Trade And Inventories Cause Drop In US GDP, Underlying Growth Healthy – Analysis

A sharp increase in the trade deficit, along with a slower pace of inventory accumulation, lead to a 1.4 decline in first quarter GDP. These two factors subtracted 4.0 percentage points from the quarter’s growth. However, consumption and investment demand were both strong in the quarter, rising at 2.7 percent and 9.2 percent annual rates, respectively. As a result, final sales to domestic purchases, a category which excludes both inventories and the trade deficit, rose at a 3.7 percent annual rate.

Inventories and the Trade Deficit

The sharp rise in the trade deficit is actually tied to a strong buildup in inventories. While inventory growth was a net negative in the first quarter, inventories actually grew at a very strong $158.7 billion annual rate. This was a negative in GDP because inventories grew at an even more rapid $193.2 billion annual rate in the fourth quarter. (Normal growth in a pre-pandemic year would be around $75 billion.)

Since a large share of the items that end up as inventories are imported, strong growth in inventories is usually associated with a large rise in imports, adding to the trade deficit. This relationship is even stronger if we look at non-farm inventories (most of our farm products are domestically produced), which rose at a $185.3 billion annual rate in the quarter.

Farm Inventories Continue 16-Year Decline

Farm inventories fell at a $36.8 billion annual rate, continuing a decline that began in 2006. The current level of farm inventories is now just 53.0 percent of its level 16 years ago.

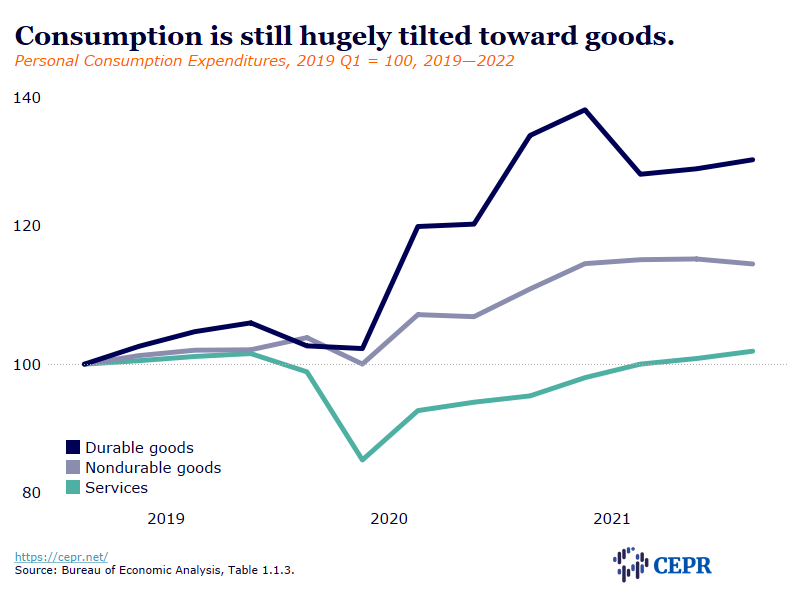

Consumption Grows at a 2.7 Percent Rate as Shift to Services Continues

Consumption grew at a healthy 2.7 percent annual rate in the quarter, driven entirely by a 4.3 percent growth rate in services. Consumption of goods actually edged down at a 0.1 percent annual rate. This switch to services is reversing the sharp shift to goods caused by the pandemic. Even with the first-quarter numbers, real consumption of goods is still 15.6 percent above its level in the fourth quarter of 2019, while service consumption is just 0.3 percent higher.

This shift will continue in the quarters ahead. In the first quarter, consumption of durable goods rose at a 4.1 percent annual rate, driven largely by a jump in car sales at the start of the quarter. Car sales slowed sharply in March. If the slower sales pace continues, this category will not be a major factor driving growth going forward. Consumption of nondurable goods actually fell at a 2.5 percent rate in the quarter.

The growth in services was broadly based across components. Interestingly, spending on restaurants and hotels did not rise at an especially rapid pace. Spending in this category rose at a modest 4.9 percent annual rate. This is not a big post-pandemic explosion; although omicron likely weakened January numbers.

Saving Rate Dips in Quarter

Consumption growth outstripped income growth, with the saving rate falling to 6.6 percent, down from 7.7 percent in the fourth quarter. This is somewhat below the 7.5 percent pre-pandemic average in the three years prior to the pandemic. One of the big questions going forward is the extent to which households will spend down savings accumulated during the pandemic. This drop in the saving rate could be a sign that they are spending out of recent savings, but the decline is still modest and may be reversed in future quarters.

Investment Growth Remains Strong

Investment rose at a 9.2 percent annual rate in the quarter. Structure investment edged downward at a 0.9 percent rate. But investment in intellectual products rose 8.1 percent, and equipment investment rose at a 15.3 percent rate. Compared with the fourth quarter of 2019, equipment investment is up 10.0 percent, while investment in intellectual products is up 16.5 percent. In contrast, investment in structures is down by 22.3 percent, as the pandemic has taken a huge toll in this area.

Residential Investment Grows at a 2.1 Percent Rate

The first quarter’s growth rate was a hair below the 2.2 percent rate of the fourth quarter. It is 14.6 percent above the rate in the fourth quarter of 2019. It is unlikely that the Fed’s rate hikes will have an immediate effect in slowing construction, as the run-up in prices and supply chain issues have created a considerable backlog. (Housing starts are now running at close to a 1.8 million annual rate, while completions are near 1.3 million.)

Higher rates have already been a huge hit to mortgage refinancing. They also have slowed sales, which will be a dampening factor in consumer durables, as fewer people moving will mean fewer purchases of refrigerators and other household appliances.

Government Spending Was a Drag on Growth in the Quarter

All categories of government spending fell in the first quarter. The 2.7 percent rate of decline subtracted a 0.48 percentage point from the quarter’s growth rate. This was the second consecutive drop for state and local spending, leaving it just 0.6 percent above the level in the fourth quarter of 2019.

Inflation Still on Upswing

The core Personal Consumption Expenditures deflator rose at a 5.2 percent annual rate in the quarter. It is now 4.6 percent above its year-ago level. With countries across the globe seeing high inflation (the breakeven inflation rate on 10-year government bonds in Germany was higher than in the US this week), it’s clear that this is not a problem specific to the US.

Overall, Underlying Growth Seems Healthy, but Swings in Trade Complicate the Picture

The story with consumption and investment looks mostly positive, as we see modest growth in the former and strong growth in the latter. We continue to see the needed switch from consumption of goods to services. The Fed’s rate hikes have collapsed mortgage refinancing and led to a large falloff in home sales. This will likely slow, or even reverse, the rate of house price rises. Overcoming supply chain problems will slow inflation across a wide range of goods.

Like what you read?

Please consider supporting Eurasia Review. Thank you for your consideration!