US Economy Adds 661,000 Jobs In September, Unemployment Falls To 7.9 Percent – Analysis

The September employment report showed a sharp slowing in the rate of job growth, with the economy adding 661,000 jobs, less than half of its August rate. The unemployment rate fell by 0.5 percentage points to 7.9 percent, but most of this was due to people leaving the labor force. The employment to population ratio (EPOP) only rose by 0.1 percentage point. At 56.6 percent, it is still 4.4 percentage points below its year-ago level.

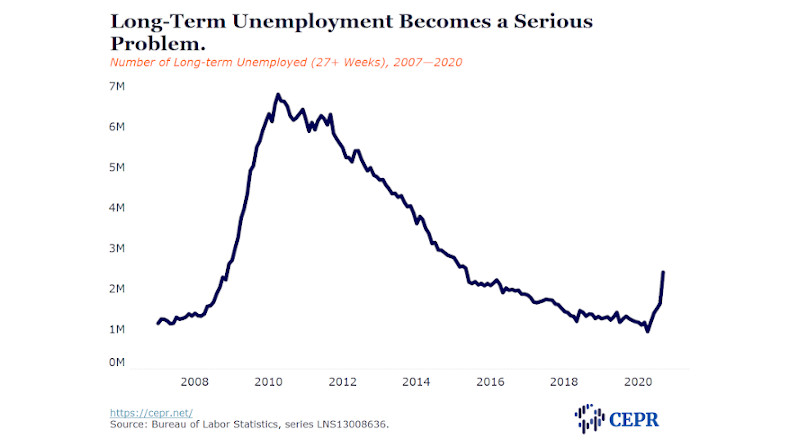

With jobs remaining in short supply, many people may permanently leave the labor force. The labor force participation rate is down 1.8 percentage points overall since last year, and 2.3 percentage points for women over age 20. The number of long-term unemployed (more than 26 weeks) also rose by 781,000 to 2,405,000. The people who drop out of the labor force or end up as long-term unemployed often suffer permanent damage to their labor market prospects.

There are also large racial differences in the impact of the recession. The EPOP for whites is down 3.9 percentage points from its year-ago level, while the EPOP for Blacks is down 6.5 percentage points. Asian Americans have also been hard-hit by the downturn, with a drop of 5.2 percentage points in their EPOP from year-ago levels. Their unemployment of 8.9 percent is considerably higher than the 7.0 percent unemployment rate for whites. Typically, the rate for Asian-Americans is slightly lower.

There are also large differences in impact by education. The unemployment rate for people with college degrees rose by 2.8 percentage points from its year-ago level, to 4.8 percent. For those with high school degrees the rise was 5.4 percentage points to 9.0 percent.

The differential impact of the recession is also seen in the loss of part-time jobs. The number of people choosing to work part-time is down 2,641,000 (12.3 percent) from its year-ago level. This fits with the 19.0 percent unemployment rate reported for workers in the leisure and hospitality industry, a sector that largely employs part-time workers.

One piece of surprising positive news in the household survey was the increase in the number of people who report being unemployed because they voluntarily quit their jobs. This jumped 212,000 to 801,000. The unemployed due to voluntary quits is actually the same share of the workforce as in September of 2019. Less positive is the share of unemployment due to temporary layoffs which fell from 45.5 percent to 36.7 percent. While some of these workers got back their jobs, many no longer consider their layoffs temporary. Still, this is an unusually high share; in the Great Recession it never peaked over 14.5 percent.

The job growth was again concentrated in the most hard-hit industries. The leisure and hospitality sector added 318,000 jobs, accounting for almost half of the total. Restaurants added 200,300 jobs, while hotels added 50,700. Retail added 142,400 jobs, while health care and social assistance added 107,700 jobs. Retail employment is now just 3.1 percent below its February level.

Manufacturing added 66,000 jobs, while construction added 26,000. Employment in these sectors now stands 5.0 percent and 5.2 percent below the February level. Mining reversed the pattern of sharp job losses and added 900 jobs. However, coal mining dropped another 900 jobs, with employment falling to 44,500, far lower than any pre-pandemic level on record.

The government sector shed 216,000 jobs, with a loss of 231,100 jobs in local education being partially offset by a gain in local non-education employment. While some of this is due to delayed school openings, state and local governments are struggling with huge budget shortfalls and will have no choice except to make large layoffs if more federal aid is not forthcoming soon.

This is, at best, a mixed report. Ordinarily adding 661,000 jobs and seeing a drop of 0.5 percentage points in the unemployment rate would be seen as very positive. However, we are still down by more than 10.7 million jobs (7.0 percent) from February. Also, we typically would have expected the economy to have added roughly 1 million jobs in this seven-month period. It would take us almost 18 months, at this pace of job growth, to make up that gap, and that does not even include the 130,000 monthly job creation that would be needed to keep pace with the growth of the labor force.

With several sectors, such as airlines and state and local governments, looking at another round of layoffs, the immediate picture does not look good. With more workers dropping out of the labor force and being faced with long-term unemployment, we are risking a large amount of long-lasting damage.

Like what you read?

Please consider supporting Eurasia Review. Thank you for your consideration!