The Awakening Giant: Risks And Opportunities For Japan’s New Defense Export Policy – Analysis

By Arthur Herman*

In 2014 the Japanese government promulgated a new defense export policy, lifting bans that had been in place for nearly thirty years. As inaugurated by the Abe administration, Japan’s new defense export policy offers huge opportunities for US-Japan defense industrial cooperation.1

These are opportunities Japan can exploit as it moves from having almost no presence in a rapidly expanding, increasingly globalized, and highly lucrative defense trade market into potentially being one of the market’s most important global players. This would be much like what it managed to do in the 1970s and 1980s when it became a dominant and innovative presence in the global automotive industry.

The United States can also take full advantage of these opportunities to increase its own defense exports and imports, including in some surprising areas. These include technologies and systems that until recently lay outside the conventional defense sector, but which now overlap with the Pentagon’s new third offset strategy for developing and fielding future military systems, in many cases by tailoring commercial high-tech technologies to fit defense needs (see chapter 5).2

At the same time, there are important risks that accompany this new defense export policy. These include:

- political risks, particularly with Japanese public opinion at home, as well as public opinion abroad;

- geopolitical risks, including Japan’s bilateral relations with Asian neighbors, particularly China;

- technological risks, particularly in the area of technology transfers and intellectual property (IP);

- economic risks for Japanese companies that venture into the new defense export arena without adequate preparation or adequate support from their government, which are vividly illustrated in Japan’s recent major effort to sell its Soryu-class submarines to Australia (see chapter 4).

Any new national policy, especially in the defense arena, comes with an inevitable learning curve. The highly competitive arms market today makes that curve especially steep for Japan. But when—not if—Japan masters that curve and becomes both an important defense exporter and innovator, much as it did in the automotive industry in the 1970s and 1980s, it can and will emerge as a formidable partner of the United States, or possibly even a competitor, in equipping its allies with defense technologies to make the world safer and more secure.

Chapter 1: Japan’s New Defense Export Policy

Nearly forty years after banning all defense and defense-related exports, in 2014 the Japanese government promulgated “three principles on transfer of defense equipment and technology,” which set the terms for transfer of military technologies by Japan’s government and defense industry to other countries, including the United States.3

Although often portrayed as an unprecedented “easing” or “lifting” of Japan’s four- decade-old defense export ban, the three principles themselves were actually far from unprecedented, nor were they the first three principles articulated to define Japan’s defense export policy. The first three principles were instituted in 1967 when the Sato administration blocked all defense exports to 1) Communist bloc countries; 2) countries subject to arms embargoes under the United Nations Security Council; and 3) countries involved in, or likely to be involved in, international conflicts. At the time, this would have included Israel as well as Arab countries such as Egypt and Syria.

Then, in 1976, the Liberal Democratic government of Prime Minister Takeo Miki extended the prohibition to all areas not included in the three principles, in effect shutting down any and all defense exports from Japan.

Beginning in the 1980s, however, it became clear that this policy was far too broad and sweeping, and successive governments granted exemptions to the defense export ban. In 1983, for example, Prime Minister Nakasone exempted the transfer of military technology to the United States,5 and in 1997, assistance was allowed for activities relating to removal of anti-personnel mines.6 Finally, in 1999, the government allowed cooperative research on ballistic missiles and missile defense.7

Other exemptions followed:

- 2006: Agreement for transfer of patrol vessels to Indonesia8

- 2013: Agreement for transfer of armored construction equipment to Haiti9

- 2013: Japan-Philippines exchange of notes for delivery of patrol vessels to the Philippines10

- 2013: Formal signing of the Japan-UK Arms and Military Technologies Transfer Agreement11

These last three were in accordance with the Guidelines for Overseas Transfer of Defense Equipment promulgated by the chief cabinet secretary two years earlier, in 2011, which eased the transfer of certain types of Japanese defense equipment and technologies in specific cases.12

All the same, there had been no effort to substantially revise, let alone replace, the three principles as a matter of policy until Prime Minister Shinzo Abe took office in 2012. Abe’s decision to invoke an entirely new approach to defense exports by permitting entire categories of defense transfers for the first time was a reflection of certain new geopolitical realities.13

These included a rapidly changing regional security environment, especially with China’s rise as an aggressive military power. There was also a changing global security environment, as Japan’s traditional reliance on the United States as its primary defender in the event of a major conflict seemed less and less certain—and seemed an artificial and outdated limitation on Japan’s ability to chart its own independent foreign policy course.

Therefore, at almost the same time that US-Japan defense security guidelines were being revised to make Japan a more active partner in operations for its own defense, and Article 9 of the Japanese constitution14 was being reinterpreted to permit a more proactive defense posture and “collective self-defense,” the Abe cabinet instituted a major reform in the defense export field, collectively known as “the new three principles.”15

Far from “lifting” or “ending” Japanese defense export controls, as some critics (and supporters) claimed, these three principles merely clarified when transfers of defense equipment from Japan to other countries will be prohibited or permitted. Under the three original headings, they can be summarized as follows:16

1) Transfers of defense equipment are prohibited when:

a) they violate obligations under treaties and other international agreements of which Japan is a signatory, e.g., the Chemical Weapons Convention; the Convention on Cluster Munitions; the Convention on the Prohibition of the Use, Stockpiling, Production, and Transfer of Anti-Personnel Mines and on their Destruction, known as the Ottawa Treaty; and provisions of the UN’s Arms Trade Treaty, among others;

b) they violate obligations under UN Security Council resolutions, including those preventing arms transfers to sanctioned countries such as North Korea and Iran;

c) they are destined for a country that is party to a conflict regarding which the UN Security Council is taking measures to maintain or restore international peace and security.

2) Transfers are permitted when they contribute to “the active promotion of peace” and international cooperation, or when they contribute to Japan’s own security, by

a) enabling it to implement international joint development and production projects with its allies and partners;

b) enhancing security and defense cooperation with its allies and partners; or

c) supporting Japan Self-Defense Forces (JSDF) activities, including maintenance of equipment that enhances the safety of Japanese nationals.

3) Finally, transfers are permitted when there are appropriate formal guarantees regarding extra-purpose use and third-party transfers, which the recipient government must provide to the Japanese government prior to transfer, and to which the government of Japan must give its consent.

In addition, in the interest of both transparency and accountability, Japan’s National Security Council is also supposed to receive an annual report concerning the overseas transfer of defense equipment issued by the Ministry of Economy, Trade, and Industry (METI), the government agency that has statutory authority over all defense exports.17

Chapter 2: The Role of Japanese Government Agencies and Trade Associations

Just as defense export policy and process in the United States is divided among several government agencies—the Departments of Defense, State, and Commerce—so too does Japan involve multiple agencies, including the Ministry of Defense. In Japan’s case, however, final authority is firmly anchored only in one agency, namely the Ministry of Economy, Trade, and Industry. This has powerful implications for the scope and direction of future defense trade, since commercial and defense export strategies will be more co-mingled than in the United States. It also makes for more unified control over the export process, providing an opportunity for a more coherent and coordinated defense export strategy than currently exists in the US government.

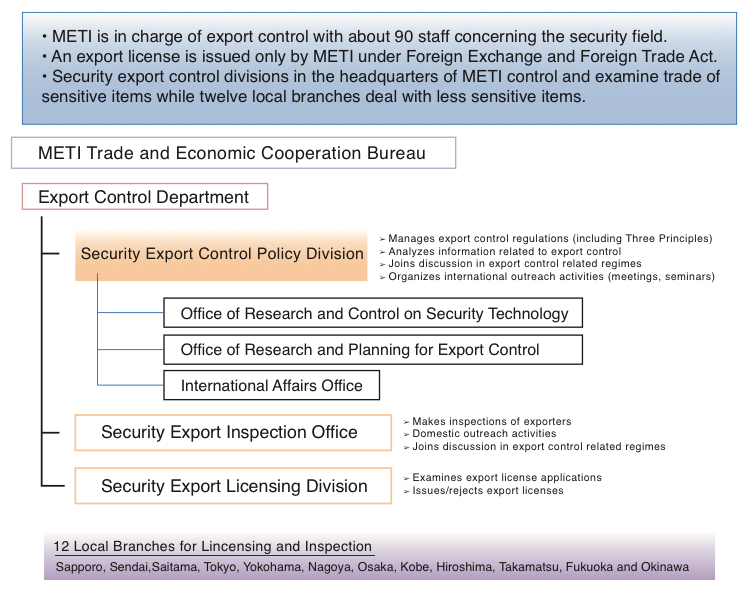

Ministry of Economy, Trade, and Industry

Under Japan’s Foreign Exchange and Foreign Trade Act, only the Ministry of Economy, Trade, and Industry can issue export licenses, including in the defense sector. Roughly ninety METI employees handle export controls in the defense and security field as part of the Security Export Control Division (figure 1). Those employees are mandated to manage export control regulations in accordance with the three principles from 2014. They also analyze all data relating to export control while joining discussions with other government agencies in export-control-related areas, including the Japan Ministry of Defense (JMOD).18

Figure 1. Organization for Security Export Control in METI

In the Foreign Exchange and Foreign Trade Act, Articles 48 and 25 specify certain goods and technologies19 that are controlled in defense transfers. These include items with both civilian and military applications (dual-use items); items that can be used for the manufacture of weapons of mass destruction (WMDs); and items with specific military end-use activities.20 The articles also designate which countries are permitted to be partners in defense export, the so-called “white countries,” which include the United States (box 1).21

There is, however, another player in the defense export policy: JMOD.

There is, however, another player in the defense export policy: JMOD.

JMOD and Defense Exports

In June 2014, JMOD issued a landmark paper, “Strategy on Defense Production and Technological Bases.”22 That document, which followed the release of the three principles of defense exports, acknowledged that these principles would significantly change the direction and force of JMOD’s own long-term goal to revivify Japan’s defense industrial and technological base.

For example, the strategy paper noted that “Japan’s defense industries must strengthen their international competitiveness to respond to changes” in the international defense market, which is changing rapidly. It also pointed to the importance of building strong relationships regarding defense equipment and technology cooperation with other countries, noting that Japan had concluded broad agreements on these issues with Great Britain in July 2013, France in January 2014, and Australia in June 2014. Such cooperation, of course, presupposes defense transfers from Japan.

For that reason, the paper stated, “MOD will formulate a framework which will enable the transfer of defense equipment, with nations that are likely to become partners in international joint development and production.” In addition, “MOD will study the postures and systems for smoothly promoting cooperation under government commitment and oversight throughout the life-cycle of transferred defense equipment.” This clearly points the way to creating a regular government-to-government and/or a foreign military sales program to oversee transfers of Japanese equipment and technologies, i.e., defense exports.

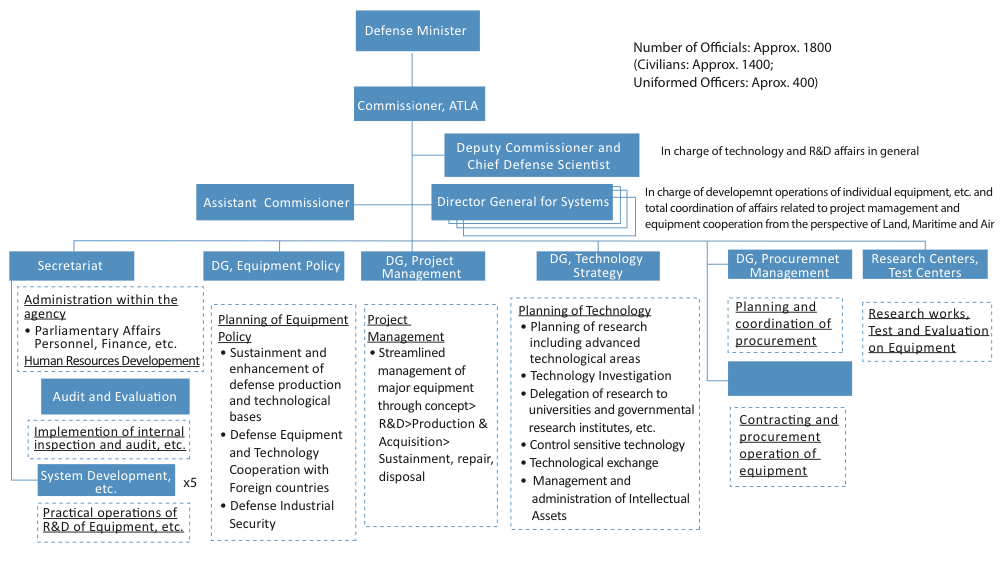

Thus, when JMOD’s new Acquisition, Technology, and Logistics Agency (ATLA) was established (figure 2), one of its important functions was to encourage and supervise defense equipment cooperation with other countries.

Figure 2. ATLA Organization Chart

Although JMOD has conceded that final authority over defense exports and technology transfers belongs to METI, it nonetheless sees an important role for itself in promoting these transfers, both as a matter of overall defense strategy and to strengthen Japan’s defense industrial base. For that reason, several former METI officials were transferred to ATLA to shore up its experience base in dealing with export and transfer issues, including the need for future export controls.

Keidanren and Defense Export Policy

Finally, the role of Keidanren (the Japanese Business Federation) in export policy needs to be considered. In July 2012, the Federation’s Defense Production Committee and the Aerospace and Defense Committee of the American Chamber of Commerce in Japan put out a “Joint Statement on Defense Industry Cooperation between Japan and the United States.” It described four models for cooperation, ranging from formal government-to-government programs like the US/Japan BMD/SM-3 missile program (see chapter 4), to cases where a licensee company unilaterally “supplies defense equipment in response to a request by the licensor’s country.”23

Although Keidanren was clearly in favor of a major reform of Japan’s defense export policy, there is every indication that the three principles exceeded its members’ expectations, especially those companies with high-tech product lines that are best positioned to take advantage of the new export regime.24

The real question is whether they and the rest of the Japanese defense industry are prepared to handle the challenges that this new export policy will present.

Chapter 3: Japan and the International Defense Market

The international defense trade market is an arena that Japanese companies, with their impressive marketing skills and sophisticated product development savvy, would seem destined to dominate. Global arms sales are slated to rise dramatically in the next decade, especially in Asia. Many countries are looking for systems that are the same as or similar to the ones Japan’s defense companies have been supplying to the JSDF and Japan Maritime Self-Defense Forces (JMSDF) for years (table 1).

Japan’s defense companies have developed and produced a range of military hardware for export that would be attractive to many overseas customers. This includes the Type 90 tank (Mitsubishi Heavy Industries, or MHI), OH-1 helicopter (Kawasaki Aerospace), and Komatsu Light Armored Vehicle (LAV), as well as Hayabusa-class patrol boats (MHI and Shimonoseki), Atago-class Aegis destroyers (MHI), Osumi-class tank landing ships (Mitsui), and Izumo-class helicopter-equipped destroyers (Japan Marine Ltd.). All are manufactured in Japan and almost certainly find customers, particularly in Asia. Indeed, the promise of Japan’s positioning for arms exports sales has been known for some time. In 1988 a secret memo circulated among Japanese defense executives that even predicted that if Japan were allowed to sell its defense articles abroad, the country could capture 45 percent of the world tank market, 40 percent of military electronic sales, and 60 percent of naval ship construction.25

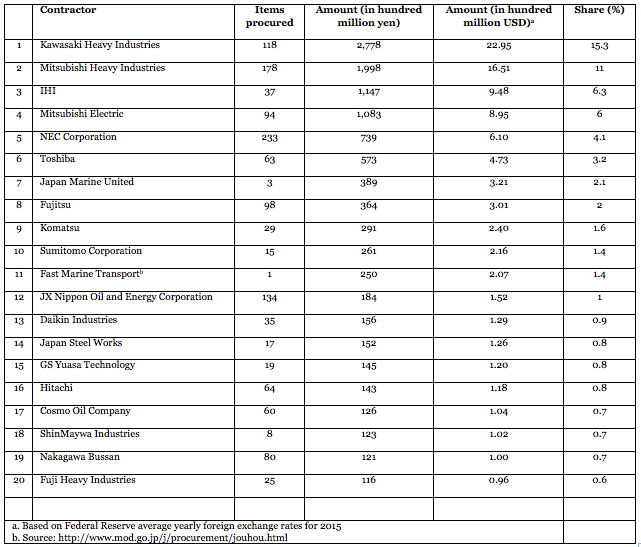

Table 1. Twenty Largest Japan Ministry of Defense Contractors in FY2015 (as of March 31), by Monetary Value of Contract

Whether that prediction was accurate or not in 1988, the sober truth is that today Japan’s defense industry also faces severe obstacles in creating its fledgling defense export market, some of which are of Japan’s own making.

The first is that they are latecomers to the game compared to the United States, Russia, China, or even South Korea. The rules of the international defense market, where every country has its own esoteric import-export restrictions and licensing requirements, are staggeringly complex. Much depends on relationships of trust developed over years and a proven track record. Foreign customers may like the sophisticated features of Japan’s Type 90 battle tank or its OH-1 observation helicopter, but they also like a tank or helicopter that’s been tested on the battlefield, as Russian and US export products have.

Another obstacle is that defense is a small share of overall business even for Japan’s biggest defense contractors—barely 4 percent of sales on average, according to Japan’s Ministry of Defense. Even MHI, Japan’s biggest defense contractor (ranking twenty-fifth in terms of world arms producers), does only 5.6 percent of its overall business in the defense market.26 This means that the sale of military systems abroad may not draw the kind of managerial attention and focus Japanese companies will need to penetrate those overseas markets, at least at first.

At the same time, in a country that is still largely pacifist, company executives will not like to be branded as “merchants of death” because of their burgeoning defense sales.27 Since Article 9 of the Japanese constitution in effect bans the use of military force,28 a strong culture of anti-militarism and pacifism has been reinforced by decades of quietism in the conduct of foreign policy. Of course, since 1954, Japan has made an exception for the defense of the home islands, and its defense budget remains impressively large for a primarily pacifist-minded country.29 Prime Minister Abe’s reinterpretation of Article 9, and defense spending that is rising to the highest level since World War II, represent important steps. But sales of defense articles abroad that could be characterized as “arms trafficking” are bound to have a negative impact on Japanese companies’ reputation at home, and consequently, there is reluctance at both the corporate and governmental level to tempt bad publicity.

Finally, Japan’s defense companies have grown up in a largely anti-competitive domestic environment, in which they have been accustomed for years to catering to the needs of a single customer, the Ministry of Defense and the JSDF. That has been a customer that knows what it wants and knows what companies can make it. In addition, the government has been inclined to make Solomon-like decisions on which companies make which defense systems to ensure that Japan’s defense industrial base is as widely distributed as possible and that everyone has a share in the action (as JMOD has done with sharing the contract for Soryu-class submarines with both MHI and Kawasaki).30

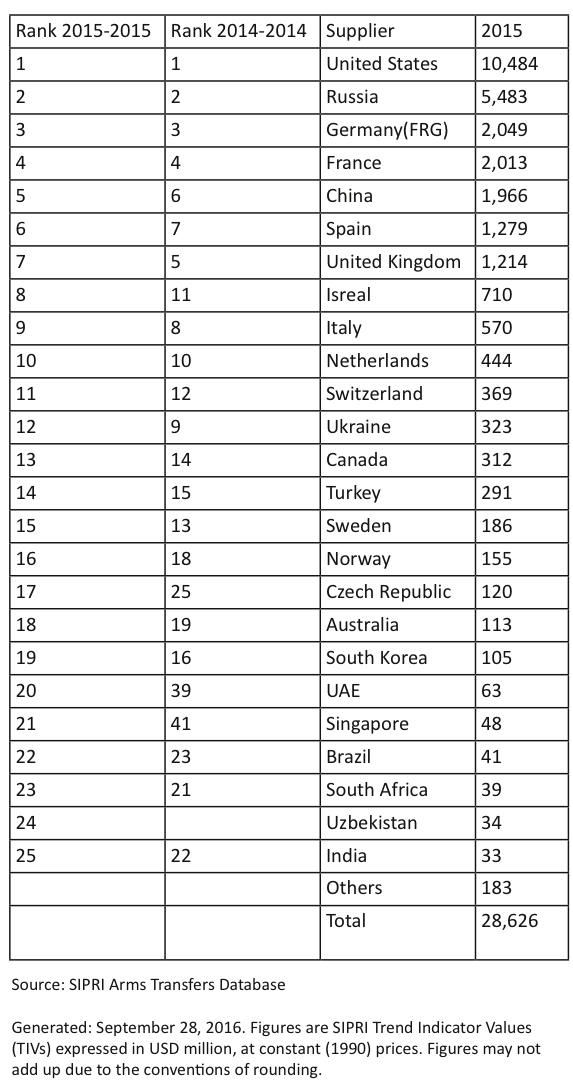

Japanese companies accustomed to an anti-competitive corporate culture will face a major challenge when operating in an international defense market that is intensely competitive, with multiple players with multiple skills and capabilities. These include not just the United States, Russia, and China, but Japan’s neighbor South Korea as well as Canada and Turkey. To qualify for the list of the largest arms exporters, Japan will have to double sales every year for a decade (table 2).

Table 2. TIVS of Arms Exports from Twenty-Five Largest Exporters, 2015

At the same time, Japan is slated to become a major importer of US arms, with its agreement to buy forty-two F-35 joint strike fighters, even though in terms of volume of American arms purchases, it still lags far behind Saudi Arabia and even India. Yet American defense companies know Japan is one of their most lucrative markets. Already American aerospace firms are lining up for the chance to replace Japan’s aging fleet of F-2 fighters with their own designs, and Japan will be hard pressed to summon up the resources to replace the F-2 with indigenous design and production.31 Furthermore, many of the technologies Japanese companies have employed to create defense systems for the JSDF are actually licensed from the United States, reducing the likelihood that foreign countries will buy Japanese when they can acquire the same technologies directly from the United States, probably at reduced cost.

In short, Japan faces many challenges as it tries to find its proper niche in today’s global defense market—just how challenging, two recent examples have revealed.

Chapter 4: Three Case Studies

Even before the declaration of the three principles, Japan began pursuing important defense sales to two Asian countries: Australia and India. Neither went according to plan, yet both offer important lessons for future export opportunities. The most important lessons of all may date back even earlier to Japan’s cooperation with the United States in joint development of a defense export product.

Australia and the Soryu-class Submarine

In July 2014, on a visit to Canberra, Prime Minister Abe and Australian prime minister Tony Abbott signed an historic agreement to jointly develop submarine technologies. This was intended to be the first step in an Australian purchase of Japan’s Soryu-class submarines to replace the aging Collins-class submarines the Royal Australian Navy (RAN) had relied on since the 1990s.32 The deal was the first important test of the Abe government’s new defense export policy and a potential $20 billion sales boost for the Soryu‘s two principal builders, Kawasaki Heavy Industries and Mitsubishi Heavy Industries.33 It was also supposed to be an important step in developing the increasingly close alliance between the two former World War II enemies, Japan and Australia.

The Soryu-class boat is the world’s largest conventionally powered submarine and reputedly the world’s best non-nuclear-powered submarine. Using a Sony-designed hydrodynamic system and equipped with special steel and noise-reduction features developed independently by Japan, it is fitted with an advanced Swedish-designed air independent propulsion system that allows it to remain submerged for extended periods—an important advantage in the wide reaches of the Pacific Ocean.34

At the time, it was understood that Australia would approach other countries, such as the United States, Germany, France, and Sweden, as part of its search to replace the Collins-class boat. It was also understood, especially in Japan, that this search would be largely pro forma and that purchase of at least ten Soryu-class submarines would soon be in the offing.35

Then, however, things began to slow down and go wrong.

First, in November, Prime Minister Abbott came under pressure to open the tender to replace the RAN’s submarines to international competition, including the German company HDW, which was building similar boats for Singapore, and the Swedish firm Saab.36 Miffed at this unexpected turn, Japan made noises indicating that it might choose not to resubmit its bid.37

Second, in September 2015, Prime Minister Abbott, a strong and committed proponent of closer defense ties with Japan,38 was replaced by Malcolm Turnbull,39 whose commitment to the Japan alliance was less certain and who made it clear that domestic considerations would also enter into any final decision.40

Those considerations included Australia’s trade unions, which began a campaign against the Japanese submarine deal. They pointed out that the new submarines would be largely built in Japan and not in Australian shipyards, while the other foreign competitors emphasized that it was important for Australia to participate in the boats’ construction.41

Critics pointed out that the Soryu class has half the range of the Collins class and does not carry any additional torpedoes or missiles. They also noted that the $38.5 billion price tag seemed too much when Canberra could buy off-the-shelf boats from HDW or Saab for far less.42

Proponents of the Japan deal replied by pointing out that the Australians would not only be getting access to sophisticated Japanese-designed systems but would also gain the advantage of interoperability with American submarine and anti-submarine warfare systems—something the Collins-class boats lacked. In addition, the Soryu-class submarine is outfitted to take on the most advanced US weapons and combat system programs and components, which were part of a separate contract with a US defense firm. Submarines built by other foreign countries would have no such capability.

Australia, by seamlessly integrating its submarine fleet with the US and Japanese fleets, went the argument, would gain an important strategic as well as technological advantage, especially in dealing with a major undersea maritime power such as China.

As time went on, however, these arguments lost their force, especially when the non-Japanese competitors proved to be more effective than was previously thought. According to a confidential source, the main Japanese bidder, Mitsubishi Heavy Industries, was forced to restrict access to information about key features of its Soryu-class design due to the JMSDF’s fears that important made-in-Japan technologies might leak out.

The turning point came in the spring of 2016, when a commission consisting of retired naval officers and officials drew up its recommendations on the tender. To the shock and surprise of the Japanese government, the MHI bid came in last, behind the bids of French company DCNS and German sub maker HDW.

The failure to seal the Australian submarine deal proved politically controversial. An article in Japan Times on June 23, 2016, was highly critical of Abe’s “obsession with exporting submarines to Australia, far removed from strategic diplomatic thinking” and also faulted “the attitudes of government agencies and private enterprises characterized by their blindly following Abe’s single-minded pursuit”43 of an Australian deal. Those government agencies included JMOD and ATLA.

Nonetheless, the criticism heaped on Abe, JMOD, and MHI in particular misses several marks. This was Japan’s first serious entry into the defense export arena, with a deal involving a highly complex and expensive weapons system with many moving parts and almost as many political actors.

In addition, the navy’s objections to selling Australia the same submarine technologies that Japan had spent decades developing, and on which the JMSDF depends and will depend for at least another decade, may have seriously weakened MHI’s case. Confidential sources have suggested that the failure to take the time to develop an export-version Soryu-class boat that overcame JMSDF’s objections meant that MHI was compelled to be vague about certain onboard capabilities in its presentations.

Neither the Germans nor the French felt any such compunctions. Indeed, Japan’s French competition, DCNS, proved masterly in its presentations. First, it focused on how a contract with DCNS would provide work and jobs for Australian workers and shipyards. Since the bidding rules that made building the boats in Australia only one of the three options for the contract, Japan failed to emphasize that possibility, while DCNS, and also Germany’s HDW, quickly committed to building in Australian yards. DCNS also arranged an off-site demonstration of those of its submarine’s capabilities in which it knew the RAN to be specifically interested. The French firm also hired a former chief of staff of the Australian Defense Ministry to advise it on the bid, and he in turn put together a list of a dozen requirements that DCNS needed to meet to win the contract. These included wooing the American defense contractors who would eventually be installing the boats’ all-important combat systems. In contrast, neither JMOD nor MHI hired any former Australian defense officials or RAN officers to help them in the tender process.44

According to sources, the off-site demonstration of submarine capabilities not only influenced the commission’s view of the French versus the Japanese tender bid; it also forced MHI to try a similar selling tactic in the final days of the competition.

In September 2015, MHI opened a unit in Australia (astonishingly, no such office had been set up in the fourteen months since the initial deal had been announced). The Abe government began talking about direct investment in Australia in areas besides defense, including creating a lithium-ion battery plant.

Then in April 2016, Japan sent one of its Soryu-class boats on a goodwill visit to Sydney. Its captain and crew learned on their way home that the contract had been awarded to DCNS.

The bottom line is that Japan found itself outmaneuvered and outsold by countries and firms that had far more experience in the international arms market. If the Abe administration is to be faulted anywhere, it is in its failure to allow more time to prepare for a serious, no-holds-barred competition with some of the most aggressive and accomplished arms dealers in the world. Until the government, JMOD, and Japan’s defense companies manage to conquer the arms sales learning curve, they will probably face more disappointments, particularly in the market for large complex systems.

India and the US-2 Seaplane

In January 2014, Japan and India announced that they were close to a deal in which Japan would sell India twelve US-2 seaplanes manufactured by ShinMaywa Industries and worth $1.65 billion.45 Although negotiations for this deal began in 2011,46 as of this writing (September 2016), it remains unsigned, and there is considerable speculation that it will never materialize.

The problems arising from this defense export, unlike those with the Australian submarine deal, do not spring from foreign competitors or failure to communicate the US-2’s key military capabilities. Indeed, India made it clear from the beginning that it was purchasing the planes for non-military use, such as air-sea rescue and maritime surveillance.

Likewise, there was no confusion about whether the aircraft would be built in Japan or India. Indian defense officials have stated that the deal was set to be signed in the first quarter of this year, with the first two seaplanes delivered off-the-shelf and the remaining ten to be built under license in India.

There were, however, serious questions raised on the Japanese side during negotiations over the types of surveillance technology transfers that would be allowed under the final deal. Fears arose that such transfers could be seen as arms transfers that would have an adverse impact at home politically. Indian navy officials in turn argued that the price tag per plane ($115 million) was too high if those planes failed to “come with other state-of-the-art surveillance technology which could enable the aircraft to be used for multiple purposes,” including presumably, military surveillance.47

Soon, there were other disagreements regarding India’s Defense Ministry offset policy, which requires 30 percent domestic production for procurements from foreign sources. A joint statement by then-Japanese Defense Minister Gen Nakatani and Indian Defense Minister Manohar Parrikar in July 2016 commended the effort made by both countries to come to an agreement on the US-2, but failed to make any further announcements of a pending deal. Some sources say both countries would prefer to let the deal wither away; others say the government of Prime Minister Narendra Modi is still hopeful that some final arrangement can be made.

Nonetheless, according to Abhijit Singh, former naval officer and head of the Maritime Policy Initiative at the Observer Research Foundation in New Delhi, “the Japanese, due to their history, are also not fully conversant with global norms on how defense deal negotiations are conducted.” This includes being adept at negotiating the labyrinthine rules and regulations of foreign bureaucracies, which can be particularly tricky in India—but which is a skill essential to doing defense business with New Delhi.

As with the Australian submarine deal, a lack of understanding of how defense export markets work has proved a major setback for Prime Minister Abe’s long-range plan for increased defense cooperation with both Australia and India—“including through two-way collaboration and technology, co-development and co-production,” as Abe and Modi announced in a joint statement in December 2015.48

But another danger also lurks in both the Australian and Indian cases. Export missteps will complicate or even upset closer alliance relationships. A Japan-Australia-India trilateral alliance has the potential to be a game changer in the Pacific and Indian Ocean security environment. Equally potentially, the loss of interoperability, especially with US systems; failure to achieve announced arms trade negotiations; and misunderstandings and unanticipated complications that breed a sense of frustration and even mistrust could work to the disadvantage of secure relationships with Japan’s allies, even undermining them.

Fortunately, this has not been the case with the United States. In contrast to the Soryu-class submarine deal with Australia and the US-2 seaplane deal with India, the Japanese-US joint development of the SM-3 anti-ballistic missile has largely been a success. It contains important lessons for Japan’s future defense exports, but also points to the road ahead on cooperation with the United States.

The United States and SM-3

On December 8, 2015, the US Missile Defense Agency, JMOD, and ATLA, in cooperation with the US Navy, announced “the successful completion of a Standard Missile-3 (SM-3) Block IIA flight test from the Point Mugu Sea Range, San Nicolas Island, California.” According to the announcement, “This test, designated SM-3 Block IIA Cooperative Development Controlled Test Vehicle-02, was a live fire of the SM-3 Block IIA. The missile successfully demonstrated flyout through kinetic warhead ejection. No intercept was planned, and no target missile was launched.”49

This test was the result of the SM-3 Cooperative Development Project, a long-term joint US-Japan development of a twenty-one-inch diameter SM-3 variant, designated Block IIA, to defeat medium- and intermediate-range ballistic missiles. Aegis Ballistic Missile Defense (BMD) is the naval component of the US Ballistic Missile Defense System (BMDS). The Missile Defense Agency (MDA) of the US Department of Defense (DoD) and the US Navy cooperatively manage the Aegis BMD program.

Back in December 2007, Japan conducted a successful test of an SM-3 Block IA against a ballistic missile aboard JDS Kongō. This was the first time a Japanese ship was employed to launch the interceptor missile during a test of the Aegis BMD system. In previous tests, the JMSDF had provided tracking and communications only.50

In 2008, Japan began codevelopment of the SM-3 Block IIA with the United States. The twenty-one-foot SM-3 missile, designated RIM-161A in the United States, is a major part of the US Navy’s Aegis BMD system and is a complement to the shorter-range Patriot missile. The intercept velocity of the latest SM-3 is around 6,000 mph, with a ceiling of 100 miles and a range of 270 nautical miles.

The missile’s kinetic warhead is a Lightweight Exo-Atmospheric Projectile, a non-explosive hit-to-kill device. According to non-classified sources, Japan is overseeing development of the nose cone, which protects an infrared ray sensor from heat generated by air friction, as well as the second- and third-stage rocket motors and the staging assembly and steering control section for the missile.51 As for the rest of the missile, the booster is the United Technologies MK 72 solid-fuel rocket, and the sustainer is the Atlantic Research Corp. MK 104 dual-thrust solid-fuel rocket. The third stage is the Alliant Techsystems MK 136 solid-fuel rocket.

Cooperation on the Block IIA proceeded smoothly, but when the United States was set to export it to other countries, including Qatar, Japan’s Foreign Ministry noted that this would be a technical violation of the long-standing ban on defense exports. After considerable discussion and considerable prompting from the US Department of Defense, then-prime minister Yoshihiko Noda decided to make an exception for weapons systems produced as part of bilateral defense agreements. Indeed, it was this decision that opened the door to other bilateral defense agreements and to the Abe government’s revising the entire export policy, leading ultimately to the three principles promulgated in 2014.52

The reasons why the SM-3 Block IIA has been a relative success for Japan’s new export policy compared to submarines and seaplanes—indeed, has heralded the new export policy itself—are many.

First, instead of trying to export an entire Japanese-made system, Japan conducted this venture in complete cooperation with the US government and US defense companies, which not only served as technical partners, but because they were more experienced in the vicissitudes of the international defense trade, were able to arrange for sale to Qatar.

Second, Japan was working in cooperation with the United States in ballistic missile defense, an area in which it faces few clear competitors, and indeed, an area in which the opportunities for more cooperation and codevelopment are relatively expansive. These include, for example, airborne boost-phase intercept ballistic missile defense. The United States already had a laser airborne system, which it is currently working to upgrade using unmanned platforms. However, there is currently a proposal involving two Japanese companies and a US technology firm for developing an unmanned boost phase interceptor using a conventional anti-missile missile. This could target and destroy missiles fired from North Korea while they are still in their boost phase, whereas land-based systems such as THAAD (Terminal High Altitude Area Defense) and Aegis Ashore do so only in the terminal phase.

If Japan moved ahead with this boost-phase interceptor, or BPI project, it would actually enjoy an advantage over the Pentagon and its usual US defense contractors. This is because development and deployment of BPI will be relatively inexpensive (less than $10 million by recent estimates), and if existing technologies are used, relatively near term. Indeed, it could become an export package system that other countries threatened by rogue nations’ ballistic missiles will want to purchase, and thus lead to a made-in-Japan ballistic missile defense system.53

Third, the SM-3 joint development project was underpinned by very clear formal agreements between the two countries. The first was in August 1999, when the Japanese government agreed to conduct cooperative research on four components of the interceptor missile being developed for the US Navy Theater-Wide (NTW) anti-missile system, for use against short- and medium-range missiles up to 3,500 kilometers.54 In 2007 came the signing of the General Security of Military Information Agreement, or GSOMIA, between Japan and the United States, followed (after considerable delay) by a formal Reciprocal Defense Procurement Memorandum of Understanding, or RDPMOU, in 2016. The United States has similar RDPMOUs with twenty-two other nations, but this was the first such agreement signed with Japan, and it points the way to further defense industrial cooperation down the road.

Fourth, the SM-3 project was undergirded by an American desire to encourage Japan’s more proactive defense and defense-trade posture to benefit the United States as well as Japan. Then-secretary of defense Robert Gates was a prime mover in getting the joint development of SM-3 underway and promoting its export sales as an important adjunct to US-Japanese strategic cooperation at the broadest level.

But another, even wider field of opportunity looms for Japan-US technology cooperation—and for possible Japanese defense exports.

Chapter 5: Japan and the Third Offset Strategy

Announced in 2014, the Pentagon’s so-called “third offset strategy” aims “to sustain and advance America’s military dominance for the 21st century” by developing key technologies that will underpin our defense systems of the future.55 These include unmanned systems, robotics, miniaturization, artificial intelligence (AI), and big data, as well as advanced weapons systems such as high-energy lasers, hypersonic missiles, and electromagnetic railguns.

As in the case of the first offset (the development of nuclear and ballistic missile technology in the fifties) and the second offset (the introduction of precision-guided munitions, stealth technologies, and digitized advanced intelligence, surveillance, and reconnaissance in the seventies and eighties), the plan is to leverage US technological advantages in the defense sector as a means of maintaining our country’s military edge.

Yet the technologies involved in the third offset are also rapidly emerging as exponential growth technologies. Exponential growth technologies can be illustrated by a simple example: while thirty linear steps roughly equal 30 yards, thirty exponential steps (i.e. that double the distance at each iteration) would equal one billion meters, or twenty-times around the earth. This will mean a dramatic change in both the per-cost basis and technological applications of future defense systems in ways that will mirror Moore’s Law.56

In announcing his “Defense Innovation Initiative” in 2014, then-secretary of defense Chuck Hagel specifically stated that since most innovation tends to come from outside “traditional defense contractors,” his department would “actively seek proposals from the private sector, including from firms and academic institutions outside DoD’s traditional orbit.”57 This would include a long-range research and development planning program to find, develop, and then field important technologies in space, undersea, air dominance and strike, and air and missile defense. The program would seek information from industry, academia, and federal research labs, as well as from foreign countries.58

In addition, as these advanced technologies approach “singularity,” opportunities to develop them further in conjunction with advanced countries such as Japan will increase, as will the possibility of deploying them across the US alliance system to dramatically upgrade leading allies’ military capabilities at much lower cost than conventional force-building. For Japan, this could represent a major breakthrough both in its own self-defense and in boosting collaborative security in the Pacific region.

Japan and Lasers

One such area is lasers and laser research. For example, in a 2012 paper published in Plasma Physics and Controlled Fusion, a team of researchers and engineers at Japan’s Osaka University described a laser they were developing and how it works. In July 2015, they reported successfully firing the Laser for Fast Ignition Experiments (LFEX) for a short pulse. The LFEX can credibly be called the world’s most powerful laser, and though the pulse was barely a trillionth of a second, it emitted two petawatts of power, or two quadrillion watts, roughly one thousand times the world’s total electricity consumption.59

A laser that could quickly shoot down or disable a cruise or ballistic missile would certainly be a huge tactical achievement. However, a laser such as the LFEX is too large and is not directly suited to military purposes. According to Michael Donovan, associate director of the Texas Petawatt Laser program, “If one wanted to destroy a satellite, the Japanese LFEX laser would not be the answer, as it would not propagate far through the atmosphere—even if it could be pointed toward the satellite.” Donovan adds that “the higher you get, the thinner the atmosphere. So a laser launched in space could propagate, but a petawatt laser is too large to economically launch into space.”60

However, as the MDA works on airborne laser projects as part of an integrated ballistic missile defense system, including boost-phase intercept of missiles using lasers and unmanned aerial vehicles (UAVs), much of the current Japanese research would seem to have important relevance to developing key components of military laser systems.

At the same time, the Technical Research and Design Institute of the Japanese Defense Ministry has designed a modified Aegis laser system for Japan’s latest 27DD destroyers to engage cruise and anti-ship missiles and other high-precision weapons. (One 27DD Atago-class destroyer is expected to be launched in 2020 and another in 2021.61)

Advanced Sensors

Another promising area is sensors. The Japan Times reported in July 2014 that Japanese companies had supplied sensors to the United States for the Patriot Advanced Capability (PAC-3) interceptor and transferred sensor-related technology to the UK.62 An example is Sony, which has a major plant for complementary metal-oxide semiconductor (CMOS) sensors in the Kumamoto Technology Center in Kyushu Region.63 These sensors are not only cheaper to manufacture than standard CCD (charged-couple device) sensors, even though both are essentially silicon chips that convert light into images; they also consume less power and offer a wider dynamic range. The CMOS sensor business is expected to grow from $10 billion in 2014 to more than $16 billion by 2020, and the range of military as well as commercial applications will grow with the size and flexibility of CMOS technology.64

In addition, Hitachi High Technologies has developed a range of ultra-thin wearable sensors, including one that detects the wearer’s emotional states.65 Many of these sensors are for medical uses or for semiconductor manufacturing that requires very high levels of precision. But the versatility and advantages of such sensors for intelligence, surveillance, and reconnaissance at a very granular level, including monitoring the physical state and stress of warfighters, seem obvious.

Composite Materials

Military-grade composite materials are highly useful for their low weight, durability, and ability to protect soldiers from injury. Today UAVs, unmanned underwater vehicles (UUVs), armored fighting vehicles, submarines, other naval vessels, and body armor all involve the use of composite materials, including advanced carbon laminates and so-called carbon “sandwich” products.

Composite material consumption has increased significantly in the commercial aerospace sector, from 5 to 6 percent in the 1990s to more than 50 percent in today’s advanced aircraft programs, such as the Boeing 787 and Airbus 350.66

As it happens, Japan has been a pioneer in development and manufacture of certain composite materials since the 1960s, and along with the United States, India, Brazil, and China, it is a leader in composite material research. The Japan Carbon Fiber Manufacturers Association includes Toray Industries, Mitsubishi Rayon Company, Kureha Corporation, Nippon Graphite Fiber Corporation, and other leading chemical, oil, and natural gas companies.

The Japan Society for Composite Materials, founded in 1975, recently organized its seventeenth US-Japan Conference on Composite Materials at Hokkaido University. Furthermore, Hokuriku Fiber Glass, a manufacturer of glass-fiber products in Komatsu, has developed a fiber-reinforced plastic using traditional Japanese weaving and braiding techniques, resulting in a three-dimensional carbon-weave heat-resistant material able to withstand temperatures as high as 3,000 degrees Celsius (5,432 degrees Fahrenheit).67 This material will be used by the Japan Aerospace Exploration Agency to protect unmanned spacecraft and probes, and its uses for other commercial or military satellite launches or for space reentry vehicles again seem obvious.

Indeed, a number of companies in the United States have begun using composite materials for lightweight launch rockets for small “cube” satellites. These materials not only make the rocket lighter but also easier to manufacture, and they can dramatically reduce the cost of a launch. The possibilities of partnering with Japanese companies such as Hokuriku Fiber Glass, which offers the added advantage of composite materials with ultra-high levels of heat resistance, appear promising.

In sum, the market for Japan’s defense exports includes many products whose military applications are not immediately obvious but which are both desirable and necessary as part of a US shift to a third offset overmatch of possible future adversaries and are fruitful avenues for US-Japan joint research and development.

The most important area, however, may be robotics.

Robotics

Japan has more than a quarter million industrial robot workers, and the robotics industry there is more important than in any other country in the world. According to Japanese estimates, in the next fifteen years, the number will jump to over one million, and expected revenue for robotics by 2025 is nearly $70 billion.68

Indeed, Japanese economic planners see robotics doing for Japan’s export economy what automobiles did in the 1970s and 1980s. Certainly something analogous may lie ahead in the area of defense-related robotics, which have assumed a new urgency within the third offset strategy model and where the Japanese enjoy several key comparative advantages.

Of course, major Japanese companies such as Honda, Toyota, Hitachi, and Fujitsu have dominated the field of industrial and/or assembly-line robots for years—so much so that very few non-Japanese robotics firms have been able to survive, let alone thrive, in this highly competitive global market. Combined with additive, or 3-D printing manufacturing techniques, advanced industrial robotics can bring dramatically improved production precision and performance to the US defense industrial sector, from conventional arms systems to more high-tech systems such as electromagnetic rail guns and directed-energy weaponry.

Beyond that market, however, Japan has also surged ahead in Android robotics, including robots that mimic human actions such as walking, talking, and smiling. A recently created robot, Child-robot with Biomimetic Body (CB²), can follow moving objects with its eyes. There is even a robot, HRP-4C, that can mimic fashion models walking the catwalk, and Kirobo, the first robot astronaut, traveled to the International Space Station in August 2010.69

For Japan, the advantages of relying on robots and robotic technology are obvious. In a country with a declining birth rate, robots represent a major “force multiplier,” in terms of both work and quality of life, for an aging population.

Yet the same analogy applies to Japan’s military and Self-Defense Forces, where a quality-over-quantity advantage over a possible antagonist such as China makes eminent good sense. It applies similarly to the US military and its third offset strategy, where robotics is not only one of the targeted technologies, but also has enormous applications across the entire field of advanced systems that make up the third offset arsenal, from advanced manufacturing processes to autonomous subsystems of larger networks.

For example, while Japan has not directly entered the arena of unmanned aerial and sea vehicles, Japanese robotics companies would clearly offer a range of applications and products that would be extremely useful in further developments in these platforms and their accompanying capabilities. This is particularly true in the defense technology sector, where China has become increasingly active and competitive.

Among these applications and products are swarm technologies. While swarm robots have only recently emerged from various robotics labs, Tokyo-based components maker Murata Manufacturing has unveiled the Murata Cheerleading robots, ten doll-like robots that are controlled by a wireless network and perform precisely synchronized dance routines, moving in unison to form shapes such as a circle or a heart, while spinning on their balls.70

“We designed the cheerleader robots to cheer people up and make them smile,” Murata spokesman Koichi Yoshikawa told Computer World in September 2014. “Their features can be summed up as ‘3S’: stability, synchronization and sensing and communication.”71 Those are precisely the characteristics needed for effective swarm systems in the military arena as well, on land, in the air, or at sea.

Finally, Japan’s preeminence in robotics will strongly complement the work the United States is doing in AI, in which it has been heavily invested for a decade or more. From Silicon Valley companies like Google and Facebook, to IBM and its mascot AI computer Watson, the private sector has been a leader in the Internet of Things (IoT), big data, and AI expertise.

Japan’s work in AI, by contrast, has been hardware oriented and seen as an adjunct to robotics research and development. Japanese AI scientists have spent considerable time, for example, doing research “that help robots learn and predictively determine what and how humans want them to act through experience-based inferences,” Mazakazu Hirokawa of Tsukuba University has been quoted as saying.72

Yet these developments of “human-friendly” robotic capability could complement AI developments in the United States, which emphasize independent creative thinking and “deep learning,” and could even dispel some of the suspicions about autonomous defense systems and “rise-of-the-machines” scenarios.

Above all, Japanese expertise in highly sophisticated robotics could provide ideal platforms for AI developments in the future defense sector. Whether the United States recognizes these opportunities for leveraging Japan’s lead in third offset technology is difficult to say and depends on many factors. One of them without a doubt is how well Japan does the job of “selling” its advanced technologies as complementing or supporting similar developments in the US defense sector, and how skillfully it cultivates this potentially huge customer for its high-tech talents.

Chapter 6: Risks of the New Export Policy

No discussion of Japan’s new defense export policy would be complete without considering the potential risks. While not exactly unprecedented, the new policy certainly represents a major change in Japan’s relationship with other countries, both friendly and unfriendly; with Japanese public opinion regarding weapons and arms; and with Japan’s own defense industry.

These risks can be divided into four groupings: political, geopolitical, economic, and technological.

Political Risks

In a country that is still largely pacifist, there could be a backlash against the government and the companies involved, which could be portrayed as forming a malign military-industrial complex that profits from conflicts, war, and the global arms trade. This possibility is hardly remote. The campaign to revise Article 9 toward a more proactive defense posture proved highly controversial, sparking a massive media campaign in opposition to the Abe policy, raucous demonstrations across Japan, including in the capital, and even fistfights inside the Diet itself.73 The initial lifting of the export ban did not provoke similar protests, in part because it was overshadowed by the controversy regarding Article 9, but also because defense exports do not have a notorious historical legacy linked to Japan’s imperialist past. In addition, because defense trade has hitherto played so insignificant a part in Japan’s commercial and geopolitical relations with other countries, a merchants-of-death narrative has not gained much purchase for Japan’s biggest defense contractors—at least for now.

However, if Japan does become a rising defense exporter, those narratives could be easily attached to the process, especially if Japanese technology is used in a conflict involving the loss of human life. If the Abe government were to fall, such narratives could even inspire a successor administration to push to reimpose the export ban—especially if Japan’s defense export industry is still in a fledgling state, so that halting exports has only a limited or highly marginal economic impact.

Even if no such restoration does take place, fear of it could act as a restraint on Japanese companies, preventing them from taking advantage of opportunities that could benefit both their bottom line and Japan’s security. In the worst-case scenario, this self-restraint could become a vicious cycle: reluctance to step forward into the export market narrows the range of options for defense trade in other countries, which means that Japan falls further behind in the global defense market, which in turn limits options for doing business. The result would be that Japan’s defense industry and defense-related companies wind up imposing their de facto ban on exports, to the detriment of Japan and its allies.

Geopolitical Risks

Some of Japan’s Asian neighbors have expressed worries that Japan’s new proactive defense policies mark a recrudescence of its role as an aggressive military power, as in the 1930s.74 Some of that concern is genuine (even some liberal Japanese have the same fears); some of it is disingenuous and politically motivated. Nonetheless, there is a risk that a Japanese entry into the global defense market that is seen as overly aggressive or aimed at a particular country, namely China, could fuel those fears.75

China sees Japan not only as an economic rival and an obstacle to China’s rise to regional and world hegemony, but also as a potential competitor in the world defense and arms market, one with important comparative advantages in quality and reliability, as well as in advanced high-tech areas.76 Beijing would not at all be displeased to see Tokyo’s new export policy fail.

The risk that Japanese defense exports could trigger a Chinese backlash would operate in two ways. First, it would discourage Japanese companies with extensive business ties with China from entering the export market. Second, it would discourage customers in Asia and elsewhere from “buying Japanese” for fear of offending China.77

Yet these fears may be overstated. Many of Japan’s potential customers, such as the Philippines, Vietnam, Malaysia, and India, have already seen their relations with China deteriorate over border disputes (India) or China’s claims to sovereignty in the South China Sea (Philippines, Malaysia, and Vietnam).78 Those that would be keener to maintain good relations with China, such as South Korea and Singapore, would be less likely to buy Japanese in any case. In addition, Japan has been dramatically scaling back its business investments in China over the last decade. This means that while many Japanese companies, like Sony and Toshiba, do have extensive business relations with China, the threat of a Chinese economic boycott or embargo is considerably less than it would have been in 2001 or 2005.79

In the final analysis, by far the greatest threat to good Sino-Japanese relations has been China’s ongoing aggressive military posture, especially in the East China Sea and the South China Sea, as well as its failure to rein in the ballistic missile and nuclear threat posed by its client state North Korea. The friction a growing Japanese defense export industry would generate between the two countries pales by comparison. Indeed, a very strong argument can be made that failure to build a strong and effective export strategy, including industrial and technological cooperation with the United States and other allies, will pose more risks than such a policy’s success by diminishing Japan’s capacity to restrain and deter present and future threats from its larger, more aggressive neighbor.

Technological Risks

These risks come primarily in two forms. The first is the risk of technology transfers, i.e., that Japanese defense technologies will be used for purposes contrary to Japanese national interests. These would include transfers to countries or groups that are committing violence, terrorism, or aggressive actions proscribed by the United Nations Security Council or other multilateral international bodies and/or treaties of which Japan is a member or a signatory.

Such transfers are, of course, specifically banned under the terms of the three principles.80 It is assumed that Japanese companies would take the necessary steps to make sure the law is observed and that the Japanese government would ensure that any company or country buying or receiving Japanese defense equipment adheres to the requirements of the three principles regarding third-party transfers (see chapter 1). In addition, a robust industrial-security regime can help to eliminate unwanted technology transfers that are due to industrial espionage or cyberespionage (see below).

Nonetheless, there is always some residual risk that Japanese technologies might fall into the wrong hands or be used for purposes that violate international law and offend Japanese public opinion. Therefore, it will be important for JMOD, METI, and other government bodies overseeing the export process to make sure the Japanese public knows that all possible steps are being taken to avoid these risks, and that Japan’s defense export trade is geared to strengthening its allies and the bonds of international peace and stability, as well as its own national security.

The second, more complicated, form of technology transfer risk is associated with IP issues and joint research and development with foreign governments and companies, particularly the United States. Many Japanese companies worry that they will lose their IP rights if they engage in joint development or joint venture projects with US companies and the US government, especially since the DoD has a policy that IP or patents created as a result of research and development it funded belong to it and the US government.81 At a February 2015 meeting in Washington, DC, organized jointly by the National Defense Industrial Association (NDIA) and the Society of Japanese Aerospace Companies (SJAC), several Japanese industry representatives expressed this concern, along with fears that even IP developed by their commercial divisions that is used in a system developed or produced jointly with a US defense contractor may be lost.

The Americans present (including myself) worked to reassure them that these IP and patent issues can be resolved through negotiation of individual contracts and should not be a barrier to US-Japan defense industrial cooperation. Those worries remain, however, and if they are not addressed in a more systematic way, Japanese companies may be reluctant to enter into joint projects with US defense contractors, even though these may be one of their most lucrative options.

Economic Risks

One type of economic risk is faced by companies that venture into the defense export arena without adequate preparation or adequate support from the government of Japan. This is vividly illustrated by the Australian submarine deal (see chapter 4),which may have inflicted lasting damage on the reputation of Soryu-class makers Kawasaki and MHI as reliable suppliers of advanced defense systems.

There is also the risk that if the US Congress perceives Japanese imports—including a growing volume of defense imports—as a challenge to American industry and jobs, as in the 1980s, this might lead to protectionist legislation that could hamper or even injure Japan-US trade relations. This has historical precedent: Professor Heigo Sato has pointed out that “as the United States began to focus on the issue of defense technology diversion and competition with Japan’s rising economy in the late 1980s, providing defense production licenses to an economic competitor was not seen as viable, even with security considerations in mind.”82

This led to one of the most notorious episodes in US-Japan defense industrial cooperation. In 1985, JMOD’s predecessor, the Japan Defense Agency (JDA), began looking for a successor to the F-1 ground support fighter. Two years later, JDA and the Pentagon signed a coproduction agreement involving the F-16 Fighting Falcon, to produce a plane for the Japan Air Self-Defense Forces (JASDF) dubbed the FSX.

The agreement, however, came under heavy fire from the US Congress, which complained that the FSX involved too little production for US defense firms and too much technology transfer to Japan—including technologies that Japan could commercialize at US expense. As a result, the agreements were rewritten, with severe restrictions placed on technology transfer and a mandate that US firms would get 40 percent of the production work. The JDA complied, and production of the Mitsubishi F-2 fighter began in 1996. But the clash left considerable bitterness on both sides, particularly in Japan, since the Japanese were convinced the original agreement already leaned too heavily toward the United States. In a Japanese corporate culture where memories are long and the sense of shame and humiliation runs deep, the FSX “debacle” still rankles—and has left residual fears that deeper defense industrial cooperation with the United States could lead to similar confrontations.

Again, those fears may be misplaced. The US defense market was very different in 1989, when US companies enjoyed a commanding position thanks to the heavy demands of the Cold War–era Pentagon for weapons and other equipment. With today’s more austere Pentagon budgets, all recognize that foreign sales, and cooperation with foreign defense firms, will be the key to sustaining growth. That necessarily includes Japan, and it is difficult to find any American defense industry official—or indeed any defense official—who is not eager to engage in defense technology and trade cooperation with Japan. In addition, given Japan’s very fledgling position in the defense export market and the fact that so many of its own defense technologies are US-derived, it is unlikely that firms like Lockheed Martin, Raytheon, or L3 Communications will perceive MHI or Mitsubishi Electric as dangerous rivals any time soon.

Chapter 7: Managing the Risks of a Defense Export Policy

Taken as a whole, development of a strong defense export policy for Japan involves multiple risks and challenges, which can make the policy itself seem daunting.

On the other hand, many of these risks can be managed and offset if the new export policy is combined with other changes in Japan’s overall defense trade strategy. These include four significant steps, the first of which is developing a robust industrial-security regime.

Exports and Industrial Security

A modern defense industry cannot thrive in the absence of effective industrial security and cybersecurity. Nevertheless, thus far Japan’s defense sector has managed to function, even prosper, without a formal industrial security apparatus. This is because the unique bonds of trust and honor between the Japanese government and its corporate partners have enabled them to work together successfully even without such an apparatus.

For decades, Japan’s defense industrial sector has been focused on indigenous products for the JSDF and licensed production of US systems. As Japan becomes both an innovator in defense products and services and an exporter, however, the lack of a robust industrial security and cybersecurity regime will create strict limits on customer confidence in the integrity of Japanese products and diminish the readiness of sophisticated users to procure defense equipment from Japan.

This will have to change as Japan enters the swirling waters of the international defense systems market. It will need a modern industrial security and cybersecurity program to match the present and future capabilities of its growing defense industrial sector.

What does a modern industrial security regime do?

A robust industrial security regime protects both national and intellectual property and will help Japan work more closely with other allied nations in developing and producing advanced defense systems.

First, it contributes to national security by serving as a continuous interface between the government and cleared industrial corporations.

Second, it administers and implements laws and regulations relating to a national industrial security program.

Third, trained industrial security personnel provide oversight and assistance to cleared contractor facilities and assist management security officers in ensuring the protection of Japanese and foreign classified information.

Finally, industrial security personnel facilitate the exchange of classified shipments between the United States and foreign countries and oversee foreign ownership, control, and influence countermeasures in the defense sector.

Eventually, industrial security program officers can also provide training and security awareness to ATLA and JMOD personnel, JMOD contractors, employees of other Japanese government agencies, and even foreign governments with which Japan is working on military-industrial and technical projects.

Japan has already taken some important steps in the industrial security arena. The most important was to sign the General Security of Military Information Agreement (GSOMIA) with the US government in 2007.83 In addition, the Japanese government has passed a state secrets law that protects classified information and imposes penalties on those who violate its provisions.84 The recent decision to intensify DoD-JMOD cooperation on cybersecurity is also an important move forward and a significant improvement over earlier US-Japan cyberdialogues.85

All the same, Japan has lagged in implementing an effective industrial security program as provided for in the GSOMIA. This increases the risk of insider threats as well as the possibility that hostile foreign intelligence services will penetrate Japan’s scientific and industrial institutions.

Incidents involving either of these would significantly injure Japan’s own national security and deter foreign countries and corporations from conducting further defense business with it, whether joint ventures/codevelopment or importing of Japanese defense articles. Hence, industrial security is one of the issues that must be addressed in order for a strong export strategy to take root.

The second step would be to develop an effective Foreign Military Sales (FMS) system under JMOD/ATLA supervision.

Exports and Foreign Military Sales

Defense export trade can take several forms: government-to-government sales, licensing of commercial sales through vendors, or a combination of both.

However, the complexity of modern defense systems (such as the Soryu-class submarine) has reduced the relative importance of commercial sales, particularly in developing major systems.

For one thing, very few major systems involve a single contractor or even a single “systems integrator” type of defense industrial firm anymore. The majority require careful government coordination and planning in order to assemble the myriad of firms and technologies needed to develop and produce the finished system and then to constantly maintain and upgrade that system in the field, particularly in a foreign country. Hence, export sales place demands that few companies, even the largest, can meet without the help of their own government from the very start.

In addition, users want to have guaranteed life-cycle support, training, performance, and product improvement and upgrades that only a government-to-government sale can offer.

Therefore, a strong, effective FMS program will become vitally important to building and extending Japan’s defense trade opportunities and will help to prevent failures like the Australian submarine deal.

Again, how would such a system work?

First, the US experience has demonstrated that no large bureaucratic infrastructure is needed to carry out an FMS program. Instead, JMOD/ATLA would establish representatives in targeted customer countries, such as Australia, India, the Philippines, and the United States. The Japanese government would also want to establish a secure financing and payments program so that the Japanese companies it has approached as part of FMS procurement will know that they will be compensated through the entire life cycle of the program. In a complementary fashion, the government of Japan would also guarantee that customers for Japanese-made systems will have support through the same life cycle, including eventual upgrading and replacement.

Finally, an effective FMS system would have an established program of offsets. One purpose would be to encourage customer satisfaction through joint production and development (something lacking in the Australian submarine negotiations86 and not handled satisfactorily in the Indian US-2 negotiations87). Another would be to broaden Japan’s access to foreign markets in both the commercial and defense sectors.

This, indeed, points to the third element in export-risk management: defense investment abroad.

Exports and Direct Foreign Investment

Under GSOMIA, Japanese investors are able to participate in the US defense market through joint ventures with US companies or as wholly owned subsidiaries, under three forms of security agreements.

The first is a special security agreement (such as the one made by British-owned BAE Systems with the US government88); the second is a proxy (used by Italian-owned Leonardo/Finmeccanica to penetrate the US market89); and the third is a security control agreement (used by French-owned Thales in its joint venture with Raytheon90).

All three offer Japan unprecedented opportunities for access to the US market, including the FMS system and military aid markets, which in 2015 totaled $46 billion and $10 billion in sales, respectively.91

The existence of Japanese-owned but US-based subsidiaries would also help reduce the perception that the Japanese defense industry is a competitive enterprise that hurts American jobs. Just as Nissan and Toyota have used the opening of auto plants in the United States as a way to promote their image as good corporate stewards, companies like MHI, Fujitsu, and IHI would be able to position themselves as job creators and technology incubators on American soil.

In short, moving to joint ventures and/or wholly owned subsidiaries in the United States could help Japan to become a global player and could serve as a powerful platform for speeding technology transfers for Japanese companies.

The most effective way to achieve the latter end, however, would be to streamline the entire defense trade process through a Defense Trade Cooperation Treaty (DTCT).

Exports and Defense Trade Cooperation Treaties

The goal of a formal DTCT is to allow license-free defense trade between the United States and key allies.92 There are rules restricting the use or sale without an export license of almost every component or material used in modern defense systems. The process of approving such licenses can be time-consuming and onerous, particularly under the International Traffic in Arms Regulations (ITAR) in the United States. A DTCT would provide a range of specific exemptions for companies doing defense trade in both Japan and the United States. These exemptions would:

- speed up the transfer of existing defense technologies in order “to achieve fully inoperable forces” and to do so by lowering existing arms control barriers between the two countries, including requirements for individual export licenses for defense articles;

- leverage the strengths of both countries’ defense industries and create a permanent new avenue for facilitating defense industrial cooperation between the United States and Japan, including codevelopment of new technologies and systems;

- foster an atmosphere of mutual trust and information sharing on defense systems between two long-standing allies.

In 2007, British prime minister Tony Blair proposed to President George W. Bush a formal DTCT between the United States and the UK.93 The two leaders signed the treaty in June of that year, and this was followed in September by a similar treaty signed between President Bush and Australian prime minister John Howard.94

The benefits of a similar DTCT with Japan seems obvious. Indeed, such a bilateral treaty makes sense on many levels. The State Department’s Directorate of Defense Trade Controls authorized over $7 billion worth of US-origin direct commercial sales of defense articles to Japan in FY2014, almost twice the value of such sales to the UK and approximately four times the value of such sales to Australia.95 With such an important ally and with trade volumes at this level, it makes good sense to enhance bilateral security by streamlining the bureaucratic process.

The benefit of a DTCT goes well beyond direct commercial sales of defense articles, however. It will directly foster deeper integration between the industrial capabilities of the two nations to dramatically increase the quality and capabilities of the technologies available to both partners. Bolstering defense trade between the world’s two most advanced high-tech industries would go far in developing key sixth-generation systems of the future. It would also go far in meeting the Pentagon’s own objectives for a third offset strategy in the areas of unmanned aerial and undersea vehicles; advanced sea mines; high-speed strike weapons; advanced aeronautics, from new engines to new and different prototypes; electromagnetic rail guns; high-energy lasers; and missile defense and cyber capabilities.

Finally, the terms of DTCT trade with other DTCT countries create, in effect, a Defense Common Market or community of DTCT companies, with the United States, Australia, the UK, and Canada all participating in defense trade more or less as licensing equals. It is even possible to envision other potential DTCT signatories joining the same Defense Common Market, including India.

Such a possibility does lie farther in the future. For now, however, an effective DTCT could be a vital cornerstone of a highly successful Japanese defense export strategy—one that matches the promise of Japan’s new defense export policy with the real need for more US-Japan defense industrial and defense cooperation, to the benefit of both countries and other allies.

Conclusion

Will Japan be an “awakening giant” in the field of defense exports in the future? What happens will depend on many factors. One of the most important, however, will be targeting the right markets for entry. While Japanese defense officials currently like to think of themselves as exporters and codevelopers with countries like Australia, the UK, France, and India, Japan’s new defense export policy’s biggest opportunity may well be here in the United States.