In The Good Old Days, One Fourth Of Income Went To Food – OpEd

By Dean Baker

I am not ordinarily a celebrant for the state of the economy, but the media have been so over the top in pushing the economic doom story during the Biden presidency, that I feel the need to put some reality into the picture.

One of the central lines among the doomsayers is that we are spending a larger share of income on housing and that for many it has become altogether unaffordable. I will agree that housing is a serious problem. In fact, I recently authored a piece in a new collection on the issue, which I would encourage everyone to read. We need to build more housing and especially more affordable housing.

But acknowledging that housing is a serious problem is not the same as saying it is an unprecedented crisis, and many of the things that have been asserted in the media are simply not true. For example, it is not true that homeownership is no longer part of the American dream for young people. In fact, homeownership rates for young people are above their pre-pandemic level.

It’s true that the run-up in mortgage interest rates since the Fed began hiking in March 2022, coupled with rising house prices, has made the cost of buying a home prohibitive for many new buyers, but few expect rates to stay this high for long.

Mortgage rates are highly cyclical, they go up when the Fed raises rates in an effort to slow the economy. The current rates of near 7.0 percent are high compared to the 3.0 percent rates we saw during the pandemic, but they are not high by historic standards. In 1981, they peaked at over 18.0 percent.

I don’t recall reporters at the time writing pieces as though 18.0 percent mortgage rates would persist for the indefinite future. I am not sure why they feel the need to write that way about the current 7.0 percent rates.

Another aspect of the manufactured housing crisis story is that we are spending higher shares of our income on housing, with a record number of people spending more than one-third of their income on housing. This share has been dubbed as a crisis point by some.

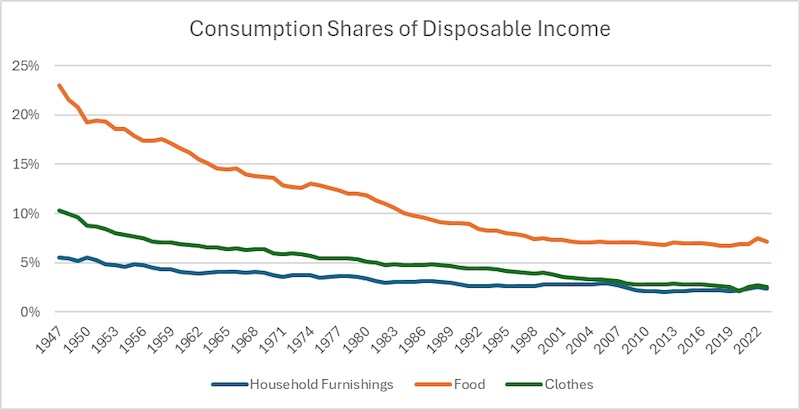

It is certainly true that we are spending a much larger share of our income on housing than in prior decades, but a big part of that story is that we are spending a much smaller share on other things. The graph below shows the share of disposable income going to food, clothes, and household furnishings since the late 1940s.

As can be seen, there has been a sharp reduction in the shares of all three. This is especially striking with food. In 1947 we spent 23.0 percent of our income on store-bought food. This had fallen to just 7.1 percent last year. The share of income going to buy clothes fell from 10.3 percent to 2.6 percent. The share for buying household furnishings dropped from 5.5 percent to 2.5 percent.

These declines freed up income to go to other areas, and one area that extra income went to was housing. The houses we live in today are on average much larger than the ones we lived in 75 years ago. They are also far more likely to have air conditioning and relatively clean sources of heat. (Coal furnaces were still common in the late 1940s.) They are much better protected against fires and less likely to have harmful chemicals like asbestos and lead.

As a result of reduced spending in other areas, and the higher quality of the housing we live in today, the share of our income going to housing now exceeds 34.0 percent, on average. (This figure includes “owner equivalent rent,” the money that a homeowner would be paying to rent the home they live in.)

Given the 34.0 percent figure is an average, it is hard to see the one-third level as a crisis. Rather, we probably need to recalculate what share of income going to housing costs presents an unmanageable burden.

None of this should be taken to mean that we don’t have to do things to make housing more affordable. We need to ease up restrictions that block both new construction and the conversion of empty office space to residential. And we should ensure that a substantial share of these new units are affordable.

We can also take short-term steps to improve affordability, like limiting vacation rentals and having moderate rent control. A vacant property tax is also a good way to get more units on the market. It will also be good when Jerome Powell and the Fed get over their inflation fears and start to ease up on interest rates.

We have a serious shortage of housing in the country due to a sharp plunge in construction in the decade following the collapse of the housing bubble. We were gradually getting back to more normal levels of construction when the pandemic broke out. If we can sustain higher levels of construction for several years and convert many of the offices that are currently vacant, due to the explosion in people working from home, we can lower housing costs.

But it is helpful to look at the issue with clear eyes. The biggest reason housing has grown as a share of our income is that we are spending so much less on other necessities. That is a good thing.

This first appeared on Dean Baker’s Beat the Press blog.