Central Banks Must Enhance Transparency To Build Trust – Analysis

The Bank of Canada published a detailed summary of its Governing Council deliberations for the first time last month, joining nearly two dozen other central banks in regularly releasing detailed information on monetary policy decisions.

Economic and financial turbulence calls for greater transparency from policymakers. As central banks raise interest rates to curb inflation, stakeholders increase their scrutiny. In some countries policymakers face growing calls to reign in their autonomy. To maintain public trust, safeguard independence, and enhance policy effectiveness in the face of such challenges, monetary authorities must focus on transparency and accountability.

Stefan Ingves, who stepped down in December after 17 years as governor of Sweden’s Riksbank, said it best:

“Independence demands transparency,” he said in a January interview with Central Banking. “If you’re independent, it’s vital that people can understand what you are doing. If you are independent and you tell the general public ‘It’s none of your business,’ independence will be taken away from you, sooner or later.”

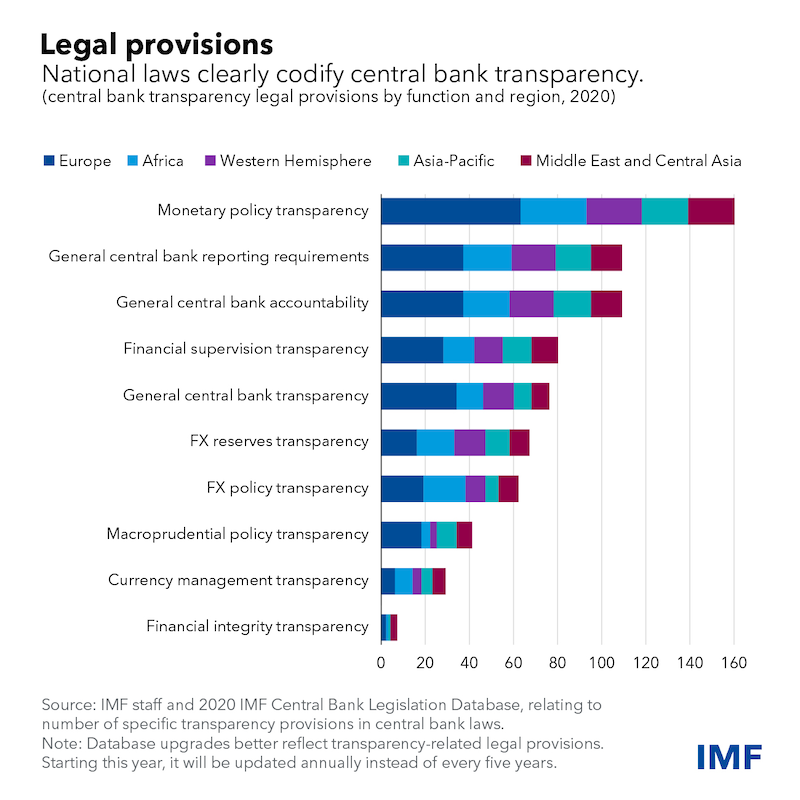

Many laws already include explicit transparency provisions, especially for monetary policy, as the IMF’s Central Bank Legislation Database shows.

The IMF has recognized the importance of transparency and actively promoted it. The Executive Board in 2020 adopted a new voluntary Central Bank Transparency Code, a comprehensive set of principles covering mandates, functions, and operations. Based on the code, the Fund offers central banks the opportunity to participate in a review of their transparency practices.

The reviews help central banks gauge their transparency and accountability, facilitating more effective communication and better-informed dialogue with lawmakers, investors, and individuals.

To date, the IMF reviewed the central banks of Canada, Chile, Morocco, North Macedonia, Seychelles, Uganda, and Uruguay, covering governance, policies, operations, outcomes, and relations with other official stakeholders, such as government and financial regulators. We summarize experience of pilot reviews in a new policy paper.

The reviews spotlight the importance of transparency in facilitating accountability, as well as detailing central bank performance and compliance with mandates. They also help facilitate more effective communication between central banks and their various stakeholders, including lawmakers, news media, academics, and the public. This helps them to adjust their communication tools, channels, and messages to the needs of the targeted audiences, reducing uncertainty and contributing to better policy choices.

How did central banks react to the recommendations? Beyond the Bank of Canada’s decision to release summaries of policy deliberations, the Central Bank of Chile approved a new transparency policy based on the IMF’s transparency review and created a specialsection on its website to provide the additional information on the way it operates.

The Central Bank of Seychelles began publishing a Monetary Policy Report, while the National Bank of the Republic of North Macedonia disclosed audit and risk management details. The central banks of Morocco, Seychelles, and Uganda used review findings to boost the effectiveness of their communications by developing institutional strategies and strengthening communication units.

Behind every central bank are dedicated professionals. And the reviews helped raise their awareness about the need for clearer and more understandable communications. Consequently, as one central bank official noted in response to the survey conducted by the IMF after the pilot phase, it helps “build more effective and client-driven communication systems.”

What’s next?

As central banks face mounting challenges, it is critical that they improve transparency because, ultimately, their independence and policy effectiveness will be at stake.

Future transparency reviews will be available to all IMF members as a voluntary tool to improve transparency and accountability. The Fund will also build a repository of transparency practices, based on information documented during the reviews, to facilitate peer-learning among staff at different central banks. The new tool will help reinforce trust in central banks, as well as their credibility and effectiveness in an increasingly complex world.

*About the authors:

- Tobias Adrian is the Financial Counsellor and Director of the IMF’s Monetary and Capital Markets Department. He leads the IMF’s work on financial sector surveillance and capacity building, monetary and macroprudential policies, financial regulation, debt management, and capital markets.

- Jihad Alwazir is an Assistant Director at the Monetary and Capital Markets Department of the International Monetary Fund (IMF) and Division Chief of Central Bank Operations. His recent analytical work is focused on Central Bank Governance and Transparency as well as Central Bank Operations and Digital Money.

- Ashraf Khan is a Senior Financial Sector Expert at the Monetary and Capital Markets Department of the IMF. He leads MCM’s work on central bank governance, transparency, risk management, and cash currency management. He also contributes to the Fund’s work on fintech, and Islamic Finance, and manages the IMF’s Central Bank Legislation Database.

- Dmytro Solohub is a Senior Financial Sector Expert at the Monetary and Capital Markets Department of the IMF. His primary focus of work is central bank governance, transparency and communications. Since joining the Fund in October 2021 he led IMF’s Central Bank Transparency Review missions for Canada and Seychelles and contributed to various Technical Assistance projects.

Source: This article was published by IMF Blog

Like what you read?

Please consider supporting Eurasia Review. Thank you for your consideration!