Money Supply Has Plummeted In Biggest Drop Since The Great Depression – Analysis

By Ryan McMaken*

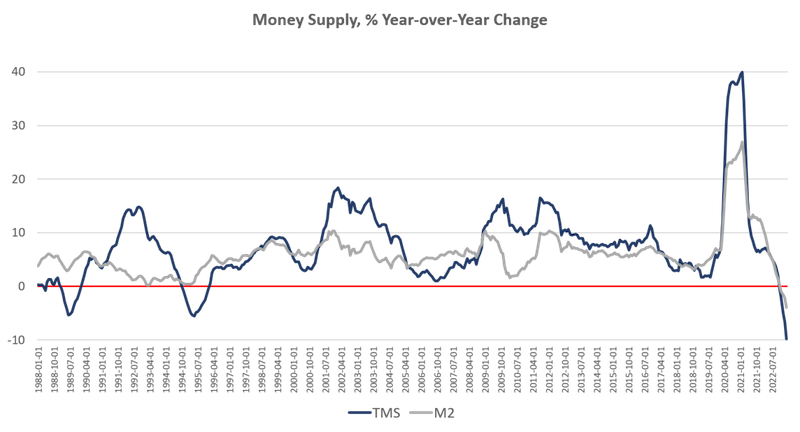

Money supply growth fell again in March, plummeting further into negative territory after turning negative in November 2022 for the first time in twenty-eight years. March’s drop continues a steep downward trend from the unprecedented highs experienced during much of the past two years.

Since April 2021, money supply growth has slowed quickly, and since November, we’ve been seeing the money supply repeatedly contract for five months in a row. The last time the year-over-year (YOY) change in the money supply slipped into negative territory was in November 1994. At that time, negative growth continued for fifteen months, finally turning positive again in January 1996.

During March 2023, the downturn accelerated as YOY growth in the money supply was at –9.9 percent. That’s down from February’s rate of –6.6 percent, and far below March’s 2022’s rate of 7.1 percent. With negative growth now falling to near –10 percent, money-supply contraction is the largest we’ve seen since the Great Depression. At no other point for at least sixty years has the money supply fallen by more than 6 percent (YoY) in any month.

The money supply metric used here—the “true,” or Rothbard-Salerno, money supply measure (TMS)—is the metric developed by Murray Rothbard and Joseph Salerno, and is designed to provide a better measure of money supply fluctuations than M2.

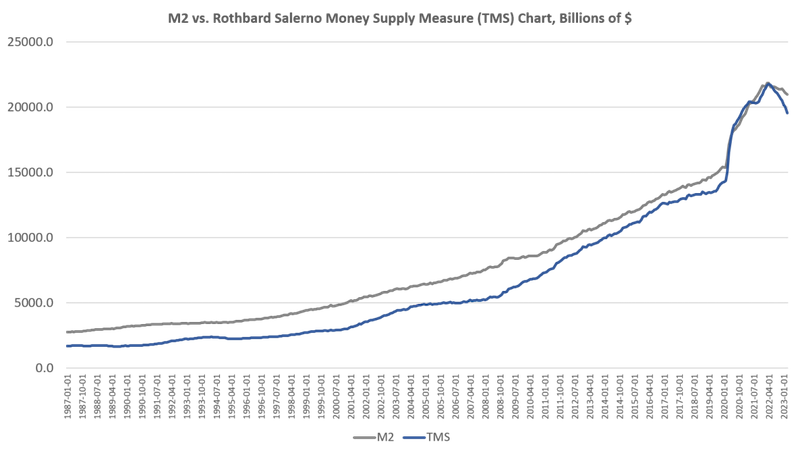

The Mises Institute now offers regular updates on this metric and its growth. This measure of the money supply differs from M2 in that it includes Treasury deposits at the Fed (and excludes short-time deposits and retail money funds).

In recent months, M2 growth rates have followed a similar course to TMS growth rates, although TMS has fallen faster than M2. In March 2023, the M2 growth rate was –3.99 percent. That’s down from February’s growth rate of –6.65 percent. March’s growth rate was also well down from March 2022’s rate of 9.6 percent.

Money supply growth can often be a helpful measure of economic activity and an indicator of coming recessions. During periods of economic boom, money supply tends to grow quickly as commercial banks make more loans. Recessions, on the other hand, tend to be preceded by slowing rates of money supply growth.

Negative money supply growth is not in itself an especially meaningful metric. But the drop into negative territory we’ve seen in recent months does help illustrate just how far and how rapidly money supply growth has fallen. That is generally a red flag for economic growth and employment.

The fact that the money supply is shrinking at all is so remarkable because the money supply almost never gets smaller. The money supply has now fallen by $2.2 trillion (or 10.2 percent) since the peak in April 2022. Proportionally, the drop in money supply since 2022 is the largest fall we’ve seen since the Depression. (Rothbard estimates that in the lead up to the Great Depression, the money supply fell by 12 percent from its peak of $73 billion in mid-1929 to $64 billion at the end of 1932.)1

In spite of this recent drop in total money supply, money-supply growth remains well above the trend that existed during the twenty-year period from 1989 to 2009. To return to this trend, the money supply would have to drop at least another $5 trillion or so—or 25 percent—down to a total below $15 trillion.

Since 2009, the TMS money supply has grown by nearly 200 percent. (M2 has grown by 145 percent in that period.) Out of the current money supply of $19.5 trillion, $5.2 trillion of that has been created since January 2020—or 27 percent. Since 2009, $12.9 trillion of the current money supply has been created. In other words, two-thirds of the money supply have been created over the past thirteen years.

With these kinds of totals, a ten-percent drop only puts a small dent in the huge edifice of newly created money. The US economy still faces a very large monetary overhang from the past several years, and this is partly why after nine months of slowing money-supply growth, we are not yet seeing a sizable slowdown in the labor market.

Nonetheless, the monetary slowdown has been sufficient to considerably weaken the economy. Home prices have fallen. Credit card debt has soared, delinquencies on loans and leases are soaring, job openings are falling, and the manufacturing outlook is falling deeper into negative territory.

Money Supply and Rising Interest Rates

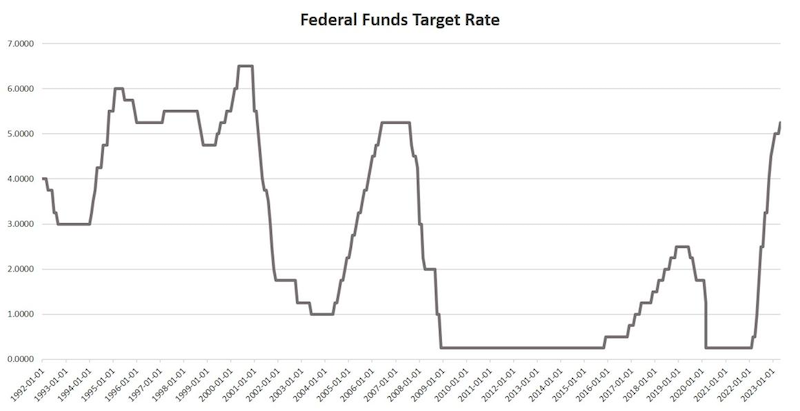

An inflationary boom begins to turn to bust once new injections of money subside, and we are seeing this now. Not surprisingly, the current signs of malaise come after the Federal Reserve finally pulled its foot slightly off the money-creation accelerator after more than a decade of quantitative easing, financial repression, and a general devotion to easy money. As of May, the Fed has allowed the federal funds rate to rise to 5.25 percent. This has meant short-term interest rates overall have risen as well. In April, for example, the yield on 3-month Treasurys is approaching the highest level measured in more than 20 years.

Without ongoing access to easy money at near-zero rates, however, banks are finding that they’re in trouble in spite of claims from Fed Chairman Jay Powell that the banking system is “sound and resilient.” In the latest Senior Loan Officer Opinion Survey from the Federal Reserve, researchers found that bankers believe lowered expectations for economic growth coupled with deposit outflows will lead to banks tightening lending standards. Banks have found that demand for loans has weakened as interest rates have increased and economic activity has slowed.

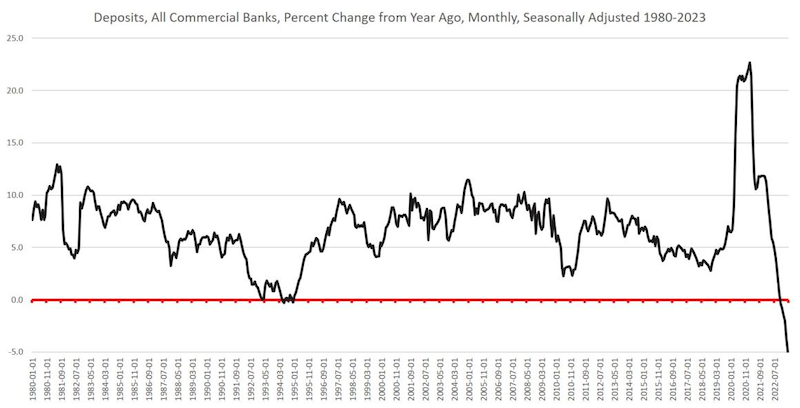

Banks have good reason to be worried. The last two months have produced a historic decline in bank deposits with April deposits falling deeper into negative territory than in any other month in more than 50 years.

There are other indications the economy is posed for recession, as well. For example, the 3s/10s yield spread remains in negative territory. This inverted yield curve is a strong predictor of coming recession, and is closely related to a falling moeny supply and rising interest rates. As Bob Murphy notes in his book Understanding Money Mechanics, a sustained decline in TMS growth often reflects spikes in short-term yields, which can fuel a flattening or inverting yield curve.

This all points toward rapidly declining economic activity in an economy where real savings and investments have been hollowed out by more than a decade of easy money. Without an economy geared toward real savings and increased productivity, ongoing monetary inflation will increasingly make price inflation worse. In this fragile economy, the Fed has therefore had to choose between rising price inflation on the one hand, and a banking system teetering on the brink in the other. Inflation fears have—for now—spurred the Fed to allow interest rates to rise, accompanied by a contracting money supply. It remains to be seen how long it will take the Fed to hit the panic button and retreat back toward easy money, spurring a continuation of this cycle of mounting price inflation.

- 1.Murray Rothbard, America’s Great Depression (Auburn, AL: Ludwig von Mises Institute, 2005) pp. 92, 302

About the author: Ryan McMaken (@ryanmcmaken) is executive editor at the Mises Institute. Send him your article submissions for the Mises Wire and Power and Market, but read article guidelines first. Ryan has a bachelor’s degree in economics and a master’s degree in public policy and international relations from the University of Colorado. He was a housing economist for the State of Colorado. He is the author of Breaking Away: The Case of Secession, Radical Decentralization, and Smaller Polities and Commie Cowboys: The Bourgeoisie and the Nation-State in the Western Genre.

Source: This article was published by the MISES Institute

Like what you read?

Please consider supporting Eurasia Review. Thank you for your consideration!