An Overview Of China’s Fiscal Policy Balancing In 2022 From The Decreasing Deficit Ratio – Analysis

By Wei Hongxu

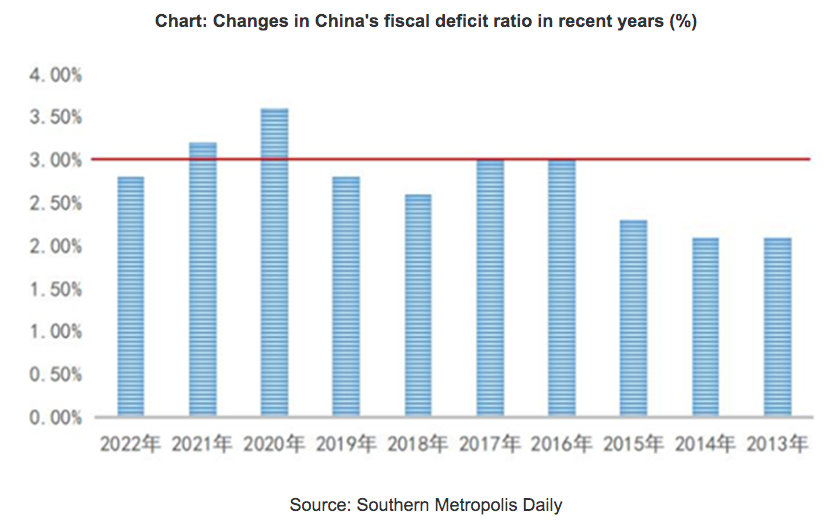

China’s Government Work Report for the year 2022 (henceforth “Work Report”) proposes that this year’s active fiscal policy should improve efficiency and focus on precision and sustainability. The deficit ratio for this year is targeted to be around 2.8%, and that would be the lowest since the outbreak of the COVID-19 pandemic. A few questions arise in this regard, for instance, how should “active” fiscal policy be reflected when the fiscal deficit ratio is declining? How can China achieve the goal of economic growth of approximately 5.5%? Researchers at ANBOUND believe that the change in the deficit ratio signifies that the market requires a more accurate understanding of the direction of fiscal policy and a better grasp on the subtle balance of fiscal policy for 2022.

The growth of China’s fiscal expenditure this year is still considerably impressive. In fact, the Work Report stated that the scale has increased by more than RMB 2 trillion compared with last year. Chinese Minister of Finance Liu Kun said at the Two Sessions that the size of the national general public budget fiscal expenditure this year is RMB 26.7 trillion, a rise of more than RMB 2 trillion over last year, being an increase of 8.4%, and 2.9 percentage points higher than the expected GDP growth ratio. According to institutional estimates, the target growth ratio of expenditures for the general finance (i.e., general budget account and government fund account) will reach 12.8%, which is much higher than the -1.0% growth ratio in 2021. These data show that the significance of China’s proactive fiscal policy lies in the expansion of the overall scale of expenditure to realize the government’s support for people’s livelihood and infrastructure. This, in turn, is an indication of the supporting role of economic growth. Furthermore, it is worth noting that the tax and cost-cutting program would be continued this year, with a total cost of RMB 2.5 trillion. These market-entity subsidies are, in reality, components of inclusive fiscal policy, and they are not reflected in the deficit ratio.

It should be noted that this year’s decrease in the general budget deficit ratio is also attributable to an increase in financial resources in several areas. According to Liu, through carryovers from previous years, the central government’s fund allocation has reached RMB 1.267 trillion, 6.6 times that of last year, equivalent to raising the deficit ratio by 1 percentage point, while the intensity of fiscal expenditure is guaranteed. In addition, certain state-owned financial institutions and franchised institutions are expected to pay a total of RMB 1.65 trillion in profits in the recent years, and these funds will support the increased intensity of fiscal expenditures. These “cross-cycle” increases in various fiscal funds compensate for fiscal revenue and minimize the fiscal deficit in 2022.

The increase in the general budget is structurally much bigger than the increase in the special debt. Last year, the scale of local special bonds remained at RMB 3.65 trillion for infrastructure investment, and part of the special bond funds carried forward from last year will be used this year. RMB 640 billion was allocated in the central budget, an increase of RMB 30 billion over last year. In comparison to the RMB 2 trillion increase in the budget and the RMB 1.5 trillion rise in central transfer payments, the overall transfer payment size increased by 18% to RMB 9.8 trillion. Noticeably, the growth in local budgeting fiscal funds is substantial. This means that the usage of budgetary funds and the allocation of expenditures will be the focus of potential fiscal expansion for local governments. These are relatively stronger than the special debt funds listed separately. This is the indication of that the degree of municipal financial support and guarantees is increasing and that the relevant public welfare investment and general expenditure should be the focus of local fiscal policy consideration.

Although the scale of fiscal expenditure has expanded, in terms of financial support for the economy, it is true that the reduction in the deficit ratio means that the intensity of fiscal support is still significantly slower than in previous years. This is precisely the significance of China’s budgetary strategy this year, which emphasizes accuracy and sustainability. Xiang Dong, deputy director of the Research Office of the State Council, said that appropriately lowering the deficit rate is conducive to enhancing fiscal sustainability. In 2020, in response to the impact of the COVID-19 pandemic, the deficit ratio was increased to more than 3.6%, an extraordinary move in an extraordinary period. With the gradual and stable recovery of the economy, the timely correction of the deficit ratio would be conducive to enhancing fiscal sustainability and leave room for dealing with any complex and difficult situations that may arise in the future. Adjusting the deficit ratio to less than 3% this year is a signal that the Chinese economic and fiscal operations are stable and such a move can boost market confidence.

The budget arrangement for this year demonstrates that the decline in China’s fiscal deficit ratio signifies the overall fiscal expansion has its own limits and provides room for economic growth. According to ANBOUND, the boundary of economic growth in fiscal spending itself is preserving the stability of the macro leverage ratio. In 2021, China’s macroeconomic policies will place a greater focus on the consistency of macro leverage ratios as the primary aim of economic stability and risk mitigation. With the economy growing at 8.1%, macro leverage actually fell by about 8 percentage points last year. This effectively means that the overall debt levels remain largely unchanged, reflecting the country’s macroeconomic policies’ emphasis on constancy. The overall idea is to maintain the leverage level and expand the denominator of economic growth so as to achieve the stability and decline of the macro leverage level. To really encourage high-quality growth, China’s economic growth will continue to stick to quality improvement rather than scale expansion.

Final analysis conclusion:

The decline in the deficit ratio in the fiscal budget arrangement indicates that China’s fiscal policy in 2022 is in a state of balance between scale growth and flexibility. In this delicate balance, fiscal policy measures may take into account the urgency of boosting efficiency as well as long-term sustainability concerns. There should be no use of excessive force or inaction; instead, an equilibrium between speed and size should be maintained.

Like what you read?

Please consider supporting Eurasia Review. Thank you for your consideration!

The financials of China s govt? Wise to invest in China?