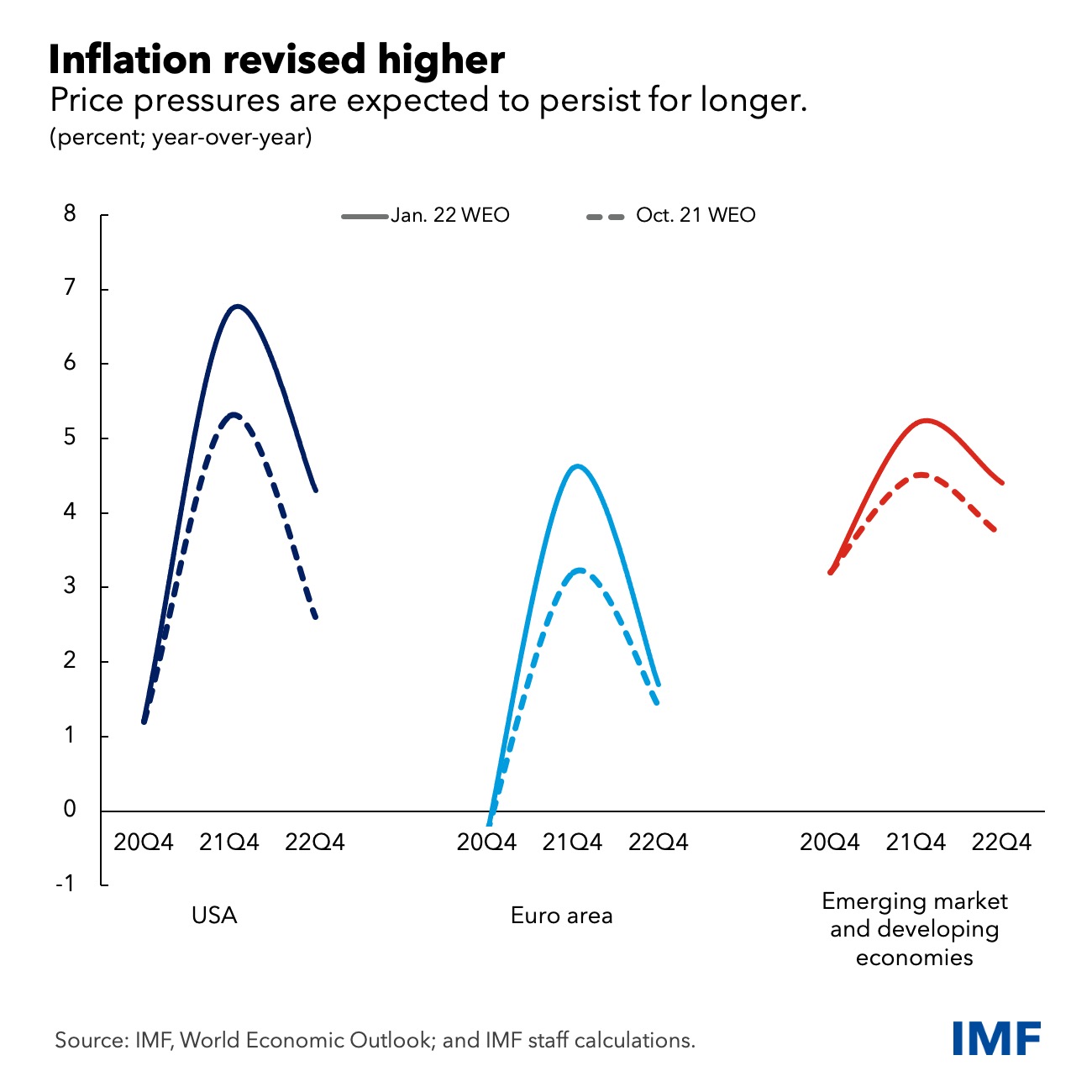

We have revised up our 2022 inflation forecasts for both advanced and emerging market and developing economies, with elevated price pressures expected to persist for longer. Supply-demand imbalances are assumed to decline over 2022 based on industry expectations of improved supply, as demand gradually rebalances from goods to services, and extraordinary policy support is withdrawn. Moreover, energy and food prices are expected to grow at more moderate rates in 2022 according to futures markets. Assuming inflation expectations remain anchored, inflation is therefore expected to subside in 2023.

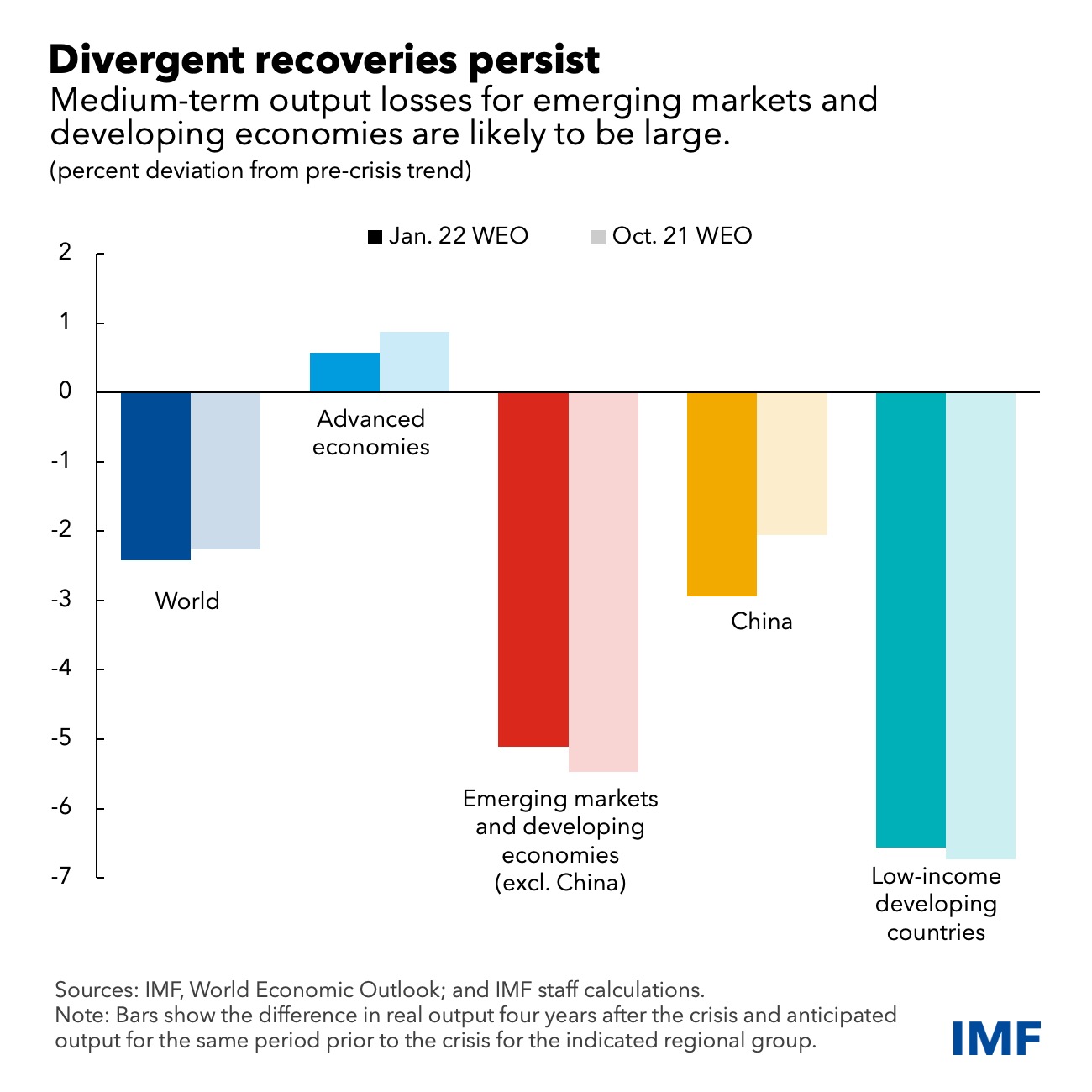

Even as recoveries continue, the troubling divergence in prospects across countries persists. While advanced economies are projected to return to pre-pandemic trend this year, several emerging markets and developing economies are projected to have sizeable output losses into the medium-term. The number of people living in extreme poverty is estimated to have been around 70 million higher than pre-pandemic trends in 2021, setting back the progress in poverty reduction by several years.

The forecast is subject to high uncertainty and risks overall are to the downside. The emergence of deadlier variants could prolong the crisis. China’s zero-COVID strategy could exacerbate global supply disruptions, and if financial stress in the country’s real estate sector spreads to the broader economy the ramifications would be felt widely. Higher inflation surprises in the United States could elicit aggressive monetary tightening by the Federal Reserve and sharply tighten global financial conditions. Rising geopolitical tensions and social unrest also pose risks to the outlook.

Global Efforts

To address many of the difficulties facing the world economy, it is vital to break the hold of the pandemic. This will require a global effort to ensure widespread vaccination, testing, and access to therapeutics, including the newly developed anti-viral medications. As of now, only 4 percent of the population of low-income countries are fully vaccinated versus 70 percent in high-income countries. In addition to ensuring predictable supply of vaccines for low-income developing countries, assistance should be provided to boost absorptive capacity and improve health infrastructure. It is urgent to close the $23.4 billion financing gap for the Access to COVID-19 Tools (ACT) Accelerator and to incentivize technological transfers to help speed up diversification of global production of critical medical tools, especially in Africa.

At the national level, policies should remain tailored to country specific circumstances including the extent of recovery, of underlying inflationary pressures, and available policy space. Both fiscal and monetary policies will need to work in tandem to achieve economic goals. Given the high level of uncertainty, policies must also remain agile and adapt to incoming economic data.

With policy space diminished in many economies, and strong recoveries underway in others, fiscal deficits in most countries are projected to shrink this year. The fiscal priority should continue to be the health sector, and transfers, where needed, should be effectively targeted to the worst affected. All initiatives will need to be embedded in medium-term fiscal frameworks that lay out a credible path for ensuring public debt remains sustainable.

Monetary policy is at a critical juncture in most countries. Where inflation is broad based alongside a strong recovery, like in the United States, or high inflation runs the risk of becoming entrenched, as in some emerging market and developing economies and advanced economies, extraordinary monetary policy support should be withdrawn. Several central banks have already begun raising interest rates to get ahead of price pressures. It is key to communicate well the policy transition towards a tightening stance to ensure orderly market reaction. Where core inflationary pressures remain subdued, and recoveries incomplete, monetary policy can remain accommodative.

As the monetary policy stance tightens more broadly this year, economies will need to adapt to a global environment of higher interest rates. Emerging market and developing economies with large foreign currency borrowing and external financing needs should prepare for possible turbulence in financial markets by extending debt maturities as feasible and containing currency mismatches. Exchange rate flexibility can help with needed macroeconomic adjustment. In some cases, foreign exchange intervention and temporary capital flow management measures may be needed to provide monetary policy with the space to focus on domestic conditions.

With interest rates rising, low-income countries, of which 60 percent are already in or at high risk of debt distress, will find it increasingly difficult to service their debts. The G20 Common Framework needs to be revamped to deliver more quickly on debt restructuring, and G20 creditors and private creditors should suspend debt service while the restructurings are being negotiated.

At the start of the third year of the pandemic, the global death toll has risen to 5.5 million deaths and the accompanying economic losses are expected to be close to $13.8 trillion through 2024 relative to pre-pandemic forecasts. These numbers would have been much worse had it not been for the extraordinary work of scientists, of the medical community, and the swift and aggressive policy responses across the world.

However, much work remains to ensure the losses are contained and to reduce wide disparities in recovery prospects across countries. Policy initiatives are needed to reverse the large learning losses suffered by children, especially in developing countries. On average, students in middle-income and low-income countries had 93 more days of nation-wide school closures than those in high income countries. On climate, a bigger push is needed to get to net-zero carbon emissions by 2050, with carbon pricing mechanisms, green infrastructure investment, research subsidies, and financing initiatives so that all countries can invest in climate change mitigation and adaptation measures.

The last two years reaffirm that this crisis and the ongoing recovery is like no other. Policymakers must vigilantly monitor a broad swath of incoming economic data, prepare for contingencies, and be ready to communicate and execute policy changes at short notice. In parallel, bold, and effective international cooperation should ensure that this is the year the world escapes the grip of the pandemic.

*About the author: Gita Gopinath is the First Deputy Managing Director of the International Monetary Fund (IMF) as of January 21, 2022. In that role she oversees the work of staff, represents the Fund at multilateral forums, maintains high-level contacts with member governments and Board members, the media, and other institutions, leads the Fund’s work on surveillance and related policies, and oversees research and flagship publications.

Source: This article was published by IMF Blog