Seeking Safety Abroad: The Hidden Story In China’s FDI Statistics – Analysis

The Chinese prefer investing overseas; dummy companies may ease transfers and devalue renminbi.

By Farok J. Contractor*

China’s sinking stock market and the government’s assiduous efforts to shore it up have been reported at length. Traders and exporters follow the gyration of the renminbi exchange rate following China’s loosening of the trading bands, allowing more fluctuation in value.

However, growing capital flight from China raises questions about the renminbi becoming a reserve currency.

The global panic in financial markets in August was catalyzed by the relatively sudden devaluation of the Chinese yuan – from 6.2 to 6.4 renminbi per dollar. The Chinese government may have had several reasons for setting the daily reference rate for the currency at a lower level – to signal greater market flexibility or to support exporters. However, the fact is that enormous amounts of liquid money held by Chinese individuals and companies have, for many years, been anxiously trying to leave China and the renminbi as an asset, and instead park in non-Chinese assets such as condominiums in Manhattan or Sydney, US stocks, Singapore bank accounts or simply luxury goods. That created the devaluationary pressure in the exchange markets.

China is getting richer, and by some accounts China may already be coequal with the United States as the world’s largest economy, if one considers the World Bank’s implicit estimate for the PPP theoretical exchange rate for the renminbi, below 4 per dollar.

In short, there are hundreds of billions of dollars’ worth of liquid assets trapped inside China – trapped because current rules do not allow Chinese to convert their renminbi into other currencies unless there is a commercial justification.

A company or individual cannot just go to a bank in China with renminbi and ask that they be converted into, say, US dollars. The bank would refuse the request unless the customer can show documentary proof that he or she is a sanctioned importer, a child’s tuition in a university overseas needs to be paid, or a foreign subsidiary of a Chinese firm is in need of funds.

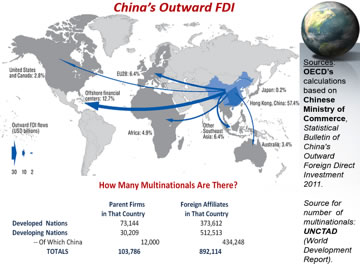

One stratagem likely used by Chinese companies to get permission to remove funds from China is to create dummy companies in Hong Kong and the Caribbean. As far back as 2011, the Organization of Economic Cooperation and Development reported that as much as 57.4 percent of all outbound foreign direct investment capital went to Hong Kong affiliates or subsidiaries and another 12.7 percent to Caribbean entities. By contrast, Chinese companies’ outflow of foreign direct investment capital to invest in European or US affiliates directly totaled a mere 8.2 percent.

That means that as much as 70.1 percent of Chinese outbound FDI capital flows, exceeding $100 billion per year since 2011, has gone to two tiny economies, the Caribbean and Hong Kong. Moreover, data gleaned from UN Conference on Trade and Development show a suspiciously large number of Chinese FDI-affiliated companies outside China. For the world as a whole, the number of multinational companies – headquartered mainly in North America, Europe and Japan – totaled 103,786. Of these, the UN data show 12,000 – or 11.6 percent of all multinational firms in the world – as headquartered in China. This appears plausible, as Chinese companies are indeed increasing their global reach. But then, the number of foreign affiliates or subsidiaries of Chinese companies is said to total a remarkable 434,248 in number – 48.7 percent of the world total.

If this is to be believed, Chinese multinational parents each had as many as 36 foreign subsidiaries or affiliates, as against the rest of the world whose multinational parent firms averaged only five foreign subsidiaries. With a 2,000-year-old bureaucracy, the Chinese do keep meticulous data, and the numbers appear to be authentic. But they reveal a hidden story, that a significant fraction of the Chinese company subsidiaries in the Caribbean and Hong Kong are mere shell companies. Many of these dummy companies are likely created for a principal reason, to create a justification for the conversion of renminbi into foreign currencies – in short, to facilitate a hidden capital outflow not really intended for business purposes, but to remove money from China on behalf of the owners.

If this is to be believed, Chinese multinational parents each had as many as 36 foreign subsidiaries or affiliates, as against the rest of the world whose multinational parent firms averaged only five foreign subsidiaries. With a 2,000-year-old bureaucracy, the Chinese do keep meticulous data, and the numbers appear to be authentic. But they reveal a hidden story, that a significant fraction of the Chinese company subsidiaries in the Caribbean and Hong Kong are mere shell companies. Many of these dummy companies are likely created for a principal reason, to create a justification for the conversion of renminbi into foreign currencies – in short, to facilitate a hidden capital outflow not really intended for business purposes, but to remove money from China on behalf of the owners.

It’s true that a fraction of the mainland China foreign direct investment outflows that go to Hong Kong affiliates return to the mainland for investment purposes in a “round trip.” A Hong Kong company can pose as a “foreign” investor and enjoy benefits such as cheap land that a purely domestic investor may not get. Other Hong Kong affiliates may be intended to mitigate the perceptual drawback of an investor’s origin from mainland China. But some unknown, yet significant fraction of the outward FDI emanating from China and going to Hong Kong – plus most of the outflows going to Caribbean havens – is intended so that owners can transfer money for tax benefits, or to invest in foreign bank accounts, equities or properties.

In 2015, Chinese purchasers topped the list of foreign buyers of Australian and US real estate. In the 12 months up to March 2015, the Financial Times reported that Chinese buyers spent $28.6 billion to buy US property and that Chinese are the top buyers of housing in New York, Vancouver, London, Sydney and Auckland. Hundreds of multimillion dollar Manhattan apartments lie empty, functioning merely as an investment for wealthy foreign buyers.

The Chinse are not alone. The world is awash in liquidity – cash and quickly sellable assets conservatively estimated at $75 trillion and likely exceeding $100 trillion worth – following the global debt crisis in 2007 and the rounds of stimulus spending. Worldwide, mutual fund assets alone exceed $30 trillion, according to the 2014 Investment Company Factbook, with probably double that amount in bank or similar deposits.

It’s a thrilling story. Up to 2 billion of humankind have become affluent enough to have investable savings. But the worldwide flood of money is seeking places for investment, safety and growth. And in a global arena, this means the need to convert from one currency to another. When there is sudden, collective rush to sell billions of one currency and buy another, exchange rates can go down sharply, despite government counter-purchases, as seen in the August devaluation of the renminbi.

The world’s 2 billion middle-class and affluent individuals are aware of investment options. Virtually all of them have an internet connnection that amplifies news reports, fears, phobias and panics. All said and done, in August there were no deep fundamental economic reasons for the simultaneous swoon of stock markets around the world. The Chinese economy is slowing down from the heady days of 10 percent or more annual growth rate to a mere 6 or 7 percent. So absurd is the news hype and consequent global angst, amplified by the internet and media, that a 7 percent growth rate – ordinarily the envy of most nations – is instead protrayed as a reason to sell assets. Similarly absurd is the portrayal of a mere 3 percent devaluation of the renminbi as a cause for panic, selloffs and crashes.

A global civilization that is intimately interconnected, awash in liquidity, is one prone to collective global psychology, manias and herd instinct. Prepare for more thundering hooves and market gyrations.

*Farok Contractor is a professor in the Management and Global Business Department at Rutgers Business School. He has researched foreign direct investment for three decades and has also taught at the Wharton School, Copenhagen Business School, Fletcher School of Law and Diplomacy, Tufts University, Nanyang Technological University, Indian Institute of Foreign Trade, XLRI (India), Lubin School of Business, Theseus, EDHEC and conducted executive seminars in the US, Europe, Latin America and Asia.

Like what you read?

Please consider supporting Eurasia Review. Thank you for your consideration!