Silver Lining To India’s Trade Blues – Analysis

India’s merchandise exports have now contracted for 13 months in a row, reflecting the global slowdown and impact of China’s economic recalibration. But, therein lay new opportunities and challenges for India’s economic diplomacy

By Rajrishi Singhal*

India’s exports of goods have now shrunk for 13 months in a row. Even as this presents a threat to the government’s “Make in India” programme, it also provides some clues to future focus areas for India’s economic diplomacy.

Data for December 2015[i] shows merchandise exports at $22.29 billion, 14.75% lower than exports booked in December 2014. Cumulative exports for the first nine months of 2015-16 (April-December 2015) amounted to $196.6 billion, down 18% over the comparable period of 2014-15. There is one silver lining though: the trade deficit for the first nine months of 2015-16 ($99.2 billion) is lower than the deficit in 2014-15 ($111.68 billion). This is primarily due to lower oil prices.

There are two ways of slicing this data to understand incipient trends; locating the geographical source of this demand compression and looking at performance of specific commodities.

According to Commerce Ministry’s database on exports by region[ii], in dollar terms, the three destinations showing maximum contraction in Indian exports (or areas that are buying much less from India than in the previous year) are Latin America (down by 36.73%), Commonwealth of Independent States (CIS) & Baltic region (down 32.4%) and Africa (25.59%). Clearly, India’s foreign policy practice and economic diplomacy needs to expend greater energy on these areas.

Granulated regional data provides better insights. In Asia, for instance, the sharpest fall in absolute terms has been in exports to the West Asian countries that are members of the Gulf Cooperation Council (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and United Arab Emirates). The second largest drop in absolute terms has been exports to the ASEAN countries, followed by North East Asia (which includes China). While the GCC phenomenon can be ascribed to shrinking oil revenues, leading to diminution of demand for Indian goods, it is the slowing of the Chinese economy that explains the North East Asian drop and a second round impact leading to dwindling of ASEAN demand.

Examining trade data through the lens of performance of specific commodities highlights stasis in India’s manufacturing industry and the need for providing stimulus. This can be either through “Make In India” initiative or through additional investments. The data clearly shows slowing demand overseas for agricultural (rice, other cereals, oil cakes and oil seeds) and oil-related commodities. However, more importantly, import data shows a huge spike in purchases of pulses, gold and silver–indicating higher consumption–but demand for fuel, mineral ores and metals, machinery and equipment remained in negative zone, reflecting static industrial and manufacturing demand.

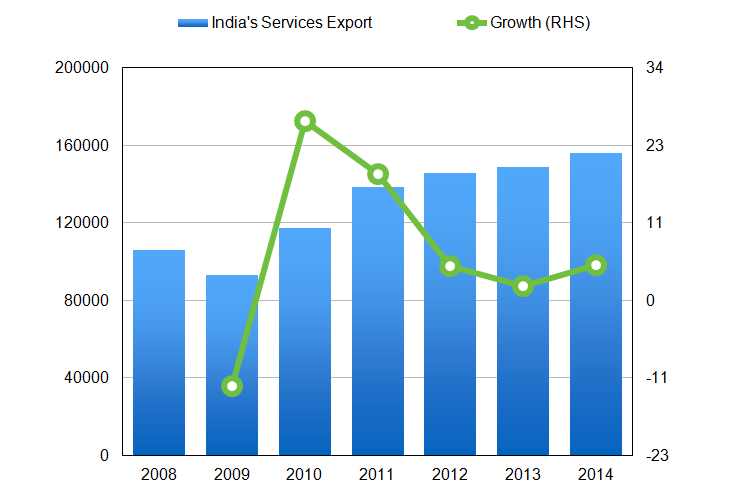

Yet, there are some oases of optimism— India’s trade in services for the first eight months of 2015-16 (April-November) showed a positive balance of $48.047 billion. In fact, this is one area in which India not only fares better than China (which has traditionally suffered a negative trade balance in services) but has also been able to stave off the China slowdown factor more effectively that merchandise trade.

This, then, points to another focus area for India’s future economic diplomacy, including its bilateral engagements with China or European Union (EU) and regional arrangements like Association of Southeast Asian Nations (ASEAN) or Regional Comprehensive Economic Partnership (RCEP).

The India and China example are instructive. India and China have multiple grounds for disagreement which occasionally drives a wedge between the two countries in multilateral negotiating forums. China’s overwhelming trade surplus with India and the festering border dispute are some of the legacy issues. Thesehave been joined by new contentions, such as India’s lack of response to China’s generous offer of building critical infrastructure.

But a common grouse should be uniting both countries’ interests at global negotiating platforms: services exports. This is because multilateral trade negotiations — such as those under World Trade Organisation (WTO) — or regional trade arrangements (examples being RCEP) and even bilateral agreements focus overly on goods trade. This is disadvantageous for India, which has competitive advantage in services but is denied level playing field in trade negotiations. China is likely to be in a similar situation when contracting exports of manufactured products forces its hand to provide a greater thrust to service exports.

India’s service sector has been a saviour for both domestic economic growth and for overall balance of payments. China’s trade in services is in negative zone because it’s a net spender on tourism and education: its trade balance was a negative $159.9 billion in 2014. This is ripe for change — a Chinese government policy document released in February 2015 set a target of $1 trillion of services trade by 2020, including accelerating services exports[iii] [iv].

With China expected to refocus economic efforts on strengthening its services sector and increasing its share in exports, both India and China need to coordinate their strategies and act in concert during multilateral trade and investment negotiations.

In fact, the UNCTAD Handbook of Statistics 2015, released recently[v] by the United Nations Conference on Trade and Development (UNCTAD), shows that services bailed out global trade during 2014. Data also shows the criticality of services exports for India, and its negative impact on China’s balance of payments. Given this strategic importance of services for both countries trade, and the continuing slowdown in demand for goods, overall global trade patterns are pointing towards the need for greater India-China cooperation in services trade.

About the author:

*Rajrishi Singhal is Senior Geoeconomics Fellow, Gateway House. He has been a senior business journalist, and Executive Editor, The Economic Times, and served as Head, Policy and Research, at a private sector bank, before shifting to consultancy and policy analysis.

Source:

This feature was written for Gateway House: Indian Council on Global Relations.

References:

[i] Department of Commerce, Ministry of Commerce and Industry, Government of India, India’s Foreign Trade (Merchandise): December, 2015;; <http://commerce.nic.in/tradestats/PressRelease.pdf>

[ii] Department of Commerce, Ministry of Commerce and Industry, Government of India, December, 2015;<http://commerce.nic.in/ftpa/rgn.asp>

[iii] The State Council; The People’s Republic of China, New guideline on boosting trade in services, ; 15 February, 2015; <http://english.gov.cn/policies/latest_releases/2015/02/15/content_281475056101818.htm>

[iv] Gerry Shih; China’s economic planners aim to boost service exports; Reuters, 14 February, 2015<http://www.reuters.com/article/china-exports-idUSL1N0VO09W20150214>

[v] UNCTAD;,International trade in services was main driver of growth in global trade in 2014 ; <http://unctad.org/en/pages/newsdetails.aspx?OriginalVersionID=1149&Sitemap_x0020_Taxonomy=UNCTAD%20Home>