How Natural Gas Market Integration Can Help Increase Energy Security – Analysis

Closer ties allowed Europe to find new natural gas sources after Russia’s supply cutoff, and growing global export capacity can reduce market fragmentation

Natural gas might be the same commodity everywhere in the world, but prices can vary dramatically because of the complex network of infrastructure needed to transport it.

The result is a partially fragmented global market, mainly because most natural gas moves by pipeline—unlike the market for crude oil, which is more integrated and tends to trade at a single price in most places. Such fragmentation in the natural gas market means not only that prices differ across regions, but also that high prices in one part of the world don’t necessarily transmit to buyers in other places.

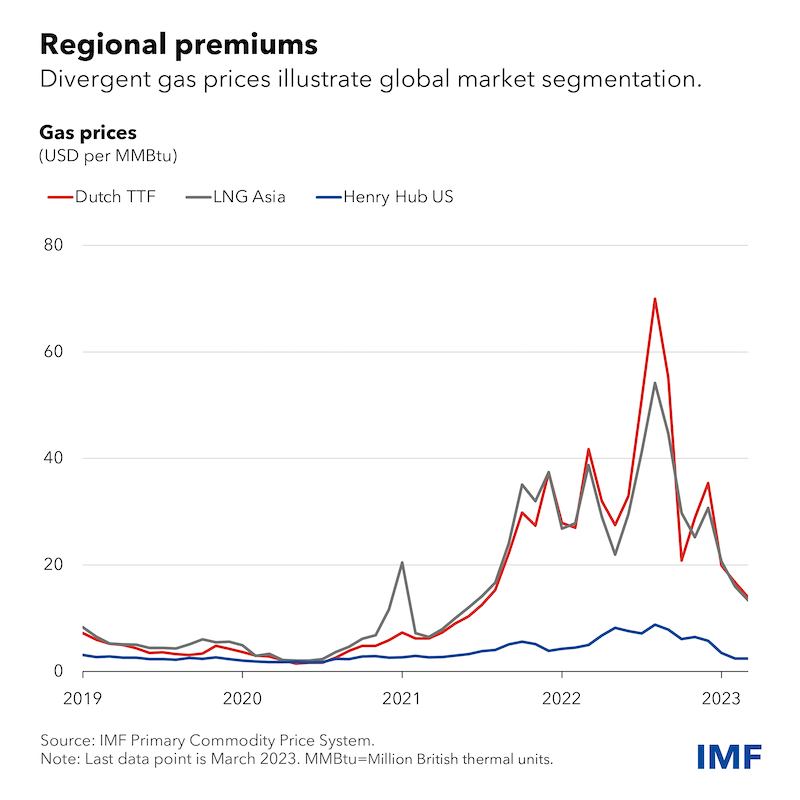

Russia’s invasion of Ukraine provided a stark illustration of the effects of segmentation. Pipeline flows to Europe from Russia dropped by 80 percent since mid-2021, sending the continent’s gas prices up 14-fold to a record level in August 2022. Prices for globally traded liquefied natural gas saw a similar jump. But LNG prices in the United States merely tripled, remaining several times below Europe and Asia.

The disparity in prices, and the US insulation against global gas-market shocks, stems from the idiosyncrasies of gas extraction and transportation. Historically, the US market was linked to crude oil prices because gas was mostly a byproduct of oil drilling, but this relationship, sometimes called artificial integration, has been unwinding over the past decade, mainly because of rising shale gas production. And as gas production surged in the US, which surpassed Russia in 2012 as the world’s largest producer, and export terminals were built, it became easier to sell into markets beyond North America.

Another important factor for gas prices is the technology needed to liquefy and ship the fuel, which must be converted into a compact form—about 600 times smaller by volume than in its gas form—called liquefied natural gas before it can be loaded onto specially designed carriers for transport by sea or road.

LNG export capacity is fixed in the short-term. Facilities for the liquefaction, exporting, importing, and regasification require major investment, so a regional shock, such as Russia’s invasion of Ukraine, can send regional prices moving in different directions.

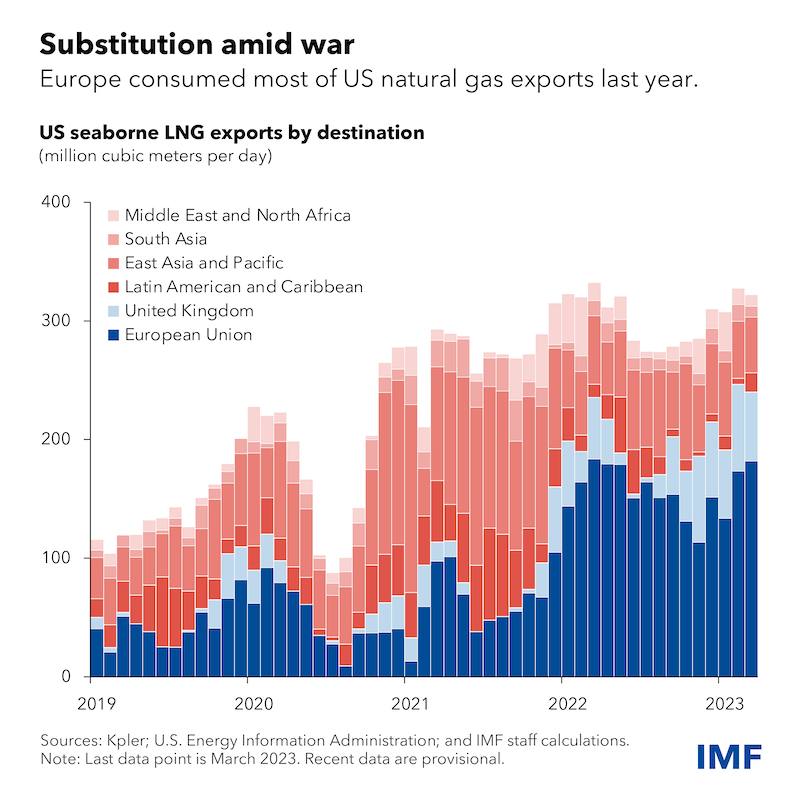

After the invasion last year, Europe turned to LNG to replace pipeline imports of Russian gas, and US shipments emerged as a key substitute. Why was that possible when US LNG export capacity is fixed? With gas in Europe commanding a temporary price premium during the spring and summer of 2022, Asian customers of US LNG decided to reroute their cargoes to sell in Europe.

There is another important quirk of the natural gas market at play. Pricing formulas for long-term delivery contracts with US companies usually use US prices. That meant Asian customers with long-term deals could buy more cheaply from the US, then reroute tanker ships at sea to sell cargo at the much higher European spot market price.

Despite an increasing reliance on LNG as a substitute for Russian pipeline gas, European LNG import capacity turned out not to be a binding constraint on market integration. European import terminals had plenty of spare capacity before Russia’s invasion of Ukraine, and with the addition of mobile floating storage regasification units, Europe has the necessary infrastructure to accommodate higher volumes of LNG imports.

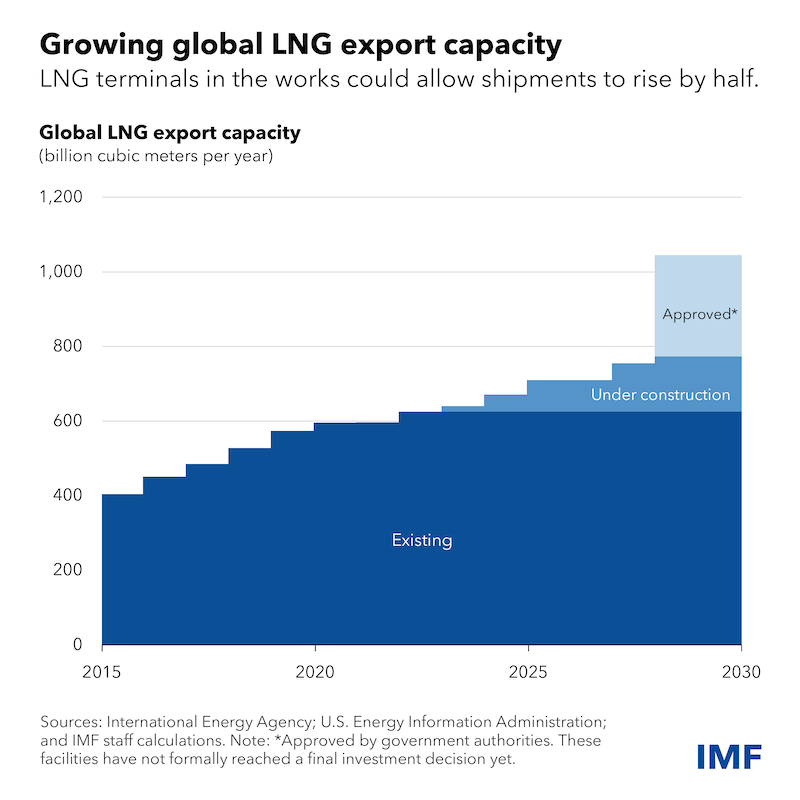

On the other hand, the United States and other gas producers are exporting at the limits of their capacities, and expansions to global LNG export capacity are needed to bring European and Asian prices back to historically normal levels over the longer term. In the United States, these capacities are poised to keep growing, even after already rapid gains. The first LNG export terminal in the country opened in 2016, followed by many more.

Sizable expansion projects already under construction in the United States, Africa, the Middle East, and elsewhere are likely to increase global LNG export capacity by 14 percent by 2025. Other planned projects could bring export capacity to around 1 trillion cubic meters, roughly a quarter of last year’s global gas consumption.

Securing financing to build new terminals, however, can face major hurdles. Companies need 15- to 20-year contracts to obtain bank financing for construction. Terminals usually cost $10 billion to $15 billion and take two to four years to complete. Timelines are less certain for projects without long-term sales contracts, and some may never be built.

Ultimately, expanded LNG export capacity for the United States and other producers may prove crucial to creating truly global gas markets that are balanced across regions. As advanced economies increase reliance on weather-dependent renewable energy from wind and solar, they will likely see critical periods of increased demand for supplemental natural gas to meet power generation needs. Integrating global gas markets and building needed infrastructure allows prices to stimulate demand and supply reactions in larger, more integrated markets. This helps to buffer global energy markets against supply shocks.

*About the authors:

- Rachel Brasier is a research officer in the Commodities Unit in the Research Department of the International Monetary Fund. Her research interests include global energy security and the energy transition. She has several years of prior professional experience in energy economics as a research analyst in the energy group of the Research Department of the Federal Reserve Bank of Dallas, and in economic development in Texas and Ukraine.

- Andrea Pescatori is Chief of the Commodities Unit in the IMF Research Department and associate editor of the Journal of Money, Credit and Banking. He has written extensively on a variety of macroeconomic topics, including monetary and fiscal policy, and published in peer-reviewed journals.

- Martin Stuermer is an economist at the Commodities Unit of the IMF’s Research Department. His research interests are macroeconomics with a focus on energy, commodities, and the energy transition. Among others, he has publications in Macroeconomic Dynamics,Journal of International Money and Finance and Energy Economics.

Source: This article was published by IMF Blog

Like what you read?

Please consider supporting Eurasia Review. Thank you for your consideration!