Inverted Yield Curves, Recessions, And You – Analysis

By Paul F. Cwik*

If one reads the headlines you might think that since the yield curve has inverted, the economy is in a recession, Trump will be swept from office and then the Progressives’ goals are right around the corner. Not so fast! While much of that may still happen, we are not there yet.

While some on the Left (see Bill Maher) may be openly hoping for the economy to slip into a recession, we are not currently in a recession and whether we are heading for one requires some serious economic analysis. To understand what an inverted yield curve means, we first need to understand what the yield curve is.

What is the Yield Curve?

Often, when economists think of the economy, they simplify. This action is necessary. They try to focus on the important factors and set the less important and irrelevant factors aside. Thus, a theory of how the economy works is an abstraction that tries to illustrate causal and connected links.

Often, when economists think of the economy, they simplify. This action is necessary. They try to focus on the important factors and set the less important and irrelevant factors aside. Thus, a theory of how the economy works is an abstraction that tries to illustrate causal and connected links.

In many economic models, economists use a single interest rate to represent the whole intertemporal market. Often they will theorize that when the interest rate rises, X will happen or if the Fed lowers the interest rate, then Y will be the result. However, the real world does not have a single interest rate. In fact, there are many interest rates. When we separate interest rates across maturities, we get what is called “The Term Structure of Interest Rates.” So across this structure, there will be an interest rate for a 3-month instrument, another interest rate for a 1-year instrument, a different one for a 10-year instrument, and so forth.

When we look at a very specific type of term structure, where the default risk is at zero, we are looking at what is called “The Yield Curve.” In the US economy, there is really only one market where we find zero default risk and that is the market for US Treasury Bills, Notes and Bonds. The reason why there is zero default risk is that if you go to cash in your US Treasury Bond, you will always be able to get dollars. Since the dollar is fiat money, meaning that it is not backed by gold, the US government can always create more dollars to honor its obligation. (Of course the value of the dollar will be eroded by the money creation, but that’s a different story.)

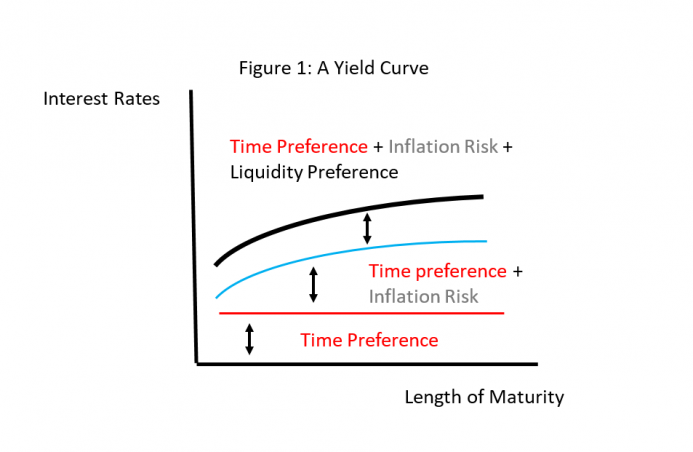

If we plot out the different maturities across the horizontal axis and the percentage rate of returns on the vertical, then we will have a graphical vision of the Yield Curve. Typically, the short-term rates are lower than the long-term rates. Graphically, we would see an upward slope. There are two major reasons for this: inflation risk and liquidity preference. Inflation risk is the risk that stems from the fear that the value of the dollar will depreciate over time. As we look at the historical inflation rates we see that the value of the dollar has been continuously eroded since we left the gold standard. Liquidity preference stems from an uncertain future. (See Figure 1.)

An investor might reason in this way, “I want to invest my money, but what if something happens and I need cash?” This reasoning reflects the fact that it is better to be liquid than not. When we add a term structure to the investment, we see that this risk changes over the various time horizons. So what is the risk of something happening where I will need cash in the next 3 months? Now compare that risk with tying up money for one or two years. Then compare that risk with tying up money for 30 years. As the length of maturity increases, the risk of something unexpected happening also increases. Thus, as we look further into the future, we see a higher degree of compensation to cover this ever-increasing risk.

So while there are different segments along the yield curve, each segment is not independent from other segments. This interconnection comes from arbitrage. If an investor is able to make more money in one segment, he can easily sell in one area and buy in another. Thus, the yield curve is interconnected through supply, demand and arbitrage. An inverted yield curve is where the short-term rates are higher than the long-term rates, i.e., it is downward sloping.

Where are we now?

Is it true that the yield curve has inverted? The answer to this is like many answers in economics, it is both a “Yes” and a “No”. On August 5, 2019, the daily rate of the 10-year bond fell to 1.75%, while the 1-year bond rose to 1.78%. (Incidentally, the 2-year bond, which the press was talking about, has not closed above the 10-year rate between August 1 and August 26, 2019.) According to the US Treasury, the 1-year bond has closed above the 10-year bond every day since August 5th, but the largest gap has only been 0.21%. Additionally, the 10-year rate has closed less than the 3-month rate every day since the middle of May 2019 (with the lone exception of July 23, 2019). So right now, I would say that the yield curve is flat, but it has been trending toward an inversion for quite some time.

Why does any of this matter?

If we strictly look at the data, we see that an inverted yield curve is an excellent predictor of an oncoming recession. However, there is a difference in the types of data that we use. On any particular day, anything can happen. For example on August 21, the last place Detroit Tigers beat the Houston Astros (with Justin Verlander pitching) with baseball’s biggest upset in 15 years (odds were between +435 and +560 for Houston). The point is a daily number is too erratic to make meaningful predictions. As a result, I use monthly averages.

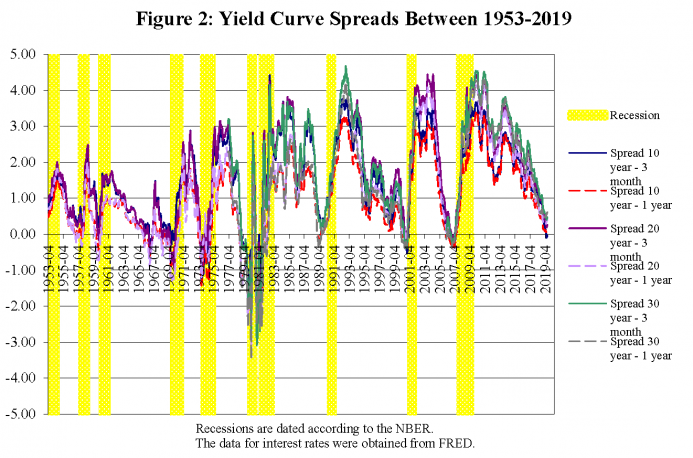

If we look at the monthly data, we see that prior to every recession since 1955, the yield curve inverted four to six quarters prior to the onset of the recession. See Figure 2.

In Figure 2, the yellow vertical bars represent recession. The lines are the differences between the various long-term rates (10, 20 and 30 years) and the two short-term rates (3 months and 1 year). When the difference falls below zero, the yield curve has inverted.

Now the real question is whether there are any false positives, where the difference is less than zero and there is no yellow bar. The answer is yes, there was one in 1966-67. However, depending on which dataset one looks at, there was either one quarter of negative growth (or nearly negative) in 1967. Recessions are typically categorized by at least two quarters of negative growth and so I believe that the relationship holds.

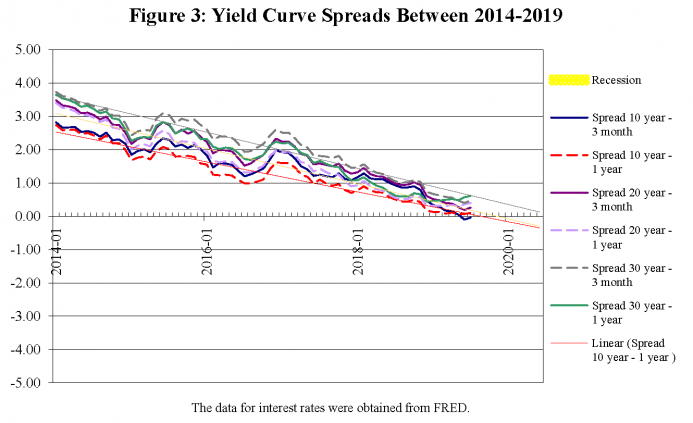

If we take a closer look at the yield curve spread and add some straightline projections, we get Figure 3.

What we see here is that whole curve is flattening. Furthermore, if everything continues along these straight lines (which never actually happens) we should expect to see the yield curve truly invert around October or November of 2019. And if history follows the past, we should then expect to see the economy in a recession 4 to 6 quarters later, meaning that somewhere between October 2020 (around election time) and April 2021, the economy will be contracting.

Is this a fait accompli? Is this story written in stone? By all means, “No.” History may rhyme, but it is not fatalistic. To understand where we are headed, we need two things, the facts and, secondly, the context within to put the facts in order to understand them. In other words, we need some data and a theory.

The Data

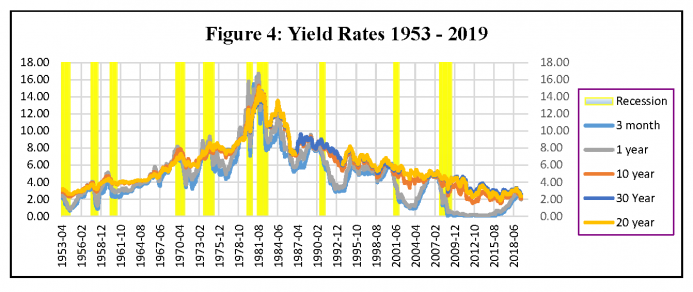

To start, we will take a look at the monthly rates of US Treasuries from 1953 until August 2019. See Figure 4.

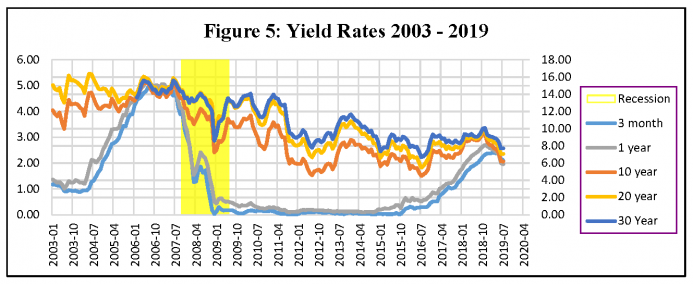

Figure 5 shows a close up view between 2003 and August 2019.

What we see is that while the long-term rates have come down a little bit, it is jump in the short-term rates has flattened and may eventually invert the yield curve. It appears that by 2016, the increase in short-term rates was well underway.

The next question that we should be asking is, “What is it that is driving up short-term rates?” In order to find the answer, we first need to know where to look and that knowledge comes from economic theory.

The Theory

In 2004, I finished my dissertation examining the relationship between the yield curve and economic downturns. What I found is that this is a very complex relationship. The reason why short rates are changing is simply due to changes in supply and demand. The difficulty lies in tracing those root causes of these changes. In order for the short-term rates to climb, there must either be a decrease in the supply of loanable funds, an increase in the demand for loanable funds, or a combination of both forces.

Is there a decrease in the supply of short-term funds on the market? While the Fed has been engaged in some monetary tightening, interest rates have been at historically low levels since 2008. (Take another look at Figure 5 above and focus on the short-term rates between 2009 and 2016.) Furthermore, in July the FOMC (the Federal Open Market Committee sets the targets for short-term interest rates) officially reversed course and announced lowered the targeted rates from the 2¼ – 2½% range to the 2 – 2 ¼% range. So, it is safe to say that it rise in short-term interest rates is not really a function of tightening supply. Thus, it must be a function of demand.

The question we need to next investigate is, “Why is there more demand for Short-term Loanable funds?” It is here that things become complex. We must first start with the Austrian Business Cycle Theory (ABCT).

The ABCT says that economic recessions can be caused by an expansion of artificial credit. This expansion leads to relative decrease in the interest rate (yes, we are assuming a single interest rate here). The relative decrease in the interest rate will cause several things. First, it will cause a shift from savings towards consumption. Secondly, it will not simply cause an increase in investment spending (overinvestment), but it will also cause a misdirection of the capital spent (malinvestment).

As the credit expansion follows its course, it causes an artificial economic boom. During the boom, there is expansion throughout the entire economy, however there are concentrations in two particular sections of the economy: the early stages and the final stages of the production process. The early stages are where we are clearing land and pouring concrete foundations. As a result, if we make a mistake, these can become very costly. The final stages of economic production are those closest to the consumers. While these later stages are also subject to the business cycle, the severity of fluctuations at these stages are less than those of the earlier stages.

In my dissertation and in a subsequent article, I argue that as we near the peak of the economic expansion, profit margins will be squeezed by rising input prices. As input prices climb, businesses will seek short-term financing to complete their projects.

An Illustration

Suppose that you are a home builder and the interest rate stands at 6% (as it did in 2001). You have looked at the market and expect the return on your building and selling of homes will yield a 4% rate of return. Of course, you do not put your money into this project.

Now suppose that the interest rate has fallen from 6% to 1% (as it did in 2003). What will you do? If you do nothing, your competitors will leave you standing in the dust. You must keep up with your competitors and thus you choose to invest. Suppose that while you want to make 6 houses, there are only enough bricks for 4. Can you start 6 foundations? Yes, of course. No one in the economy really knows how many “bricks” (available resource inputs) exist in the current and near future economy. And so as an entrepreneur, you follow the market signals and start 6 foundations. As you and your competitors start to use the bricks, the price of these bricks starts to climb. As the price of bricks climbs, the funds at your disposal no longer cover the costs of completing the 6 houses. Without getting the bricks, the houses will remain incomplete and the project will be a huge loss. It is imperative that your company gets those bricks. And so your home building company is willing to borrow short-term money at higher and higher rates in order to complete something and reap at least a little return from the project.

Back to the Data

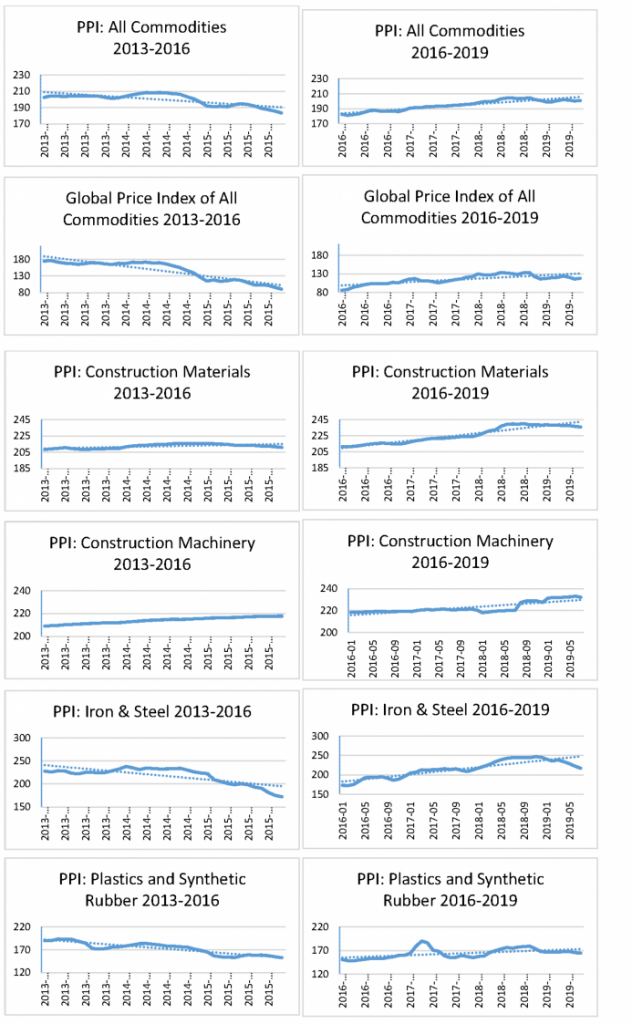

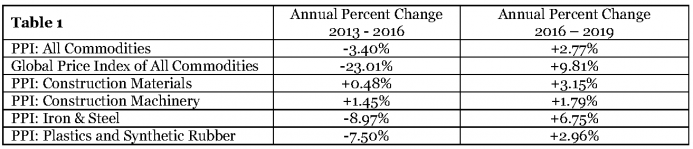

So according to the theory outlined above, we are positing that the interest rates are climbing in the short-run because of input price increases, which are squeezing profit margins. So, the next step is to look at input prices. Unfortunately, the data that is collected by US governmental institutions were designed from a Keynesian perspective. Thus, the data that an Austrian would like to look at doesn’t really exist, at least not in a format that we would prefer. Nevertheless, there are some general statistics that we can use. I have pulled six statistics from the Federal Reserve Economic Data which pertain to commodity prices: PPI: All Commodities, Global Price Index of All Commodities, PPI: Construction Materials, PPI: Construction Machinery, PPI: Iron and Steel, and PPI: Plastics and Synthetic Rubber.

If we look at the short-term interest rates in Figure 5, we see that they start to climb in 2016. What does tracking these commodity prices from 2016 through 2019 show us? In each category we see prices rising, just as the theory predicts. Furthermore, if we look three years before 2016 and examine the range between 2013 and 2016, what do we see? As summarized in Table 1 below, in four of the six categories, the prices were falling. The two categories were the prices were increasing (PPI: Construction Materials and PPI: Construction Machinery), we see that the rate of increase has accelerated after 2016.

What should we look for next?

The takeaway from the analysis so far is that we are coming to the end of an economic boom and nearing the upper turning point of the business cycle. The next phase in the business cycle is business failures and bankruptcies. According to the ABCT, the areas that we should be looking for bankruptcies are in the early stages of production.

There are some signs that bankruptcies are increasing. We can see that there is a lot of economic distress in the farming sector, but this might be more the result of the trade tariffs than the normal course of the business cycle. The Chinese know that a lot of political support for President Trump lies within the agricultural community and so they have specifically targeted their trade tariffs on this constituency group.

The overall point is that the data is not yet clear. In fact, it is probably a little too early in the business cycle for a disproportionate amount of bankruptcies. Bankruptcies occur all the time, in both good and bad economic times. So, as the yield curve inverts over the next several weeks or months, we should expect to see a steadily rising amount of bankruptcies until we make the turn and the bottom falls out.

What can be done to mitigate the next recession?

Many people believe that the higher you go, the greater the fall. When it comes to business cycles, it is simply not the case. We can have a small upswing and a dramatic collapse, a large upswing followed by a mild recession, or anything in between. The key market factor in determining the level of economic decline is the amount of savings. Simply put, the larger the amount of savings, the smaller the downturn will be. Thus, anything that can be done to stop discouraging savings should be done. This is not to say that government should force savings to occur, but every policy where the government is currently encouraging spending over savings should be stopped. For example, when the government decides to increase spending to stimulate consumption, it is shifting funds that would have been otherwise saved into spending. The policies that the government enacts during the downturn will strongly affect the size and duration of the collapse. Misguided policies, such as stimulus spending, actually prolong an economic downturn and delay a full recovery.

Nevertheless, there are steps we can take that encourage savings. Here are three examples. First, we can cut the capital gains tax. Savings are actually deferred consumption. Since retained earnings are a form of deferred consumption, they are a type of savings. So any policy that taxes or discourages retaining earnings should be abolished. Secondly, if the US changes from the income tax to a consumption tax, there would be a disincentive to spend and thus a relative incentive to save. And third, if the US Federal Government balanced budget by cutting spending, there would be an encouragement of savings. Currently, the US Federal Government is borrowing money to finance its spending. These “saved” funds are not actually saved, but spent by the US government. By cutting the amount that the government spends, these funds will shift back into the private sector as investment funds.

Furthermore there are some additional steps that we could take to mitigate the recession. First, we need to recognize that the artificial bubble was caused by the expansion of the money supply. We need to stop this inflation. Denationalizing and deregulating the money supply would be a step in the right direction.

Secondly, we could make the bankruptcy process easier. The way in which we turn a recession into a recovery is by clearing out the misaligned capital structures and converting the malinvestments into proper investments. In the last downturn, the Federal Government bailed out General Motors. Suppose, instead, what would have

happened if it did not bail out GM. GM would have gone bankrupt. It would have had to sell its assets to generate cash to pay its creditors. Thus, GM would have had to sell Cadillac and Corvette. Of course, Cadillac is not worth zero dollars. There would be buyers for Cadillac, maybe Ford or Toyota or Elon Musk. Whoever the ultimate buyer would be, that buyer would not have to pay top dollar for Cadillac (it is a going-out-of-business sale). This new owner could then, on the very next day, turn on the very same machines, produce the very same car, and sell it at the very same price. However, this new owner would be able make a profit where old GM could not. Why? It is because this new owner has a lower cost structure. The new owner bought the capital in a fire sale. This process is how we convert a recession into a recovery. Thus, by making the bankruptcy process easier and faster, the economy can realign itself more quickly. If we continue to follow this logic, if we also make mergers and acquisitions easier, we can reduce both the depth and the duration of the recession.

Many people have claimed that the Austrian approach leads government officials to “do nothing” in the face of a recession. When the people are clamoring for “something to be done” the Austrians say, “No.” But this this is simply an empty charge. Outlined above are several positive steps that can be taken to reduce the size and scope of the recession.

I do not know when we will reach the upper-turning point and start the economic slide into recession. From this analysis, I can say that it is coming. If history follows the same path, then sometime between October 2020 and April 2021, we should be in a recession. The questions of how long it will last and how deep it will get depend upon our response and the policies we enact. Since we know it is coming, we can prepare. We can curb our personal spending and accumulate savings. We have at least a little time to prepare.

*About the author: Paul Cwik is Professor of Economics and Finance at the University of Mount Olive and Teaching Assistant Professor of the BB&T courses in Free Market Economics at North Carolina State University.

Source: This article was published by the MISES Institute

Like what you read?

Please consider supporting Eurasia Review. Thank you for your consideration!

We have been in a recession for quite a while according to many economists.