Saudi Arabia Energy Profile: Second Largest Holder Of Proved Oil Reserves – Analysis

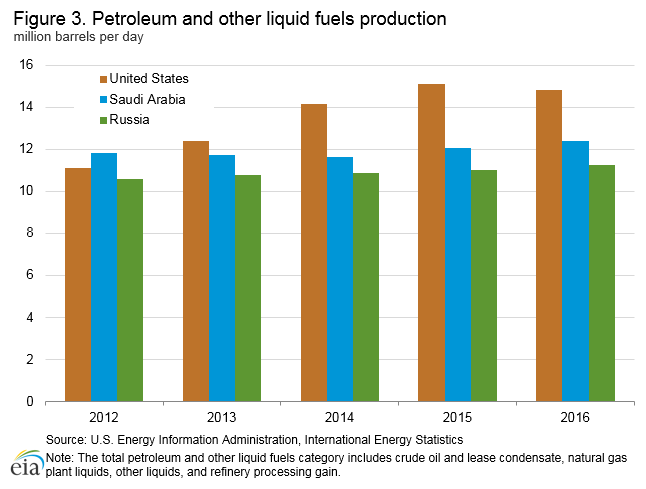

Saudi Arabia is the world’s second-largest holder of proved oil reserves, ranking second only to Venezuela, holding roughly 16% of total reserves. In 2016, Saudi Arabia was the largest exporter of total petroleum liquids (crude oil and petroleum products), with exports mostly destined to Asian and European markets. During that same year, Saudi Arabia was the world’s second-largest petroleum liquids producer behind the United States and was the world’s second-largest crude oil and lease condensate producer behind Russia. During the first half of 2017, Saudi Arabia has maintained this position, despite lower production than in the previous year.

Saudi Arabia’s economy remains heavily dependent on petroleum exports, which accounted for nearly 75% of total Saudi export value in 2016.[2] According to the International Monetary Fund (IMF), about 60% of Saudi government’s revenues are oil-based, and the real GDP growth rate fell significantly in 2016, as a result of the slowdown in oil-driven growth that year.[3] Saudi Arabia’s oil revenues have fallen dramatically as crude oil prices have decreased since mid-2014. EIA estimates that Saudi Arabia’s net oil export revenues totaled $133 billion in 2016, compared with $159 billion (in 2016 dollars) in 2015 when Saudi Arabia boosted production and exports to record highs. Despite the increase in output, Saudi Arabia’s net oil revenues in 2015 saw dramatic decrease compared with 2014, when the country was estimated to have earned $301 billion (in 2016 dollar).

In addition to continued investment in maintaining its crude oil production capacity, Saudi Arabia has also invested considerable resources to develop its natural gas, refining, petrochemicals, and electric power industries. The country’s natural gas and electric power industries, in particular, are geared to meet increasing domestic demand. Investments in refining and petrochemical industries aim to improve Saudi Arabia’s ability to compete internationally in these sectors.

Saudi Arabia’s oil and natural gas operations are dominated by Saudi Aramco, the national oil and gas company, which is the world’s second-largest oil company in terms of production (behind Russia’s Rosneft). Saudi Arabia’s Ministry of Petroleum and Mineral Resources and the Supreme Council for Petroleum and Minerals oversee the oil and natural gas sector and Saudi Aramco.

In 2016, Saudi Arabia announced that it will undertake a national transformation called Vision 2030, encompassing both cultural, governance, and economic aspects of Saudi society. On the economic front, Vision 2030 plans to make the kingdom less dependent on income from oil production by broadening the economic base. The plan outlines far-reaching reforms of the energy sector and includes the partial privatization of state-owned Saudi Aramco, planned for the second half of 2018. Income from Saudi Aramco’s initial public offering (IPO) would be used to help finance the economic transition.

Saudi Arabia is located near two of the world’s busiest chokepoints, and most of its crude oil and petroleum liquid exports travel through them. The Strait of Hormuz, which connects the Persian Gulf with the Gulf of Oman and the Arabian Sea, is the world’s most important chokepoint. The oil flow of 17 million barrels per day (b/d) in 2015 through this strait accounts for about 30% of all seaborne-traded crude oil and other liquids during the year. In 2016, total flows through the Strait of Hormuz increased to a record high of 18.5 million b/d. This strait is an important route for the Persian Gulf countries for oil and liquefied natural gas exports.

Another regional chokepoint, Bab el Mandeb, links the Gulf of Aden and the Red Sea. This waterway is a strategic link between the Mediterranean Sea and the Indian Ocean. An estimated 4.8 million b/d of crude oil and refined petroleum products flowed through this waterway in 2016 toward Europe, the United States, and Asia.

Energy consumption

According to the BP Statistical Review of World Energy 2017, Saudi Arabia was the world’s 10th largest consumer of total primary energy in 2016 at 266.5 million tons of oil equivalent, of which about 63% was crude oil and petroleum liquids-based. Natural gas accounted for nearly all of the remaining 37% of consumption. Domestic consumption growth has been spurred by the economic expansion in the wake of historically high oil-related revenues that persisted until mid-2014. Further, large fuel subsidies, which reportedly cost the Saudi government an estimated $61 billion in 2015, have led to demand growth of about 7% per year between 2006 and 2016.[4] Despite crude oil revenues falling from historic highs in 2014, Saudi Arabia’s energy consumption has grown steadily mainly as a result of the subsidies.

Saudi Arabia is the largest consumer of petroleum in the Middle East, particularly in the area of transportation fuels and direct crude oil burn for power generation. Although transportation demand is substantial and growing, an increasing share of crude oil demand is attributable to direct crude oil burn for electric power generation, which can reach as high as 900,000 b/d during summer months.[5] Crude oil and petroleum liquids reserves in the country remain plentiful, but Saudi Arabia is looking to diversify its mix of fuels for electric power generation, focusing on natural gas, nuclear, and renewable energy solutions.

Petroleum and other liquid fuels

More than half of Saudi Arabia’s oil reserves are contained in eight fields. Saudi Arabia is home to the largest onshore and offshore fields in the world: the giant Ghawar field, the world’s largest oil field, with estimated remaining reserves of 75 billion barrels and Safaniyah, the largest offshore field, with 35 billion barrels of remaining reserves.

Reserves

According to the Oil & Gas Journal (OGJ), Saudi Arabia had approximately 266 billion barrels of proved oil reserves as of January 1, 2017, amounting to 16% of the world’s proved oil reserves.[6] Although Saudi Arabia has about 130 major oil and natural gas fields, more than half of its oil reserves are contained in nine fields in the northeast portion of the country.[7] The giant Ghawar field is the world’s largest oil field in terms of production and total remaining reserves. The Ghawar field has an estimated remaining proved oil reserves of 75 billion barrels,[8] more than the reserves of all but seven other countries. Safaniyah, the world’s largest offshore field, holds an estimated 35 billion barrels of remaining reserves.[9]

Saudi Arabia has half of the estimated 5 billion barrels of total proved oil reserves located in the Saudi-Kuwait Partitioned Neutral Zone (PNZ). The PNZ is the area between the borders of Saudi Arabia and Kuwait that was established in 1922 to settle a territorial dispute between the two countries. The Neutral Zone reserves are divided equally between the two countries.

Consumption

Saudi Arabia is the largest oil-consuming nation in the Middle East. Saudi Arabia consumed 3.9 million barrels per day (b/d) of oil in 2016. Oil consumption grew by 7% per year on average between 2006 and 2016, mainly as a result of strong economic growth and government-subsidized energy prices.[10]

Other contributing factor to this growth is sizeable direct burn of crude oil for power generation, which peaked at an average monthly crude burn rate of 900,000 b/d in July 2014. Direct crude burn in the summer months (June-September) averaged more than 700,000 b/d from 2014 and 2016, according to the Joint Oil Data Initiative (JODI). Crude oil burn for electric power generation has fallen during summer months in 2016 and so far in 2017, compared with year-earlier levels, which has freed up crude oil for exports and refining. The recent downward trend occurred when the Wasit gas processing plant commenced operations in 2016, making more natural gas available for power generation, and as energy efficiency measures resulted in lower demand.

The growth in oil consumption since 2006 was also driven by the use of natural gas liquids (NGL) in the country’s growing petrochemical sector.

Production

Saudi Arabia produced, on average, 12.4 million b/d of petroleum liquids in 2016, of which 10.5 million b/d was crude oil and about 2.0 million b/d was non-crude liquids. Total petroleum liquids production rose by 300,000 b/d in 2016 compared with 2015, marking the second year in a row of robust growth in output. Saudi Arabia’s production saw increases in 2015 and 2016 as it adopted a strategy of defending its market share in response to increased non-OPEC production, particularly from countries in North America. Saudi Arabia’s crude oil production has been lower since the beginning of 2017 compared with previous years as a result of the late-2016 OPEC agreement that capped collective crude oil output at 32.5 million b/d. Saudi Arabia’s production target was set 10.06 million b/d.

Saudi Arabia maintains the world’s largest crude oil production capacity, estimated to have reached about 12 million b/d[11] at the end of 2016. Saudi Arabia currently has no plans to increase oil production capacity; however, Saudi Aramco seems to be moving forward with upstream investments to sustain the current level of production capacity. Saudi Arabia’s long-term goal is to further develop its lighter crude oil potential and to maintain current levels of production by offsetting declines in mature fields with newer fields and by expanding projects in existing fields, such as the Shaybah and Khurais fields.[12]

Saudi Aramco also plans to expand a number of its offshore fields by the end of this decade. Zuluf, Marjan, and Berri are the main targets of the expansion. Zuluf and Marjan produce about 1.2 million b/d, while Berri’s output averages at about 300,000 b/d. Expansion of these fields will reportedly add heavier grades of oil, replacing lighter grades from the older fields.[13]

Oil production capacity in the PNZ was about 600,000 b/d in 2015, all of which was divided equally between Saudi Arabia and Kuwait. However, production averaged roughly 500,000 b/d right before the shutdown of output at the Khafji field in October 2014. Production in the PNZ production was halted in May 2015 and it remains shut in at the time of writing. Onshore production in the PNZ centers on the Wafra oil field, which began producing oil at the end of 1953. Wafra is the largest of the PNZ’s onshore fields, with approximately 4.9 billion barrels in estimated recoverable reserves, and is considered a super-giant heavy oil field.

Although Saudi Arabia’s crude oil production is subject to OPEC production targets, non-crude liquids are not subject to OPEC quotas or targets, and production in the country is at full capacity.

Saudi crude streams

Saudi Arabia produces a range of crude oils, from heavy to super light. Of Saudi Arabia’s total crude oil production capacity, more than 70% is considered light gravity, with the remaining crude oil considered medium or heavy gravity.[14] Lighter grades generally are produced from onshore fields, while medium and heavy grades come mainly from offshore fields. Most Saudi oil production, except for the Arab Light and Arab Super Light crude oil types, is considered sour (containing relatively high levels of sulfur). Saudi Aramco said that its oil fields do not require the use of enhanced oil recovery (EOR) techniques, although fields in the PNZ could require steam flooding. In 2015, Chevron was developing a full-field steam flood injection EOR project to offset field declines and to boost production of the heavy oil play. However, because of the dispute between Saudi Arabia and Kuwait and Chevron’s difficulty in securing work and equipment permits, Chevron’s activities in the PNZ have stopped.[15]

Saudi Aramco continues to drill at existing fields to help compensate for the natural declines from the mature fields.[16]

| Field | Location | Production capacity as of 2017 (million b/d) | Crude grade |

|---|---|---|---|

| Ghawar | onshore | 5.8 | Arab Light |

| Safaniya | offshore | 1.2 | Arab Heavy |

| Khurais | onshore | 1.2 | Arab Light |

| Manifa | offshore | 0.9 | Arab Heavy |

| Shaybah | onshore | 1 | Arab Extra Light |

| Qatif | onshore | 0.5 | Arab Light |

| Khursaniyah | onshore | 0.5 | Arab Light |

| Zuluf | offshore | 0.68 | Arab Medium |

| Abqaiq | onshore | 0.4 | Arab Extra Light |

| Source: Saudi Aramco, Arab Oil and Gas Journal, IHS Markit |

Oil processing

Saudi Aramco operates the world’s largest oil processing facility and crude oil stabilization plant in the world at Abqaiq, in eastern Saudi Arabia. The plant has a crude oil processing capacity of more than 7 million b/d. The plant processes the majority of Arab Extra Light and Arab Light crude oils, as well as natural gas liquids (NGL). The facility’s infrastructure includes pumping stations, gas-oil separation plants (GOSPs), hydro-desulphurization units, and an extensive network of pipelines that connects the plant to the ports of Jubail, Ras Tanura, and Yanbu (for NGL).[17] The Abqaiq processing plant is a vital part of Saudi oil infrastructure. Most of the oil produced in the country is processed at Abqaiq before export or delivery to refineries.

Refining and petrochemicals

According to OGJ, Saudi Arabia has nine domestic refineries, with a combined crude oil throughput capacity of about 2.9 million b/d.[18] Saudi Aramco operates six of the nine refineries exclusively, and the remaining three are joint ventures. Saudi Arabia continues to integrate its refinery projects with large petrochemicals complexes in what has been described as petrochemical cities.

Saudi Aramco is working to expand domestic refinery capacity. The company is developing the 400,000 b/d Jazan refinery project in southwest Saudi Arabia, which will be able to process Arab Heavy and Arab Medium crude oils. As of July 2017, construction of the refinery was 55% completed. According to Saudi Aramco, the pre-commissioning activities are scheduled to begin in mid-2018, once the associated marine terminal is completed. Saudi Aramco is also reportedly near completion of the expansion of its integrated Petro Rabigh Refinery and petrochemical joint venture, which has a capacity of 400,000 b/d.[19]

| Name | Company | Crude distillation capacity (thousand bbl/d) |

|---|---|---|

| Ras Tanura | Saudi Aramco | 550 |

| SATORP Jubail | Saudi Aramco, Total S.A. | 400 |

| Rabigh | Saudi Aramco | 400 |

| SAMREF Yanbu | Saudi Aramco, Mobil | 400 |

| Yasref | Saudi Aramco | 400 |

| Al Jubail | Saudi Aramco, Shell | 310 |

| Yanbu | Saudi Aramco | 235 |

| Riyadh | Saudi Aramco | 124 |

| Jeddah | Saudi Aramco | 88 |

| TOTAL | 2907 | |

| Source: Saudi Aramco, Oil and Gas Journal |

Oil exports and shipping

Saudi Arabia is the second-largest petroleum exporter to the United States after Canada.

Exports

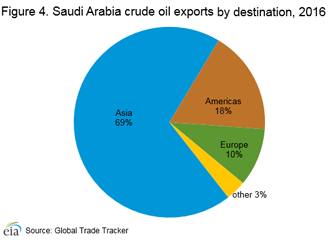

Saudi Arabia exported an estimated 7.1 million b/d of crude oil in 2016, according to the Global Trade Tracker (GTT). Asia received an estimated 69% of Saudi Arabia’s crude oil exports and most of its refined petroleum products.

Saudi Arabia exported an average of 1.1 million b/d of total petroleum liquids to the United States in 2016. In the first half of 2017, U.S. total petroleum liquid imports averaged slightly higher at 1.2 million b/d. Since 2012, Saudi Arabia has been the second-largest petroleum exporter annually (after Canada) to the United States, when it surpassed U.S. imports from Mexico. In 2016, after the United States, the next four top importers of Saudi crude and petroleum products were Japan (1.2 million b/d), China (1.0 million b/d), South Korea (0.9 million b/d), and India (0.8 million b/d), according to GTT.

Major ports

Saudi Arabia’s total crude oil export and loading capacity is about 13 million b/d. Most of this capacity comes from its four primary oil export terminals:

- The port of Ras Tanura on the Persian Gulf is Saudi Arabia’s

primary port. This facility,the world’s largest offshore oil exporting

port, has a combined handling capacity of about 6.5 million b/d. All of

Saudi crude oil grades load at this port, along with condensate and

products. The port comprises three terminals: Ras Tanura terminal,

Ju’aymah crude terminal, and Ju’aymah LPG export terminal.[20]

- The Ras Tanura terminal, the largest terminal at the port of Ras Tanura, has an average handling capacity of 3.4 million b/d[21] and 33 million barrel storage capacity.[22] The terminal can accommodate tankers up to 500,000 deadweight tons (dwt). All of Saudi Arabia’s crude oil grades are loaded at the Ras Tanura terminal.

- The Ras al-Ju’aymah terminal has an average handling crude oil capacity of about 3.12 million b/d,[23] and because of the availability of six single-point mooring buoys, the terminal can accommodate some of the largest tankers (700,000 dwt) for crude loadings.[24] All of Saudi Arabia’s crude grades are loaded at this terminal, along with bunker fuel (at a maximum loading capacity of 120,000 b/d).[25]

- The Yanbu King Fahd terminal on the Red Sea, from which most of the remaining volumes are exported, has a loading capacity of 6.6 million b/d.[26] The terminal includes seven loading berths and can accommodate tankers up to 500,000 dwt. Total crude oil storage capacity at the terminal is 12.5 million barrels. Only Arab Light crude oil grade is loaded at the Yanbu terminal.[27]

In addition to these primary export terminals, Saudi Arabia has other smaller ports, including Ras al-Khafji, Jubail, Jizan, and Jeddah.

Saudi Aramco plans to begin exports from the overhauled Muajjiz oil terminal on the Red Sea sometime before the end of 2017, which would raise Saudi Arabia’s total loading and export capacity to about 15 million b/d. Before the Iraqi Pipeline in Saudi Arabia (IPSA) was converted to a natural gas line, Muajjiz was used as an export terminal for the Iraqi crude oil that flowed through the IPSA. Muajjiz will be integrated into the Yanbu crude oil terminal.[28]

Major domestic petroleum pipelines

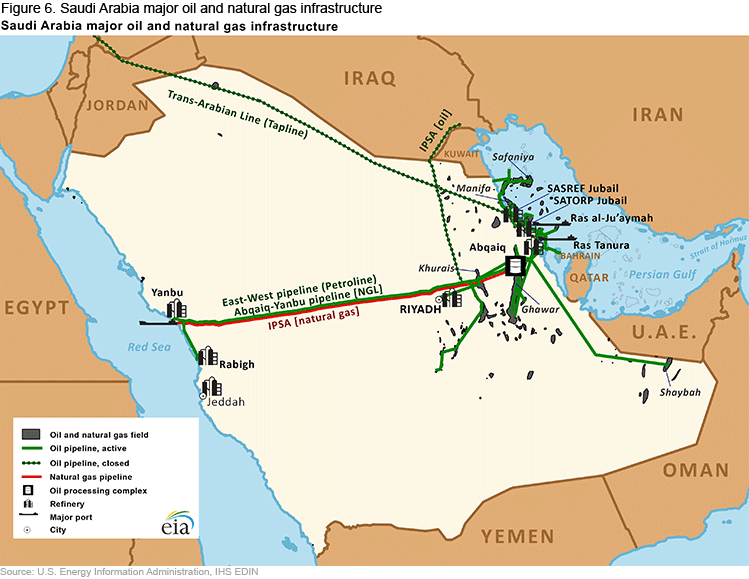

Saudi Aramco operates more than 90 pipelines and 12,000 miles of crude oil and petroleum product pipelines throughout the country, all of which link production areas to processing facilities, export terminals, and consumption centers.

The 746-mile Petroline, also known as the East-West Pipeline, is significant because of its large capacity and because it connects production and processing facilities in the east of the country to export facilities in the west, allowing the crude oil to bypass the Strait of Hormuz. The Petroline system, which runs across Saudi Arabia from its Abqaiq complex to the Red Sea, consists of two pipelines with a total nameplate (installed) capacity of about 4.8 million b/d. One of the pipelines has a diameter of 56 inches, and a nameplate capacity of 3 million b/d. The other pipeline is a 48-inch diameter. This pipeline had previously operated as a natural gas pipeline, but it was converted to an oil pipeline. This conversion increased Saudi Arabia’s spare oil pipeline capacity that bypasses the Strait of Hormuz from 1.0 million b/d to 2.8 million b/d, if the system operates at its full nameplate capacity. In 2016, Saudi Aramco announced plans to expand the capacity of the East-West pipeline to 7 million b/d, with a scheduled completion by the end of 2018. To date, little progress has been made on the pipeline expansion.[29]

Running parallel to the Petroline is the 290,000 b/d Abqaiq-Yanbu NGL pipeline,[30] which serves petrochemical plants in Yanbu. The Abqaiq-Yanbu NGL pipeline is Saudi Arabia’s largest NGL pipeline.

International petroleum pipelines

Saudi Aramco does not operate any major functioning international pipelines. The Trans-Arabian Pipeline (TAPLINE), built in 1947 to transport crude oil from Qaisumah through Jordan to Sidon, Lebanon, has been partially closed since 1984. The portion of the pipeline that runs to Jordan was closed in 1990.

The 1.65 million b/d, 48-inch Iraqi Pipeline in Saudi Arabia (IPSA), runs parallel to the Petroline from pump station #3 (11 pumping stations run along the Petroline) to the port of Muajjiz, just south of Yanbu, Saudi Arabia. The pipeline was built in 1989 to carry Iraqi crude oil to the Red Sea. The pipeline closed indefinitely following the August 1990 Iraqi invasion of Kuwait. In June 2001, Saudi Arabia seized ownership of IPSA as compensation for debts Iraq owed and converted it to transport natural gas to power plants. The portion of the pipeline that goes north into Iraq remains a closed, inactive oil pipeline.[31] Saudi Aramco pumped test volumes of crude oil through the pipeline in response to Iranian threats to close the Strait of Hormuz in 2012.[32]

Saudi Arabia’s only functioning international crude oil pipeline system is a 60-year old complex of four small underwater pipelines carrying Arab Light crude from Saudi Arabia’s Abu Safah field to Bahrain. This aging pipeline system is expected to be decommissioned after the construction of a new pipeline, with a capacity of 350,000 b/d, running between Abqaiq and Bahrain’s refinery at Sitra. The new pipeline is expected to be commissioned in 2018, and its capacity will eventually be expanded to 400,000 b/d.[33]

Shipping

Saudi Aramco’s shipping subsidiary, Vela International Marine Limited, operates 15 Very Large Crude Carriers (VLCCs) that transport crude oil between the Middle East, Europe, and the U.S. Gulf Coast. Vela also operates five product tankers that conduct coastal trade in the Red Sea and the Persian Gulf. Vela has a large number of VLCCs and product tankers employed on time or as spot charters. In addition to tankers, Saudi Aramco owns or leases oil storage facilities around the world, including Rotterdam (3.9 million barrels), Sidi Kerir (the Sumed pipeline terminal on Egypt’s Mediterranean coast), and Japan (6.3 million barrels).[34]

The National Shipping Company of Saudi Arabia (also known as Bahri) is the world’s largest operator and owner of VLCCs. Its fleet consists of 87 vessels, including 40 VLCCs, 36 chemical and product tankers, along with other cargo carriers. The Public Investment Fund (PIF) of the Saudi Arabian government holds 22% of the company’s shares, Saudi Aramco Development Company holds 20%, and the remaining shares are traded publicly on the Saudi stock exchange.[35]

Natural gas

Despite its sizeable reserves, natural gas production in Saudi Arabia remains limited. However, the Saudi government plans to monetize its vast natural gas reserves as it expands its petrochemical sector and natural gas-fired electric power generation.

Reserves

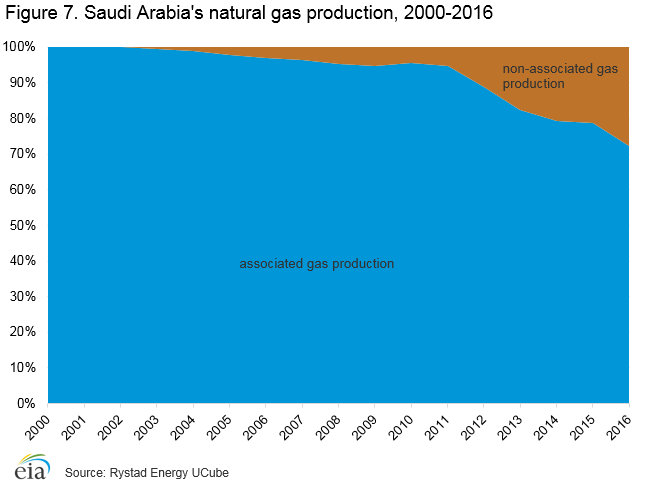

Saudi Arabia (including the Neutral Zone) had proved natural gas reserves of 303 trillion cubic feet (Tcf)[36] as of January 1, 2017, the fourth-largest in the world behind Russia, Iran, and Qatar, according to OGJ. Most of the natural gas fields in Saudi Arabia are associated with petroleum deposits or are found in the same wells as the crude oil. Increased production of this type of natural gas remain linked to an increase in oil production.

Production and consumption

Saudi Arabia does not import or export natural gas, so all consumption must be met by domestic production. Saudi Arabia’s dry natural gas production and consumption reached 3.9 Tcf in 2016.[37] Almost 60% of Saudi Arabia’s natural gas production in 2016 came from four fields: Ghawar, Safaniya, Berri, and Zuluf. Associated natural gas produced at the Ghawar oil field alone accounts for almost 48% of total production, according to Rystad Energy field-level production data.[38]

Rapid reserve development is necessary for Saudi Arabia’s plans to increase the growth of the petrochemical sector and provide fuel for power generation and for water desalination. All current and future natural gas supplies (except NGLs) reportedly remain earmarked for domestic use, in part to minimize the use of crude oil for power generation. However, natural gas production remains limited, as soaring costs of production, exploration, processing, and distribution of natural gas have limited supply growth. Saudi Arabia flared roughly 3% of its total natural gas production in 2016, according to Rystad Energy.[39]

Natural gas developments and strategy

Saudi Arabia is unlikely to boost its natural gas production from associated gas reserves in the near term because the country recently completed a major oil development phase, and it has shifted its attention to natural gas and downstream petroleum activities. In the longer term, Saudi Aramco’s strategy outlines a push for greater nonassociated natural gas development to help meet growing domestic demand. The company plans to almost double its gas production capacity in a decade, including unconventional gas developments to limit the use of oil in power generation and to provide feedstock to the country’s growing petrochemical industry.

In terms of upstream development, Saudi Aramco has focused heavily on major offshore natural gas developments in the Persian Gulf. Exploration and development are also planned for the Red Sea, northern and western Saudi Arabia, and the Nafud basin (north of Riyadh). Saudi Aramco divides its exploration activities into three regions: the northwest region of the country, the South Ghawar region, and the Rub al-Khali desert in the southern region of the country, (also knows as the Empty Quarter).

Saudi Aramco launched its Upstream Unconventional Gas program in 2011. In its 2016 Annual Review, the company reported having made progress completing wells in northern Saudi Arabia, delivering 55 million cubic feet per day (MMcf/d) of natural gas to electrical power facilities in the Wa’ad al Shamal industrial city.[40]

Saudi Arabia’s notable natural gas fields include:

- The Karan gas field, discovered in 2006, is Saudi Arabia’s first offshore nonassociated gas development. The Karan field came online in 2012, with a production capacity of 1.8 billion cubic feet per day (Bcf/d) of sour gas that is delivered via a 68-mile subsea pipeline to the Khursaniyah natural gas plant.[41]

- The Hasbah offshore field, which is part of the Wasit Gas Program, began production in March 2016. Total natural gas output capacity at the field is 1.3 Bcf/d.[42] A planned expansion of the Hasbah field will provide an additional 2 Bcf/d of gas to the Fadhili processing plant.[43]

- The Arabiyah offshore gas field, also part of the Wasit gas program, has a production capacity of 1.2 Bcf/d and began production in 2016.

The country’s total gas processing capacity was about 12 Bcf/d in 2016, according to Saudi Aramco. The Wasit gas plant reached full operating capacity in 2016 at 2.5 Bcf/d. The plant is fed by the Arabiyah and Hasbah fields, which supply more than 40% of nonassociated gas production. Commissioning the Wasit gas processing plant has made it possible for Saudi Arabia to dramatically reduce direct burn of crude oil for electric power generation and expand natural gas-fired generation.

As part of its plan to nearly double the country’s natural gas production capacity in a decade, Saudi Aramco is planning to add 1.3 Bcf/d of processing capacity at its Hawiyah plant, which processes nonassociated gas from the Ghawar field. The Hawiyah natural gas processing plant began operations in December 2001.[44] In addition to the expanded capacity of the Hawiayah gas plant, Saudi Aramco is now constructing the Midyan natural gas plant, which is 97% complete, in the Tabuk region in northwestern Saudi Arabia, according to the company. Construction on the Fadhili natural gas plant, located near the Jubail industrial city, also began in late 2016. The completed plant will be able to process 2.5 Bcf/d of raw natural gas.[45]

Upstream activities in Rub al-Khali (Empty Quarter)

The Saudi domestic natural gas market has traditionally been the sole domain of Saudi Aramco. However, Saudi Arabia opened the Rub al-Khali (referred to as the Empty Quarter in English), which encompasses most of the southern third of Saudi Arabia to foreign firms’ participation. Rub al-Khali is the only area where foreign firms were allowed to participate in the upstream exploration and development. A number of foreign firms formed joint ventures (JVs) with Saudi Aramco, including Shell (which formed the South Rub al-Khali Company, or SRAK), Lukoil (Luksar Energy Limited), and Eni and Repsol (EniRepSa Gas Limited). Over the past few years, efforts to develop unconventional natural gas resources by foreign firms have largely ended as a result of a lack of successful discoveries and high development costs.

Saudi Aramco, however, is re-exploring the Empty Quarter using new technology in advance of the company’s planned IPO. It is reportedly using advanced seismic technology to explore the vast area around the Turayqa gas field, partly in the area where joint ventures failed to find meaningful quantities of natural gas in the past.[46]

Domestic natural gas pipelines

Domestic demand for natural gas, particularly the delivery of feedstock to petrochemical plants, has driven expansion of the Master Gas System (MGS), the domestic natural gas distribution network in Saudi Arabia. MGS, first built in 1975, is an integrated gas gathering, processing, and transmission system originally put in place to recover the associated natural gas produced at the Ghawar oil field. Prior to the MGS, all of Saudi Arabia’s natural gas output was flared. The MGS transports natural gas from associated and nonassociated fields to natural gas processing plants, which separate out the NGLs. The NGLs are then transported to fractionation plants in Ju’aymah, Yanbu, and the Shaybah field plant, which recently added a second NGL processing train.[47]

Further expansion of natural gas production will require MGS expansions, and several additions to the MGS are in the planning or construction phases. These expansions include installing about 250 miles of natural gas line along the East-West oil pipeline. That pipeline would transport gas to plants at Yanbu; to natural gas lines in central Saudi Arabia; and to the pipeline between Riyadh and the Shedgum natural gas plant.[48]

Electricity

Saudi Arabia plans to increase electricity generating capacity to 120 gigawatts by 2032 to meet the country’s rapidly growing demand for electricity.

Saudi Arabia generated 330.5 billion kilowatthours (kWh) of electricity in 2016, 7% higher than in 2015, according to the BP Statistical Review of World Energy 2017. Like many developing countries in the Middle East and North Africa, Saudi Arabia faces a sharply rising demand for power. Demand is driven by population growth, a rapidly expanding industrial sector led by the development of petrochemical cities, high demand for air conditioning during the summer months, and heavily subsidized electricity rates. Saudi Arabia’s electric generating capacity in 2016 was approximately 66 gigawatts (GW). The country has the largest electric power generation expansion plan in the Middle East, with plans to increase generating capacity to 120 GW by 2032.[49]

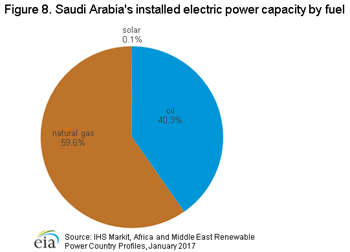

Nearly all of the existing generating capacity is powered by oil or natural gas, but Saudi Arabia plans to diversify fuels used for generation, in part, to free up oil for export. Although the Saudi Electricity Company (SEC) plans to continue reducing direct crude burn for electricity generation by switching to natural gas, plans are also in place to develop renewable sources for electric power generation. The King Abdullah City for Atomic and Renewable Energy (KACARE) calls for an additional 41 GW of solar power, 17.6 GW of nuclear power, and 9 GW of wind power by 2032.[50] These goals are ambitious, particularly given the slow pace of progress on currently planned nuclear and renewable projects.

The Saudi government has also issued a scaled-down plan to develop nuclear power capacity. In July 2017, the Council of Ministers approved proposals to establish the National Project for Atomic Energy, which includes large-scale (1.2-1.6 GW) and small-scale reactors that would be built in areas that are outside the national grid. KACARE is reportedly undertaking a technical study to construct four of these reactors.[51]

Sector organization

Saudi Electricity Company (SEC) is the largest provider of electricity in Saudi Arabia, with total available generation capacity of 74.3 GW. The SEC is responsible for generation, and the National Grid S.A. Company, SEC’s subsidiary, is responsible for the transmission and distribution of electrical power.[52] The state-owned Saline Water Conversion Corporation (SWCC), which provides most of Saudi Arabia’s desalinated water, is the second-largest generator of electricity, at 7.4 megawatts (MW) of installed capacity. SWCC plans to rapidly increase its desalination capacity, with an equivalent increase in generation capacity.[53] Privately-owned independent water and power plants also provide electricity to the grid. Saudi Aramco continues to build cogeneration plants to generate power for its own needs at various oil facilities. During 2016, Saudi Aramco completed cogeneration projects that added 984 MW of new power capacity.[54]

In 2007, Saudi Arabia began allowing private participation in the electric power sector, approving the first Independent Power Producer (IPP). The first two projects began operations in 2013: the 1,204 MW Rabigh 1 project in Mecca and the 1,729 MW Riyadh 11 project in Dharma. The Qurayyah project in the Eastern Province was completed in 2006, which added 3,927 MW of additional capacity. Several other IPP projects are expected to begin operations in the near term.[55]

Physical improvements are needed to allow more companies to sell power to the grid. SEC has ongoing and planned projects that will link power plants in the eastern, western, and southern portions of the country. To meet peak demand requirements, Saudi Arabia is participating in the Gulf Cooperation Council’s (GCC) efforts to link the power grids of member countries. The GCC is an alliance between six Persian Gulf states: Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates. The alliance seeks to build closer ties with the member countries, including the construction of electric power interconnections. The GCC Interconnection Authority is owned by the six member countries. The GCC member states’ grid interconnection was completed in 2011. In 2016, 1.32 million MWh of electric power was traded between five of the six member states.[56]

Notes

- Data presented in the text are the most recent available as of October 20, 2017.

- Data are EIA estimates unless otherwise noted.

Endnotes

1. U.S. Energy Information Administration estimates.

2. OPEC Annual Statistical Bulletin 2017, Tables 2.4 and 2.5, p. 19-20 (accessed August 2017), http://www.opec.org/opec_web/static_files_project/media/downloads/publications/ASB2017_13062017.pdf

3. International Monetary Fund, 2017 Article IV Consultation with Saudi Arabia, July 21, 2017 https://www.imf.org/en/News/Articles/2017/07/21/pr17292-imf-executive-board-concludes-2017-article-iv-consultation-with-saudi-arabia (accessed September 2017).

4. Middle East Economic Survey, “Saudis Slash Subsidies as Oil Revenue Collapses” Volume 59, Issue 1, (January 8, 2016).

5. Reuters, “Energy Subsidies Will Test Saudi’s Pain Threshold”

(October 29, 2015) and Joint Oil Data Initiative (JODI) data.

6. Oil & Gas Journal, “Worldwide look at reserves and production” (January 1, 2017).

7. Arab Oil and Gas Directory, “Saudi Arabia” (2014), page 392.

8. Internal estimate from U.S. Energy Information Administration.

9. IHS Markit, Upstream Companies and Transactions, Safaniyah, July 19, 2017 (accessed August 2017).

10. BP Statistical Review of World Energy 2017 (accessed August 2017).

11. Internal estimate from U.S. Energy Information Administration.

12. Saudi Aramco, Annual Review 2016, July 6, 2017 (accessed August 2017).

13. Energy Intelligence, “Aramco Advances Megaprojects Ahead of IPO” (April 27, 2017).

14. Facts Global Energy, “Middle East Oil Databook” (April 2017).

15. Chevron Corporation, https://www.chevron.com/worldwide/kuwait, (accessed August 2017).

16. Saudi Aramco, Annual Review 2016, July 6, 2017 (accessed August 2017).

17. Saudi Aramco, http://www.saudiaramco.com/en/home/our-business/upstream/oil-production.html (accessed August 2017).

18. Oil & Gas Journal, “Worldwide Refining Capacity Detail” (January 1, 2017).

19. Saudi Aramco, Annual Review 2016, July 6, 2017 (accessed August 2017), p.26

20. Saudi Aramco, Ports and Terminals Booklet (accessed September 2017), http://www.saudiaramco.com/en/home/news-media/publications/books/ports-and-terminals.html

21. U.S. Energy Information Administration estimate.

22. Energy Intelligence, World Crude Oil Data 2017 (Saudi Arabia).

23. U.S. Energy Information Administration, derived from information

published in Saudi Aramco’s Ports and Terminals Booklet, Ju’aymah Crude

Terminal section p.18 (accessed September 2017).

24. Energy Intelligence, World Crude Oil Data 2017 (Saudi Arabia).

25. U.S. Energy Information Administration, derived from

information published in Saudi Aramco’s Ports and Terminals Booklet,

Ju’aymah Crude Terminal section p.18 (accessed September 2017).

26. Arab Oil and Gas Directory, “Saudi Arabia,” (2014), p. 425.

27. Energy Intelligence, World Crude Oil Data 2017 (Saudi Arabia).

28. Reuters, “Saudi Aramco to boost oil loading capacity with reopened terminal,” May 1, 2017 (accessed September 2017).

29. U.S. Energy Information Administration estimates based on Lloyd’s List Intelligence tanker tracking data.

30. U.S. Energy Information Administration estimate.

31. U.S. Energy Information Administration estimate.

32. Middle East Economic Survey, “Iraq hopes for IPSA access with Saudi opening,” (Volume 60, Issue 35), September 1, 2017.

33. Reuters, “Bahrain, Saudi Arabia sign contracts worth $300 mln

for new oil pipeline,” September 17, 2015 (accessed September 2017).

34. Middle East Economic Survey, “Saudi Arabia looks east” (November 21, 2014).

35. Badri company website, http://www.bahri.sa/About/About-Bahri.aspx (accessed September 2017).

36. Oil & Gas Journal, “Worldwide look at reserves and production” (January 1, 2017).

37. BP, Statistical Review of World Energy 2017 (accessed September 2017).

38. Rystad Energy UCube (accessed September 2017).

39. Ibid.

40. Saudi Aramco, Annual Review 2016, July 6, 2017 (accessed August 2017), p. 18.

41. IHS Markit, Upstream Companies and Transactions, Profile Karan (accessed September 2017).

42. IHS Markit, Upstream Companies and Transactions, “Saudi Aramco

announces gas production at offshore Hasbah field,” (accessed September

2017).

43. Middle East Economic Survey, “Saudi: Key gas start-ups increase oil field flexibility,” (April 1, 2016).

44. Middle East Economic Survey, “Aramco receives bids for Hawiyah expansion, targets gas supply boost,” (August 25, 2017).

45. Saudi Aramco, Annual Review 2016, July 6, 2017 (accessed September 2017), p. 20-21.

46. Reuters, “Saudi Aramco uses new technology to re-explore vast Empty Quarter,” August 31, 2017.

47. Saudi Aramco, Annual Review 2016, July 6, 2017 (accessed September 2017), p. 20.

48. Middle East Economic Survey, “Saudi vision balances economics with planned social reform,” (July 22, 2016).

49. King Abdullah Center for Atomic and Renewable Energy, https://www.kacare.gov.sa/en/FutureEnergy/Pages/vision.aspx (accessed September 2017).

50. Ibid.

51. Middle East Economic Survey, “Saudi approves scaled-back

nuclear plans, studies reactors large and small,” (July 28, 2017).

52. Saudi Electricity Company, “Annual Report 2016” p. 15-16.

53. Saline Water Conversion Corporation, Annual Report 2014 (accessed September 2017).

54. Saudi Aramco, Annual Review 2016, July 6, 2017 (accessed September 2017), p. 54.

55. Saudi Electricity Company, “Annual Report 2016” p. 36-39.

56. Gulf Cooperation Council Interconnection Authority, http://www.gccia.com.sa/P/energy_trading/79 (accessed September 2017).

Like what you read?

Please consider supporting Eurasia Review. Thank you for your consideration!